Investments in Hong Kong's offices, shops and homes slowed to a standstill as Covid-19 outbreak adds to market's woes

By Kathleen Magramo kathleen.magramo@scmp.com

/ https://www.scmp.com/business/article/3074711/investments-hong-kongs-offices-shops-and-homes-slowed-standstill-covid-19?utm_medium=partner&utm_campaign=contentexchange&utm_source=EdgeProp |

Investments in Hong Kong's real estate are almost at a standstill, as the global coronavirus outbreak exacerbated the slumping sentiment from half a year of anti-government protests and the ongoing US-China trade war.

February's transactions declined 13 per cent from last year to 3,572 deals, the lowest monthly tally in four years, comprising both newly launched property and lived-in homes, according to estimates by Cushman & Wakefield. On the high end of the property market involving offices, shops or homes exceeding HK$100 million (US$12.87 million) in value, only 17 deals changed hands last month, the lowest since 2009 while the average deal size shrank 44.1 per cent to a decade low of HK$235.3 million.

"There is a lack of incentives for transactions," said Tom Ko, executive director of capital markets at Cushman & Wakefield. "Landlords want to wait until the coronavirus situation eases before selling their property and have stronger holding power due to low interest rates."

The data underscores the market's gloomy outlook, as the bull run in the world's most expensive real estate market stumbled after many months of anti-government protests sapped appetite. Now, as the coronavirus outbreak shows no signs of letting up, few buyers dare to venture into sales rooms or commit to big-ticket purchases.

The last weekend offered the latest sign of gloom: China Evergrande sold 49 of the 141 flats on offer at its Emerald Bay project in Tuen Mun, even after the developer increased its average discount to 14 per cent. The sales slump was the city's first major launch in two months, further weighing down on home prices, which have fallen 7.6 per cent this month from a record last May.

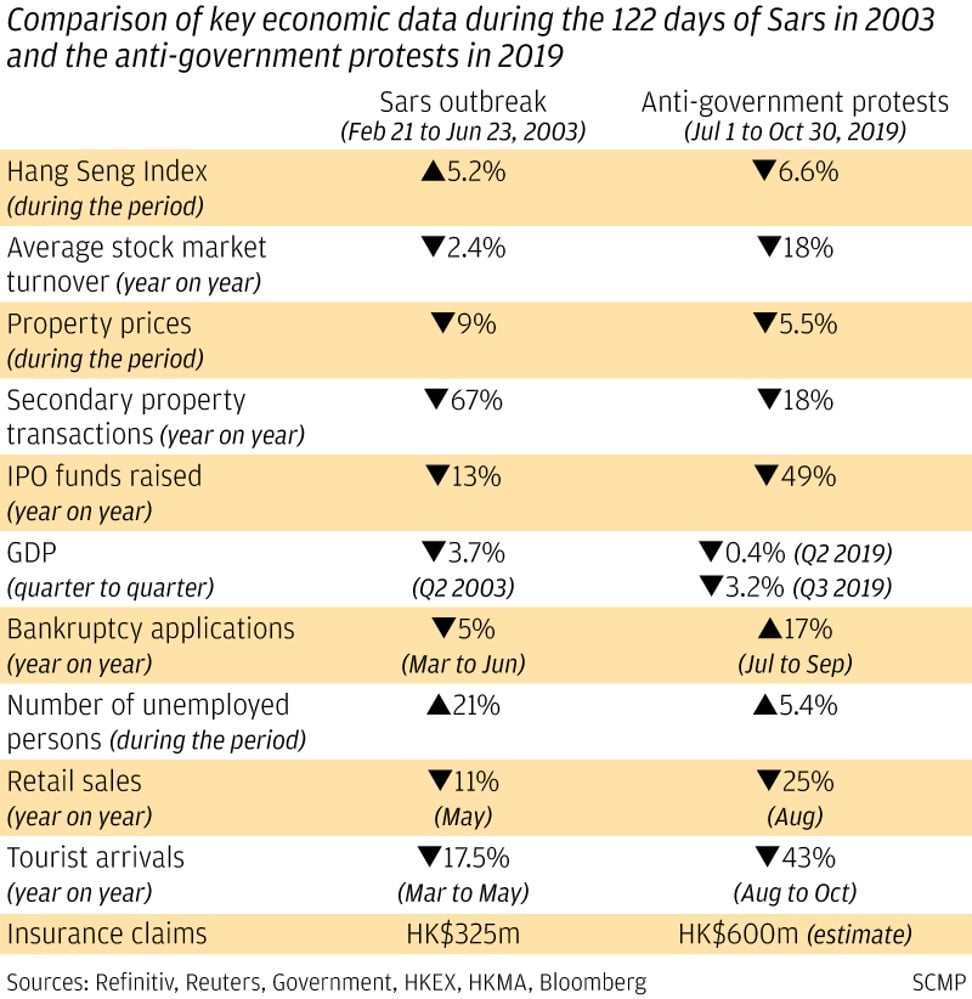

"We are just starting to enter a down cycle, unlike the severe acute respiratory syndrome [outbreak in 2003] when we were coming to the end of the down cycle since 1997," said JLL's head of Greater China and Hong Kong research Nelson Wong, adding that he expects prices in the mass-market and mid-market segments to drop by 10 to 15 per cent this year. That could generate interest in buyers, he said.

SCMP Graphics alt=SCMP Graphics

Hong Kong's home prices slipped 6.5 per cent in February from its August 2018 peak before the city was engulfed by anti-government protests, according to a property price index compiled by real estate agency Midland Realty. In comparison, home prices plunged by as much as 70 per cent during the 2003 Sars outbreak from their 1997 peak.

Hong Kong's current shortage of land and homes, combined with the backdrop of declining interest rate and easier mortgage rules, could provide a strong support for home prices said Alva To, Cushman's vice-president and head of consulting for Greater China.

Declining home prices may find a floor if the current Covid-19 outbreak stabilises by June or July, according to a forecast by Savills, adding that first-half transactions may drop 10 per cent to 22,720 from the second half of 2019.

In the luxury segment, local and mainland Chinese high net worth individuals have "virtually stopped all dealings" and opted to diversify in overseas markets, Savills said in February. These potential buyers are likely to turn cautious on investment as business prospects and economic conditions weaken in Hong Kong, which would pull luxury prices down by another 5 to 10 per cent for the year.

This article originally appeared in the South China Morning Post (SCMP), the most authoritative voice reporting on China and Asia for more than a century. For more SCMP stories, please explore the SCMP app or visit the SCMP's Facebook and Twitter pages. Copyright © 2020 South China Morning Post Publishers Ltd. All rights reserved.

Copyright (c) 2020. South China Morning Post Publishers Ltd. All rights reserved.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Subscribe to our newsletter

Search Articles