Private home prices up 1.4% q-o-q in 1Q2024 even as sentiment turns cautious

By Nur Hikmah Md Ali

/ EdgeProp Singapore |

The price increase in 1Q2024 was led by the prime non-landed market, which rose 3.4% q-o-q (Photo: Samuel Isaac Chua/EdgeProp Singapore).

Private housing prices rose 1.4% q-o-q in 1Q2024, slowing from the 2.8% increase in 4Q2023, according to URA data released on April 26. "The current market upcycle is 27 quarters, which is the longest streak since the start of the price index in 1995," says Lee Sze Teck, senior director of data analytics, Huttons Asia. "As of 1Q2024, property prices have appreciated by 49.6% since the trough in 2Q2017."

The price increase in 1Q2024 was led by the prime (Core Central Region) non-landed market, which rose 3.4% q-o-q. In comparison, the suburban (Outside Central Region) and city fringe (Rest of Central Region) markets grew by a marginal 0.2% and 0.3%, respectively.

According to Huttons’ Lee, homebuyers are increasingly stratified into two groups. The first group of buyers are on the hunt for space and are willing to pay more for a large unit. The landed housing market saw prices rise 2.6% in 1Q2024, while CCR non-landed prices rose 3.4% last quarter.

A total of 23 terraced houses have been sold at Bukit Sembawang's Pollen Collection in the first four months of 2023 (Photo: Samuel Isaac Chua/EdgeProp Singapore)

Bukit Sembawang's landed housing project Pollen Collection sold 17 terraced houses at an average of $3.7 million each, with an average land size of 1,724 sq ft. Based on caveats lodged as at April 26, 23 houses have been sold to date.

In the CCR, 19 Nassim, Klimt Cairnhill, and Watten House topped the table with the highest sales in the non-landed segment. Keppel's 101-unit, 19 Nassim, which obtained its Temporary Occupation Permit (TOP), recently saw strong interest from buyers looking for large units and an address in the prestigious Nassim enclave. The 138-unit, freehold Klimt Cairnhill by Low Keng Huat and the 180-unit, freehold Watten House by a joint venture between UOL Group and Singapore Land Group similarly attracted buyers for its larger units and coveted address.

The second group of buyers, says Huttons' Lee, is quantum-sensitive and looking for a non-landed home with a budget of around $2 million. "It is the sweet spot for many first-time homebuyers and HDB upgraders," he adds.

Lentor Mansion sold more than 400 units or 76.5% of its units in March 2024 (Photo: Samuel Isaac Chua/EdgeProp Singapore)

Launch sales

In 1Q2024, developers launched 1,304 units for sale and sold 1,164 units. The number of units sold in 1Q 2024 is 6.6% higher than the previous quarter but 7.3% lower than a year ago.

The first two launches of 2024, the 341-unit Hillhaven by Far East Organization, and the 172-unit The Arcady at Boon Keng by a consortium made up of KSH Holdings, SLB Development and Ho Lee Group, sold a combined total of 111 units in January. It brought the tally for developers’ sales for the first month of the year to 304 units. "It is the lowest January sales since 2009, reflecting the cautious sentiment among buyers," says Huttons' Lee.

February 2024 was a quiet month with no new project launches due to the Chinese New Year (CNY) period. In March 2024 after the CNY, four projects were launched: the 35-unit, freehold Ardor Residence by Nanshan Group on Haig Road in the east, the 17-unit freehold Koon Seng House by Macly Group, the 533-unit Lentor Mansion by GuocoLand and 267-unit Lentoria by TID, a joint venture between Hong Leong Holdings and Mitsui Fudosan.

"Lentor Mansion was a runaway success, selling more than 400 units or 76.5% of its units in March 2024, making it the best-selling project in 2024 in terms of number of units sold and in percentage terms," says Huttons' Lee. "The efficient and compact layout led to an attractive quantum. Almost 75% of the units sold were below $2 million."

At the 267-unit Lentoria, 60 units were sold in March 2024, mainly attracting owner-occupiers (Photo: Samuel Isaac Chua/EdgeProp Singapore)

Lentoria sold 60 units in March 2024, mainly attracting owner-occupiers, probably because of the exclusive private residential enclave and proximity to CHIJ St. Nicholas' School, Lee adds.

In 1Q2024, all the top-selling projects were in the RCR and OCR, primarily driven by local demand (See Table for Top 10 Best-Selling Projects).

Resale volume and transaction prices

Source: URA, Huttons Data Analytics

Transaction volume in the resale market fell by 5% q-o-q in 1Q2024 to 2,689 units, from 4Q2023's 2,831 units. According to URA data, resale transactions made up 63.6% of total transactions in 1Q2024, a lower proportion than the 65.3% in 4Q2023 on higher new sales.

"Expectations of a cut in interest rate in the coming months led to some buyers waiting on the sidelines," says Huttons Lee. "The high interest rates and soft economic sentiments capped buyers' appetite and willingness to pay more. Median prices of resale private residential units inched up by 0.7% in 1Q 2024."

Besides the tentative market conditions, the drop in resale volume was also due to a mismatch in price expectations between buyers and sellers, says Chia Siew Chuin, JLL head of residential research.

The most expensive non-landed units in 1Q2024 were two 3,057 sq ft units in The Ritz-Carlton Residences, sold for $16.5 million each (Photo: Samuel Isaac Chua/EdgeProp Singapore)

Foreign buying level – lowest since 1995

According to Huttons, 34.9% of the transactions in 1Q2024 were priced below $1.5 million, 24.6% between $1.5 million to $2 million and 40.4% above $2 million.

Singaporeans and Permanent Residents (PRs) made up 98.7% of homebuyers in 1Q2024, while foreigners accounted for 1.3%, deterred by the doubling in additional buyer's stamp duty (ABSD) to 60% imposed in April 2023.

While still low at 1.3%, Huttons' Lee notes a pick-up in transactions in March 2024, with 22 purchases made. It showed a sharp increase from eight in February and 13 transactions in January. Lee attributes the increase to the rise in interest during the CNY period in February, and the rising geopolitical tensions. "Singapore is generally viewed as a safe haven," says Lee. "Some buyers may be willing to pay a premium for their safety."

The top five nationalities purchasing residential property in Singapore in 1Q2024 were from China, Malaysia, India, Indonesia and the US, notes Huttons.

According to PropNex, the proportion of foreign buyers in 1Q2024 is the lowest since 1995. In absolute terms, there were 43 transactions to foreigners in 1Q2024: 22 from the US, five from China, three from Switzerland, two from Norway and 11 unspecified entries.

Amid a pullback in foreign demand, the proportion of Singaporean buyers rose to 82.4% in 1Q2024 from 81.8% the previous quarter. PRs made up 16.4% of the transactions, on par with 4Q2023, notes PropNex.

The most expensive non-landed units in 1Q2024 were two 3,057 sq ft units in The Ritz-Carlton Residences, sold for $16.5 million each. The two units were purchased by Yuan Yonggang, chairman of Suzhou Dongshan Precision Manufacturing Co., and the other by his wife, Wang Wenjuan, who are both Singapore PRs. The $5,307 psf achieved is also the highest psf price for the project.

While the level of unsold stock in the CCR was relatively stable in 1Q2024, the RCR and OCR recorded quarterly increases in unsold inventory of 22.3% and 29.8%, respectively (Photo: Samuel Isaac Chua/EdgeProp Singapore)

Unsold inventory climbs

Owing to slower new home sales at new private residential project launches, unsold inventory of uncompleted units climbed to 19,936 in 1Q2024 from 16,929 units in 4Q2023, notes Tricia Song, CBRE head of research for Singapore and Southeast Asia. Including completed units, unsold inventory increased 17% to 20,204 units in 1Q2024 from 17,262 units in 4Q2023.

While the level of unsold stock in the CCR was relatively stable in 1Q2024, the RCR and OCR recorded quarterly increases in unsold inventory of 22.3% and 29.8%, respectively, according to JLL's Chia.

"Unsold inventory remains low compared to the 10-year annual average of 23,369 units," says Wong Xian Yang, Cushman & Wakefield (C&W) head of research for Singapore and Southeast Asia. "As more launches enter the market in 2024 amid cautious buying sentiments, unsold inventory is expected to rise further."

The last peak in unsold inventory was 37,799 units recorded in 1Q2019, notes CBRE's Song. The 20,204 units in 1Q24 are equivalent to more than two years of landbank -- based on the five-year annual average new home sales of 9,288 units between 2019 to 2023, she points out.

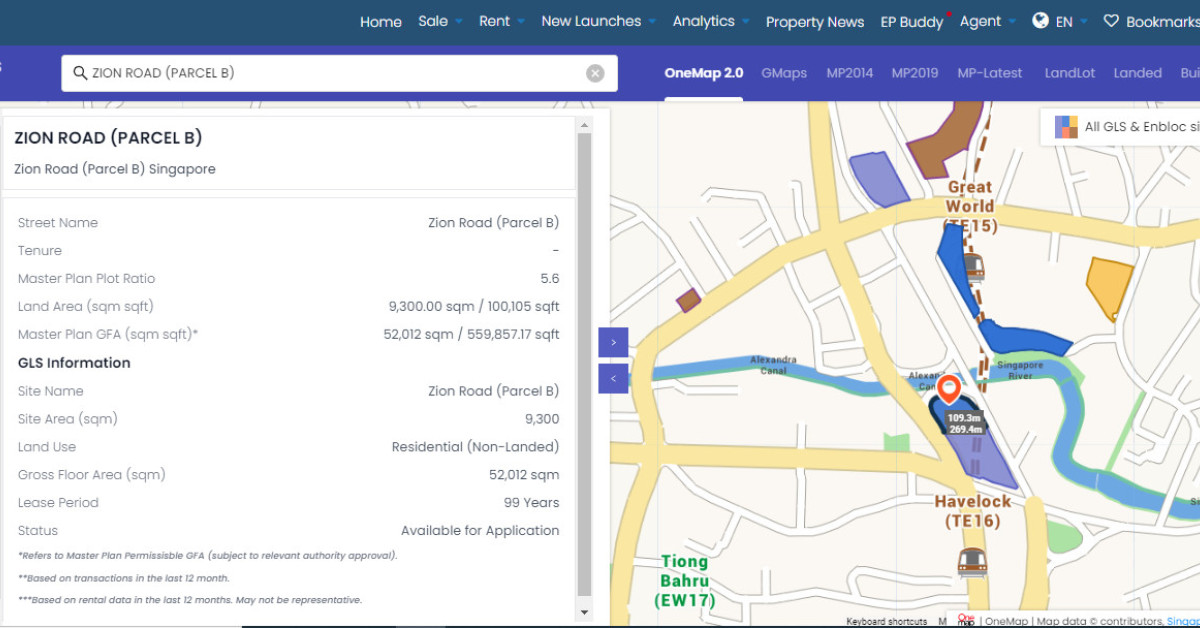

The release of the Zion Road (Parcel B) reserve list site, which was recently triggered, highlights underlying developer confidence towards acquiring select sites with strong locational attributes and good future market demand. Parcel A next door was sold to a joint venture between City Developments and Mitsui Fudosan for $1.107 billion earlier this month (Photo: Samuel Isaac Chua/EdgeProp Singapore)

Caution in developers’ bids at GLS tenders

While the current level is still significantly lower than the last peak, Song observes that the ramp-up in the Government Land Sales (GLS) confirmed list supply, coupled with the slowdown in developer sales over the past two years, is impacting the market.

C&W's Wong found that in 2024 YTD, around two bids were received per GLS residential site launched for tender, lower than the average of three bids in 2023 and four in 2022.

Caution prevailed among developers during recent GLS tenders such as Zion Road, Upper Thomson, Media Circle and Orchard Boulevard, which received fewer than expected bids and fetched lower bid prices compared to past tenders within similar localities, says Wong.

"Despite low levels of unsold inventory, developers remained selective in their site acquisition activities, with a preference for smaller to medium-sized sites or sites with low future market competition,” he adds.

However, the release of the Zion Road (Parcel B) reserve list site, which was recently triggered, highlights underlying developer confidence towards acquiring select sites with strong locational attributes and good future market demand, according to Wong.

Amid a higher pipeline this year, new launches are expected to be priced competitively. C&W's Wong expects private residential prices to grow by up to 3% in 2024, easing from 6.8% y-o-y growth in 2023. "We expect local demand for private housing to remain resilient, supported by still-low unemployment rates, upgrading aspirations, as resale HDB prices continued to increase by 1.8% q-o-q in 1Q2024, and strong household balance sheets," he says.

However, affordability continues to be weighed down by still-high interest rates and elevated housing prices. he adds.

The 440-unit Sora on Yuan Ching Road in Jurong West, fronting Jurong Lake Gardens, will be one of the major launches coming onstream in 2H2024 (Photo: Samuel Isaac Chua/EdgeProp Singapore)

Launches ahead

Ismail Gafoor, CEO of PropNex, expects home sales to pick up in 2H2024 when more launches come onstream. They potentially include larger projects such as the 440-unit Sora on Yuan Ching Road by SingHaiyi Group and KSH Holdings, the new 840-unit project at Jalan Tembusu Parcel B by Sim Lian Group, the 916-unit The Chuan Park and the 1,190-unit mixed-use development at Tampines Avenue 11, by a joint venture between CapitaLand Development and UOL Group-Singapore Land Group.

"Larger developments will offer buyers a wider selection of units, and we anticipate healthy interest for the upcoming launches this year, mainly from Singaporean first-time homebuyers as the ABSD measure continues to stymie investment demand from foreigners," says Gafoor.

With home sales going to be driven primarily by local buyers, developers have adjusted to the new market realities, notes Gafoor. He sees it manifested in developers' more conservative bids for GLS sites and pricing of units at new launches, aware that local homebuyers are more price-sensitive than foreign investors.

In 1Q2024, the median transacted price of new non-landed private homes (excluding ECs) was $1.96 million, down from about $2.15 million in the previous quarter, notes PropNex. Gafoor, therefore, expects private home prices to remain relatively resilient, increasing by 4% to 5% by the end of 2024, with private developer's home sales hovering at 7,000 to 7,500 units.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Subscribe to our newsletter

Related Articles

Top Articles

Search Articles