How do recession and property refinancing affect you?

By Paul Ho

/ iCompareLoan |

The world is entering a phase of slower growth — this is perhaps one of the more dangerous periods of its history. Since the financial crisis of 2008, the world has become more leveraged instead of less.

Between 2007 and 2014, global debt increased by US$57 trillion. Total debt has grown from 269% of GDP as at 4Q2007 to 286% of GDP as at 2Q2014.

Government debt has grown at a compound annual rate of 9.3%, way faster than GDP growth. And following closely behind is corporate debt.

The world’s total GDP is about US$70 trillion ($97 trillion). But most major governments are running budget deficits of between 2% and 5% of GDP. This means they are running a budget deficit of US$1.4 trillion to US$4.2 trillion. To put the numbers into perspective, US$4.2 trillion is about the annual production of the whole of Japan.

Since borrowings are not directly used to stimulate spending and do not correspond to a proportional increase in GDP, rising debt is incurred when governments service debt-interest payment.

Why is high debt a precursor to a recession?

Many countries are seeing a faster increase in debt than in GDP. This means that global production has not gone up correspondingly with the growth in debt.

For example, a government that incurs a budget deficit of, say, US$50 billion may use US$15 billion of that amount to service the interest payment of the debt. This leaves US$35 billion to be used for economic growth. That amount gets pumped into the economy to create investments or is spent on capital purchases (such as land, plants, machinery and equipment) and to hire people (to stimulate GDP growth).

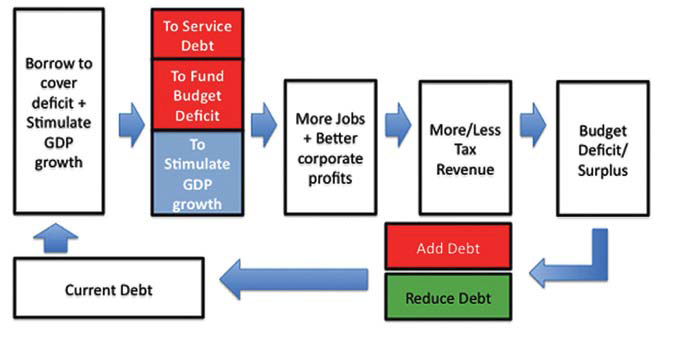

Based on Figure 1, you can see that much of the debt incurred by governments goes into servicing a current budget deficit, an existing debt and additional borrowing — if needed — which then goes towards stimulating the economy.

Figure 1: Government’s flow of debt and deficit spending

Corporate debt is also increasing at a faster rate than economic growth and corporations are becoming more indebted. The only bright side is that financial debt — that is, debt owed by financial institutions — is growing at 2.9%, which is close to economic growth.

Many countries are already servicing so much debt that much of a year’s budget goes towards repaying and servicing a debt. This leaves little money for disposable spending to help the economy grow.

Levying a low tax on the super-high-networth individuals does not help; the trickle-down effect is marginal as these people have a propensity to accumulate wealth and store them in tax havens rather than circulate the wealth (see Figure 2).

Figure 2: Global economy starved of consumers as super-high-net-worth individuals hoard cash and assets

As the global economy is starved of funding, income levels may not go up. Also, with corporations increasing their debt at a faster rate than that of GDP, this means they face the stress of reduced margins. That, in turn, could be the main cause of retrenchments.

The US dollar — the Monopoly game-keeper

The US dollar is the world’s pre-eminent currency. According to Stockholm International Peace Research Institute, the country’s military spending is more than the combined military spending of China, Saudi Arabia, Russia, the UK and India. The US’ military power, cultural soft power and non-governmental bodies influence the world we live in.

Up until 2013, the US dollar made up about 60% of the world’s foreign exchange reserves. The International Monetary Fund’s special drawing right is a standby borrowing for countries with weaker fiscal positions to draw on in times of emergency. Effective from Oct 1, the IMF’s reserves will be weighted in US dollars (41.73%), euros (30.93%), renminbi (10.92%), yen (8.33%) and pounds (8.09%).

Imagine you are playing a game of Mono poly and there is one player/banker and four other players. Each one has US$10, making a total of $50. One day, the player/ banker decides to print an extra $50 as he has run out of money. So, the total monetary amount in the game becomes $100.

This is as good as stealing 50% of the money of the other players, who decide not to play anymore. What does the banker/player do? He borrows — and promises to pay the sum back one day. So, there is now $100 in the game and a holding of debt (-$50). The money in circulation is $100, while the debt is $50, with the net effect of $50. This is also known as quantitative easing. However, it has the same effect as printing money because the value of the dollars held by the other players is diluted while the debt is not repaid.

Take the example of two poor people who have zero equity. One has $1 million in cash and a $1 million debt at 2% interest, while the other has zero cash but owes nothing. Which one is better off?

The first person is in a better position because he can buy food and pay the bills, for the time being. In the same way, unless countries choose to default on their debt or simply print currency notes outright to repay their debt, their economy will get worse.

Printing money is not a bad idea, as politicians like to kick the can down the road. But some say printing money will cause hyper-inflation. However, various countries have had rounds of QE, and there is hardly any inflation. In fact, we are facing deflation in Europe and Japan.

Perhaps the world’s major economies can get together to print money to reduce their debts.

Today, we have the productive capacity in industries and are largely not short of many resources. Hence, printing money to use up additional capacity and re-employ people is perhaps not a bad idea. Instead of borrowing money, a government could print money for capital-formation measures.

Deleveraging is painful

There will come a time when a debt has to be repaid. Deleveraging becomes imminent then and this will cause immense pressure as banks lend out less and the interest rate goes up.

Are corporations doing well?

Corporate debt is an area of concern. Singapore’s corporate debt-to-GDP has risen from about 100% in 2010 to 150% in 2014. Corporate interest coverage ratio has dropped from about 14 times to six times. This means that up till 2014, earnings before interest and taxes were six times those of interest payment.

In the event of an economic shock, such as a 25% drop in Ebit and a 25% increase in interest costs, many companies may start to retrench.

While the overnight interest rates benchmarks look likely to increase by 25% or more, the business interest rate is unlikely to go up that much as the interest rates for loans to small and medium-sized enterprises and other facilities already range from 8% to 20%. So, banks have the margins to absorb the increases. But will they?

SPRING Singapore is preparing to launch a working capital loan on June 1, whereby local SMEs can borrow up to $300,000. SPRING will offer loan loss provisions to banks. This is an indication of a worsening economy.

Not all companies will qualify for this loan as they still need to be profitable. Many of those companies facing hardship will perish, while some of those SMEs that qualify for this loan will stay afloat or grow to absorb excess retrenched workers.

Trade, an important segment of Singapore’s economy, has been declining since July 2014. The shipping and logistics sectors have been hard hit, as has the oil and gas sector. Singapore’s Purchasing Managers’ Index has fallen under 50% for eight months in a row. The April PMI stood at 49.8%, indicating a decline in orders.

Property prices are languishing

Private residential property prices have fallen gradually in the last 10 quarters since 3Q2013.

Many people will be hit by reduced rental income and higher interest payments. Owing to falling valuations, banks may be even more cautious about giving out loans. This pro- cyclical behaviour will cause more hardships to Singaporean households. When it comes time to refinance, a bank’s appointed panel of valuers may be so conservative that an outstanding loan may exceed 80% of loan-to-value.

Refinancing woes will hit home soon

The Total Debt Servicing Ratio was imposed in June 2013. Many people who are highly leveraged may have TDSR above 60%.

The Monetary Authority of Singapore allows a transition period in which borrowers for residential own-stay and investment properties can exceed TDSR of 60% (subject to meeting certain conditions) when they refinance, until June 30, 2017. If you fail to meet the TDSR after that date, you will be slapped with an expensive interest rate when you are already financially under strain.

Banks tend to offer rates that step up (for example):

• Year 1 = Sibor + 0.75%

• Year 2 = Sibor + 0.85%

• Year 3 = Sibor + 1%

• Year 4 onwards = Sibor + 1.25%

Therefore, a person will be faced with the following risks:

• Retrenchment,

• Reduced salary,

• Reduction of rental for investment property ,

• Margin call risks on falling property valuations,

• Increase interest cost, and

• Business failure, owing to debt being recalled and credit lines being cancelled

All these risks could hit you at the same time, just when you have fallen and need a helping hand owing to the pro-cyclical behaviour of banks. Hence, it would be wise to immediately convert to a rate that is stable and low, so there is no need to constantly refinance. Failing that, the consequences could be dire.

Paul Ho is chief mortgage consultant of iCompareLoan. He can be contacted at paul@icompareloan.com.

This article appeared in The Edge Property Pullout, Issue 730 (May 30, 2016) of The Edge Singapore.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Subscribe to our newsletter

Top Articles

Search Articles