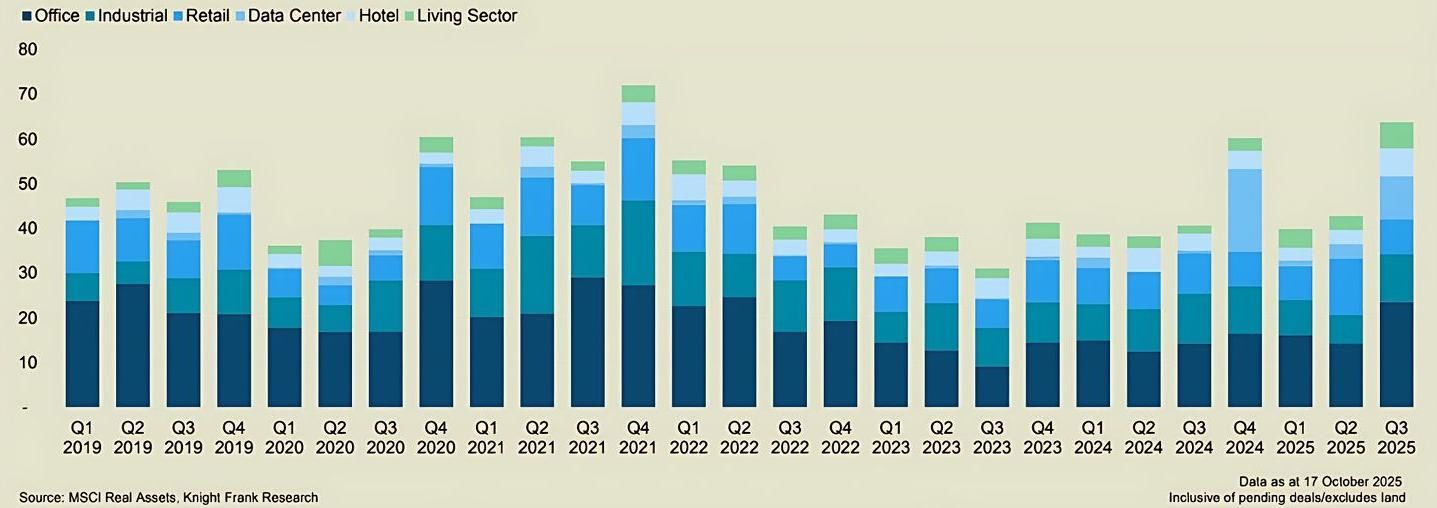

In 3Q2025, Asia Pacific commercial real estate investment volumes hit a record high of US$63.8 billion ($82.65 billion), marking a 56.8% y-o-y rise from 3Q2024. On a quarterly basis, investment activity within the region surged by 49.1%, says Knight Frank in its Asia-Pacific Capital Markets Insights report released on Oct 28.

The agency attributes the surge in commercial real estate investment to several large entity-level transactions and the completion of deals after extended due diligence periods.

"3Q2025’s record US$63.8 billion transaction volume marks a genuine market revival in Asia Pacific, driven by policy clarity and capital rate stabilisation,” says Christine Li, head of research of Asia-Pacific at Knight Frank. “Investors are shifting from cap rate compression strategies to external factors such as active asset management and income growth.”

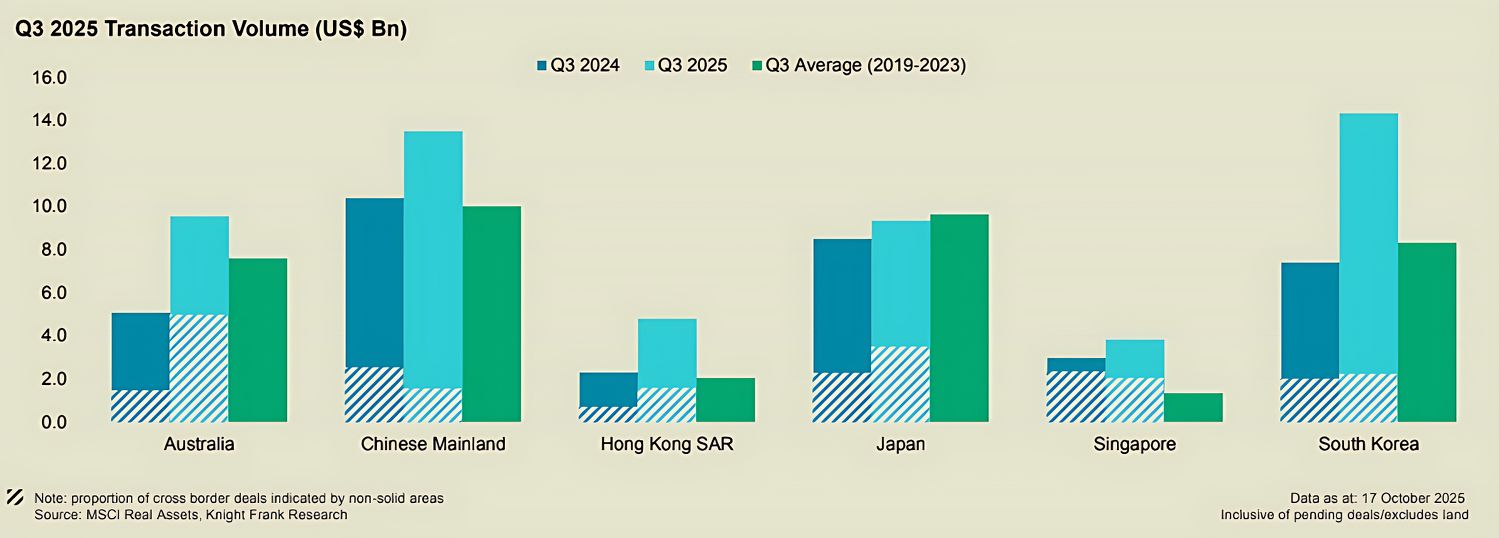

During the quarter, cross-border investment in the region reached US$17.8 billion, rising 72.1% q-o-q and 28.6% y-o-y, underscoring Asia Pacific’s renewed attractiveness to global investors, says Knight Frank.

This was led by Australia, which saw the highest volume of cross-border capital at US$5.0 billion, mainly targeting the living and industrial sectors. This was followed by Japan with US$3.5 billion, concentrated in office and multi-family assets, while South Korea saw US$2.3 billion in cross-border investments, primarily invested in industrial and office properties.

“What is particularly encouraging is the breadth of activity,” notes Dan Dixon, head of capital markets for Asia-Pacific at Knight Frank. “We see strong deal flow across offices, industrial, and living sectors, reflecting genuine structural demand rather than opportunistic plays."

Overall, investment activity rose across the majority of asset classes in 3Q2025, with office transactions at the forefront, totalling US$23.7 billion in investment volume. This marked a 64.2% y-o-y increase. Knight Frank anticipates further growth in office rental and capital values, driven by limited new supply in key CBD locations.

Hotel transactions also saw an uptick of 67.7% y-o-y, posting investment volumes of US$6.2 billion within the quarter.

That said, industrial and retail volumes declined 3.7% y-o-y and 13.4% y-o-y in 3Q2025, respectively, as investor sentiment remained cautious amid global trade uncertainties.

In terms of growth, South Korea led the region, recording a 93.6% y-o-y increase to US$14.3 billion in transactions. This was driven by office assets, which accounted for 70.9% of the country’s total investment volume. Notable transactions include the acquisition of Pangyo Tech One Tower, which achieved a record transaction price of US$1.42 billion.

The Chinese mainland secured second place with US$13.5 billion in investment volume, up 29.9% y-o-y. Data centres accounted for one-third of total volume activity, following Bain Capital’s divestment of data centre operator WinTriX DC Group’s Chinese mainland business to a consortium led by Guangdong Hec Technology for US$3.9 billion.

Meanwhile, Singapore posted US$3.8 billion in investment capital, up 28.6% y-o-y. According to Knight Frank, this was led by the completion of several large-scale transactions. This included the sale of Jem’s office component by Lendlease Global Commercial REIT, which was sold for US$356 million to Keppel Land.

Singapore posted US$3.8 billion in investment volume, up 28.6% y-o-y, driven by the completion of several large-scale transactions. Key transactions included Lendlease Global Commercial REIT’s US$356 million sale of Jem’s office component to Keppel Land, and UOL Group’s US$292.3 million divestment of Kinex to Kinex Times Square and Xiaohong Property Management.

Looking ahead, the agency expects investment momentum across the region to remain steady in 4Q2025, boosted by “clearer monetary policy direction and improved liquidity”.

Despite dampening investor sentiment following recent US tariffs on China, the performance in 3Q2025 reflects underlying market strength, says Knight Frank.

Li notes that industrial and retail sectors may encounter near-term headwinds due to upcoming policy changes.

“Amid this capital re-allocation phase, Japan stands out as a policy-anchored beneficiary,” she adds. “Its yield spreads remain comparatively attractive, and despite gradual monetary tightening, rental fundamentals are supported by sustained urbanisation.” Li highlights that international investors are increasingly drawn to multifamily and logistics assets in Greater Tokyo and Osaka, supported by the country’s inflation-hedging traits and relative stability amid a volatile global environment.