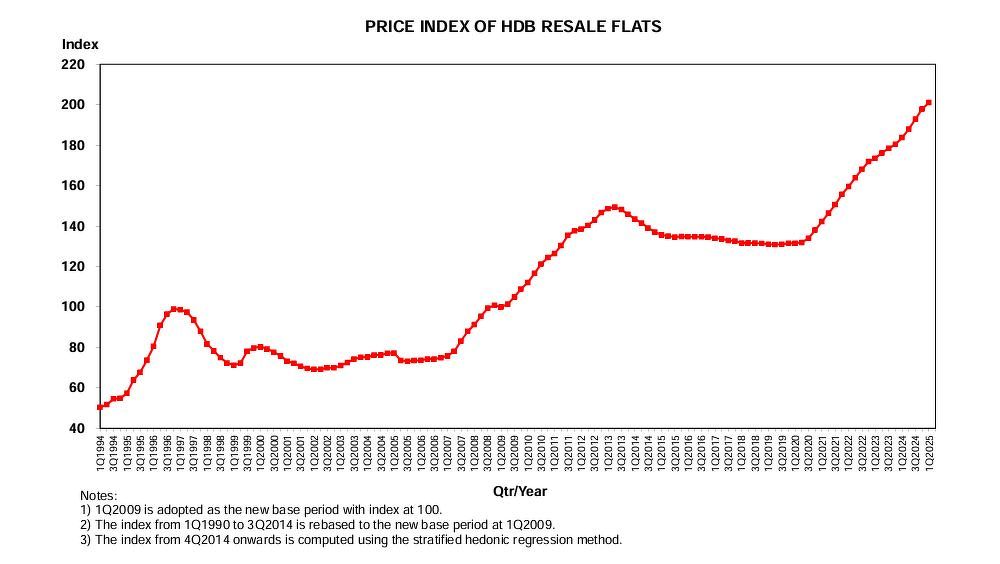

HDB resale prices showed signs of stabilizing in 1Q2025, rising just 1.6% q-o-q in 1Q2025, compared to 2.6% in 4Q2024. It marks the slowest quarterly price increase in over a year since the sluggish 1.1% rise recorded in 4Q2023.

The slower price growth could be the result of the February 2025 Sale of Balance Flats (SBF) exercise which saw a record 5,500 flats offered for sale, says Lee Sze Teck, senior director of data analytics at Huttons.

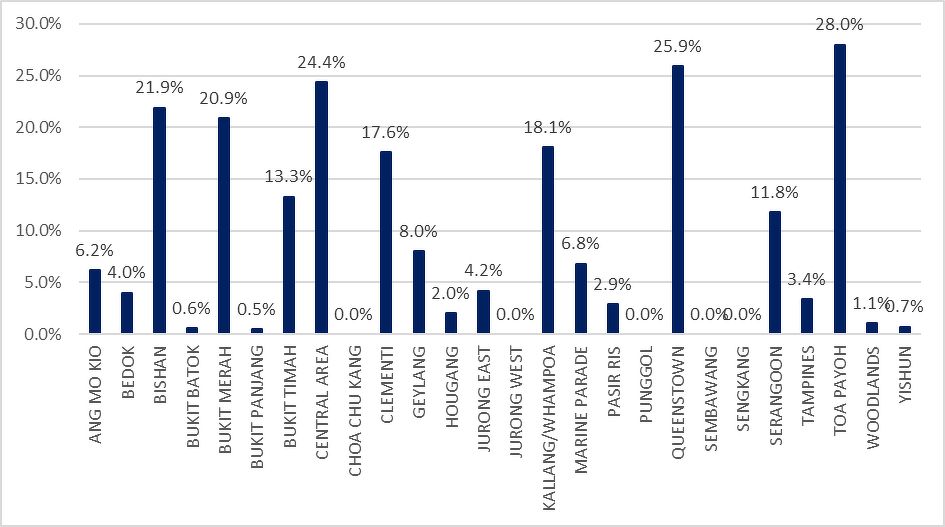

The first three months of the year saw 19 out of 25 HDB towns recording price gains. Clementi saw the highest q-o-q price spike of 15.4%, followed by Marine Parade (7.2% increase) and Bukit Merah (6.2% increase).

However, the gains were smaller than the highest gains recorded in 4Q2024 such as Central Area (25.6% increase) and Toa Payoh (12.1% increase), notes Christine Sun, chief researcher and strategist at OrangeTee Group.

She also notes that price declines in 1Q2025 were also considerably larger, with the biggest falls in the Central Area (18.5 decrease) and Geylang (7% decrease). The steepest declines of 4Q2024 were seen in Ang Mo Kio, which saw a more modest fall of 5% in prices.

“The price trends are an indications of increasing price resistance among buyers,” adds Sun. “The market may experience slower price growth in the upcoming months.”

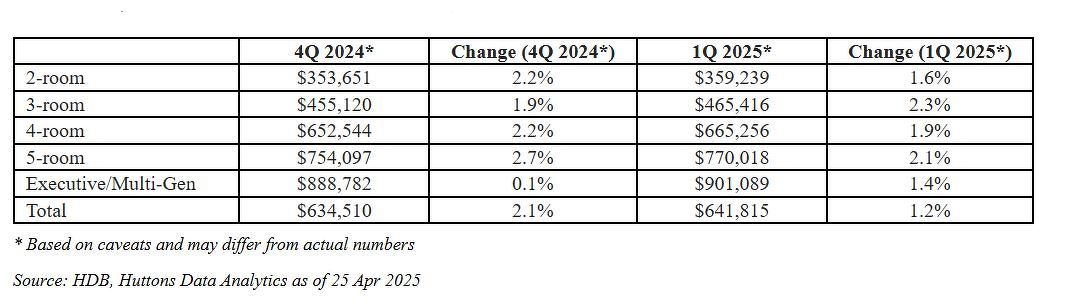

By room type, three-room units saw the highest growth in 1Q2025 with average prices rising 2.3% q-o-q from $455,120 in 4Q2024 to $465,416 in 1Q2025. Five-room units also saw notable growth of 2.1%, followed by four-room units which saw average prices rise 1.9% in the quarter.

Multi-gen and Executive units saw the slowest quarterly price growth of 1.4%, followed by two-room units at 1.6%, according to HDB caveats.

“Since allowing singles to apply for two-room flexi Build-To-Order (BTO) flats in all locations from Oct 2024, the demand had shifted away from smaller units in the secondary market,” notes Huttons’ Lee.

Change in Average Prices of HDB Resale Flats in 1Q 2025

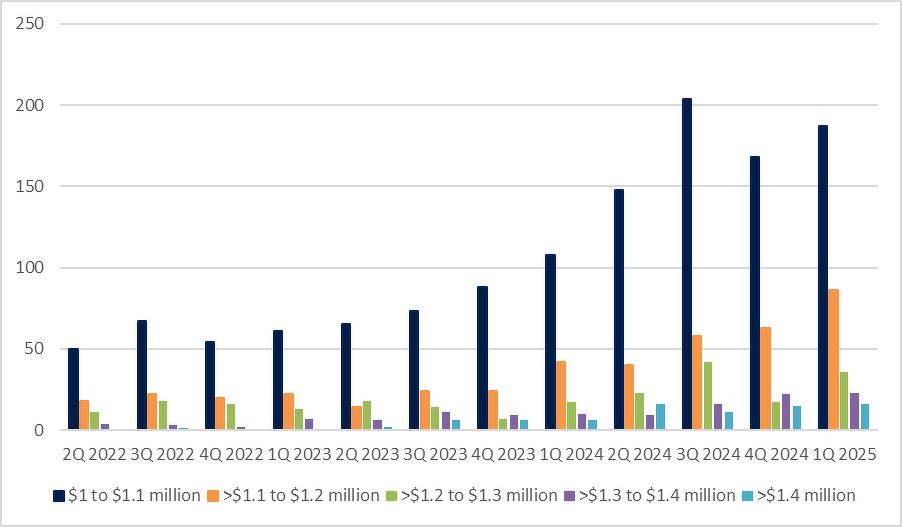

Despite the moderated overall price growth in 1Q2025, an estimated 348 HDB resale flats were sold for seven-figures, marking a 22.1% increase over the previous quarter and making it the highest number ever sold in a single quarter.

Breakdown of million-dollar flats by price range (Source: HDB, Huttons Data Analytics as of 25 Apr 2025)

According to Huttons’ Data Analytics, 57 such transactions were units that had just reached their Mandatory Occupation Period (MOP) of five years. This exceeds the number of five-year-old million-dollar resale flats sold in whole of 2024.

“This is probably due to the number of centrally located HDB estates fulfilling their MOP period such as those along Alkaff Crescent, Bidadari Park Drive, Circuit Road, Dawson Road and St George’s Lane,” says Lee.

Over 90% of million-dollar transactions were in mature estates with Toa Payoh recording the highest number of million-dollar flats sold in the quarter at 68. Bukit Merah took the silver medal with 53 flats and Queenstown rounded out the top three with 42 flats.

Overall, million-dollar flats made up around 5.3% of total transactions for 1Q2025.

"PropNex expects the number of million-dollar resale flats sold to exceed 1,000 units again this year, as such flats – typically with very desirable attributes – are seen to offer more bang for buck versus comparable private homes in the same area, particularly among more price conscious buyers who may have a smaller housing budget," says Wong Siew Ying, head of research and content at PropNex Realty.

Proportion of million-dollar flats by township in 1Q 2025 (Source: HDB, Huttons Data Analytics as of 25 Apr 2025)

HDB resale transactions rose by 2.6% from 6,424 cases in 4Q2024 to 6,590 cases in 1Q2025, according to data released by HDB. On a yearly basis, transaction volumes fell 6.8% from the 7,068 cases recorded in 1Q2024. It is also the lowest first quarter number since 2020.

Despite the dip in yearly sales, OrangeTee’s Sun considers the overall performance of the resale market ‘remarkable’.

“The resale market faced intense competition from the primary market as HDB introduced more than 10,000 new flats across the BTO and SBF sales exercises in February 2025,” she adds.

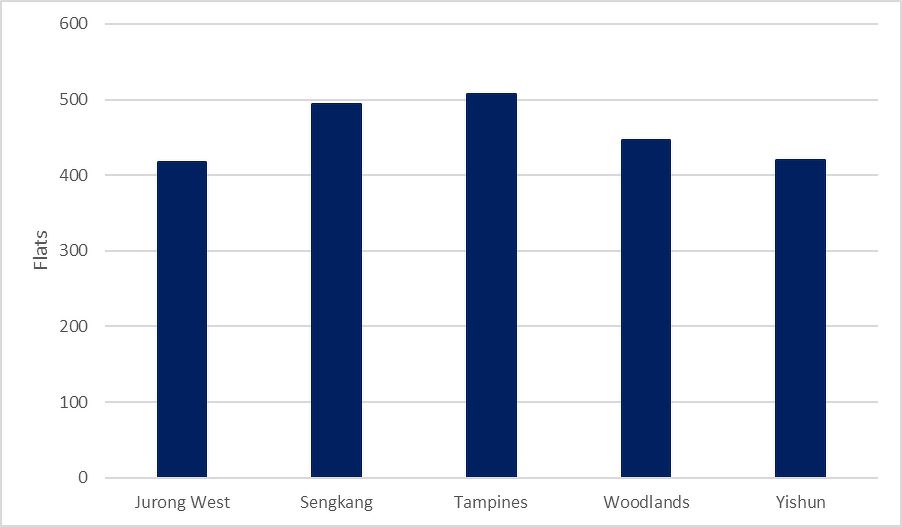

The five-most popular HDB towns among buyers in 1Q2025 were Tampines, Sengkang, Woodlands, Yishun and Jurong West. Together, they accounted for 36.2% of total transactions in 1Q2025.

Top Five most popular HDB Towns among buyers in 1Q 2025 (Source: HDB, Huttons Data Analytics as of 25 Apr 2025)

1Q2025 saw a 12.3% rise in approved rental applications, from 8,603 units in 4Q2024 to 9,662 in the first three months of this year. Year-on-year, rental applications rose 2.8 per cent from 9,398 units.

“Rental demand usually picks up after the year-end holidays and festive season,” observes Sun. “Recently, there has been a noticeable rise in foreign students and expats returning to Singapore. Some landlords were also more flexible and open to negotiate rents, given the intense competition for tenants from the private rental market.”

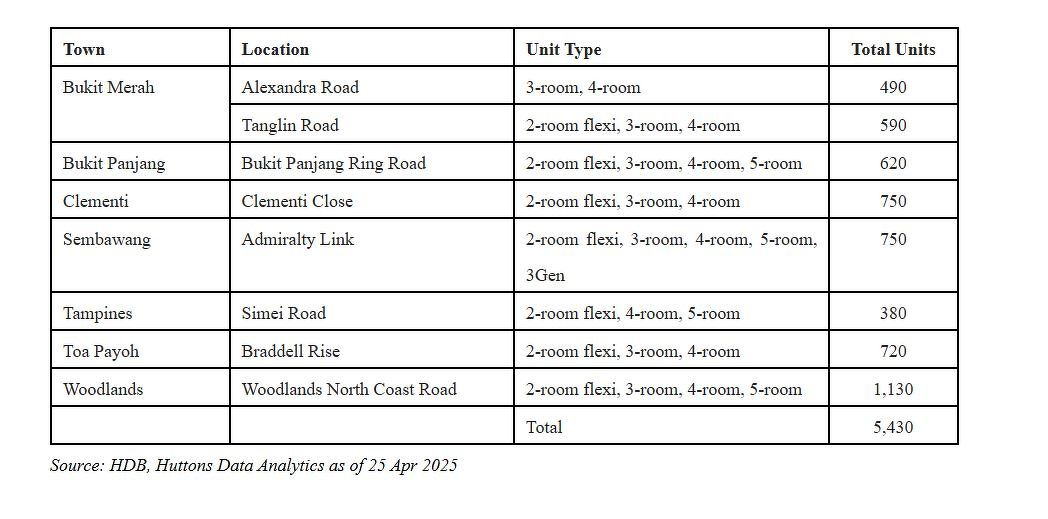

In July, HDB will launch about 5,400 BTO flats in Bukit Merah, Bukit Panjang, Clementi, Sembawang, Tampines, Toa Payoh, and Woodlands. HDB will also be conducting a concurrent SBF exercise offering about 3,000 flats. This brings the total SBF supply this year to about 8,500 flats, the largest since 2017.

This is in line with HDB’s target of launching 50,000 BTO flats from 2025 to 2027, including the 19,600 BTO units slated to be launched this year.

BTO Launches in Jul 2025

“The HDB resale market is expected to remain tight for the rest of 2025,” opines Lee. However, with the fresh supply of resale flats limited and no BTO or SBF exercise set to launch in 2Q2025, prices may begin to pick up.

However, the mid-term outlook is still dependant on several external factors such as sustained elevated interest rates, job security, household income growth and how the ongoing trade war might escalate, notes OrangeTee’s Sun.

“Amid an atmosphere of heightened caution, many potential buyers may exercise greater restraint to avoid overstretching their budgets,” she adds.

Meanwhile, over the long term, the supply of newly MOP units is expected to increase over the next two years. Around 8,000 flats are expected to reach the Minimum Occupation Period (MOP) in 2025, 13,500 in 2026, and 19,500 in 2028.

“The increase in MOP supply may alleviate pressure on resale prices, especially for flats in mature estates or central locations, which continue to experience strong demand among home buyer,” says Eugene Lim, key executive officer at ERA Singapore.

Lim anticipates HDB resale prices to rise at between 3-6% with 26,000 to 27,000 resale HDB flat transactions by the end of 2025. Huttons’ Lee has a more optimistic forecast with prices rising between 5-8% over a similar number of transactions. PropNex's Wong concurs, projecting a price increase of 5-7% over the year.

")

(1).jpg?cFDFBuYaczaPAqQpcbRxTSsSUPGGP.Bv&itok=K31QTGdR "HDB has announced changes to its processes for assessing flat buyers’ incomes and eligibility for housing subsidies, effective May 9 (Picture: Samuel Isaac Chua/The Edge Singapore)")

")