Economic headwinds may moderate industrial rents in 2020

Ask Buddy

SINGAPORE (EDGEPROP) - Industrial real estate rents in Singapore were generally stable in 2019, although the sector was weighed down by oversupply from preceding years, says Christine Li, head of research, Singapore and Southeast Asia, at Cushman & Wakefield (C&W).

Tricia Song, head of research for Singapore at Colliers International, agrees. She says that compared to 2018, the overall industrial property market has shown “clearer signs of stabilisation, with both rents and vacancy rates remaining relatively stable in the year to September”. Both net demand and net supply are expected to have increased in 2019.

But looking ahead, Li says the industrial outlook for 2020 could be gloomier compared to this year. She says global macroeconomic factors, such as slowing economic growth in the US, the EU and China, is likely to have a negative impact on Singapore’s economy in 2020. The subdued global economy is expected to moderate industrial rents next year, she adds.

Newly completed industrial space doubles in 2019

This year, close to 12.5 million sq ft of net new industrial space is expected to have been completed, which is more than twice the 5.84 million sq ft of net new completions in 2018, says Song. Net new demand is also expected to have increased by 50% y-o-y to 11.0 million sq ft in 2019, she adds.

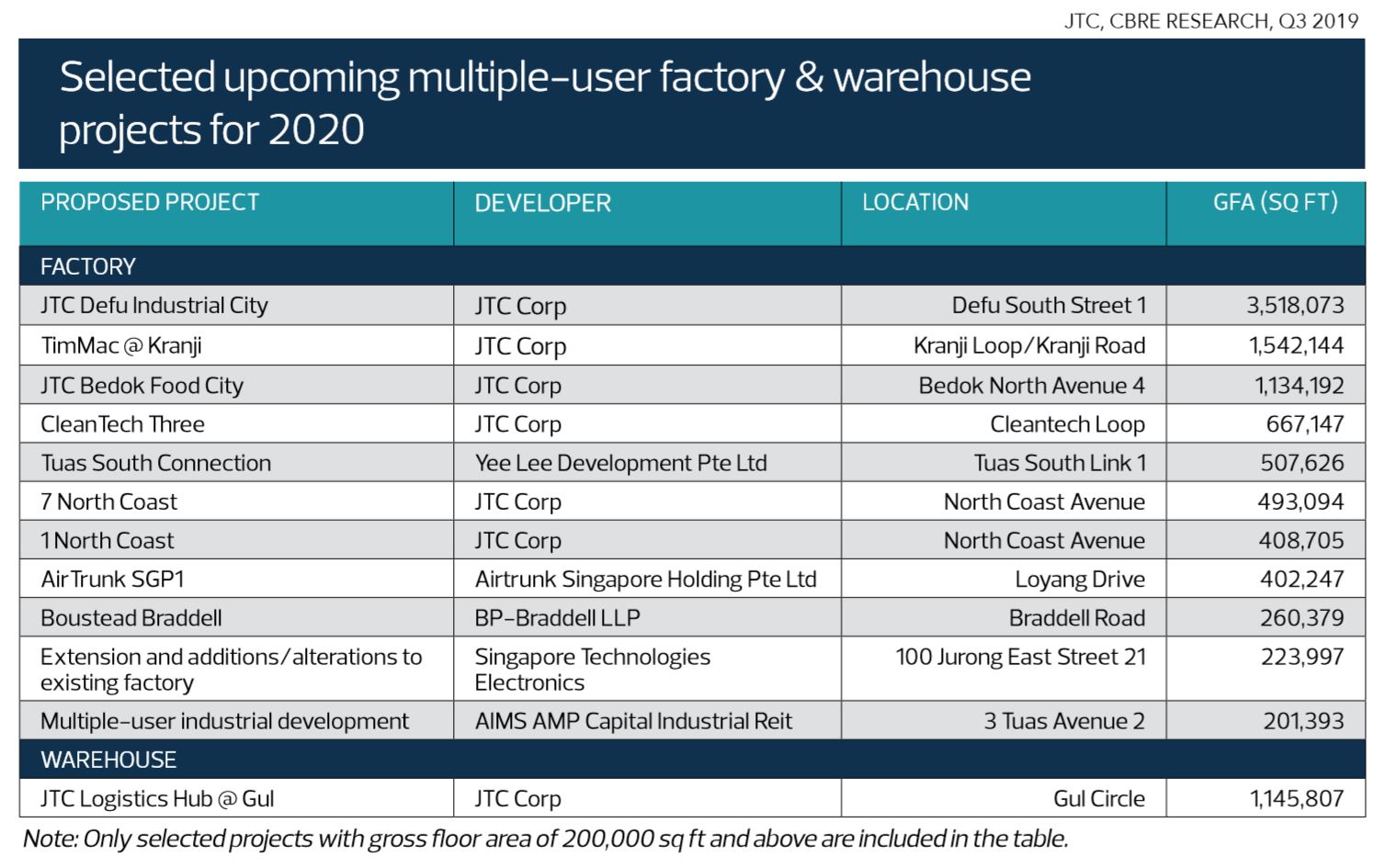

For 2020, the largest new industrial development that will be completed is the Defu Industrial City at Defu Street 1. JTC’s flagship stackup complex at Defu Industrial Park will have a total gross floor area (GFA) of 3.52 million sq ft. Other sizeable new industrial developments in 2020 include JTC’s TimMac @ Kranji boasting 1.54 million sq ft in GFA, and JTC Bedok Food City with 1.13 million sq ft in GFA.

Over in the one-north business park district, homegrown gaming hardware company Razer is expected to open its purpose-built, 207,743 sq ft headquarters building next year, while ride-hailing giant Grab is due to move into its 387,000 sq ft purpose-built headquarters building by 4Q2020.

Two-tier leasing performance in factory segment …

Based on CBRE Research’s basket of industrial properties, factory and warehouse rents remained steady at $1.57 psf per month (pm) and $1.58 psf pm respectively in 4Q2019. “Looking ahead, warehouse rents are expected to be more resilient, supported by a tight supply pipeline,” says Desmond Sim, head of research, Southeast Asia, at CBRE.

But he adds that industrial occupiers were looking for premises with higher specifications and better efficiency. This contributed to a two-tier leasing performance by the factory segment in 2019, as industrial developments with higher specifications outperformed older, conventional industrial buildings.

“The 10.5% vacancy [in the factory segment] in 3Q2019 included a growing pool of vacant, ageing industrial stock of about 53.85 million sq ft. This spurred several landlords to undertake asset enhancement initiatives on older industrial stock in a bid to unlock value by repositioning and redeveloping assets with under- utilised gross floor area,” he says.

According to Colliers, these enhancements include increased power capacities, high-floor loading capability, modern ventilation and cooling systems, higher ceilings and better loading bay facilities. Redevelopment could also enhance connectivity between adjacent buildings and to transportation nodes.

According to Song, landlords feel it is the right time to adopt smart features such as automation and artificial intelligence to improve productivity and space efficiency, and reduce operating costs.

In general, leasing demand in 2019 was driven by renewals and relocations of companies in the third-party logistics, high-tech manufacturing, and chemicals sectors. The electronics sector took a backseat in 2019 when the US-China trade war escalated, and the sector was also hit by an economic dispute between Japan and Korea, CBRE’s Sim says, adding that some industrialists are taking a cautionary stance and limiting expansion plans.

According to Colliers, third-party logistics companies, transport agencies, e-commerce, and manufacturing companies were the top occupiers of warehouse logistic spaces this year. Companies in these sectors accounted for close to 74% of occupied islandwide warehouse space.

… as well as business parks segment

High-spec premises such as business parks also recorded a two-tiered leasing performance in 2019 as the market split between city-fringe and suburban submarkets. City-fringe business park rents climbed 0.9% y-o-y to $5.85 psf pm, but suburban rents fell by 1.3% y-o-y to $3.75 psf pm, based on JTC statistics.

“We continue to see a flight to quality in the business parks sector,” says Colliers’ Song. “We observe that new business park spaces near MRT stations in the city fringe continued to attract healthy demand, while those older and further away from MRT stations located in the suburbs faced more difficulty in finding tenants, despite lower rents.”

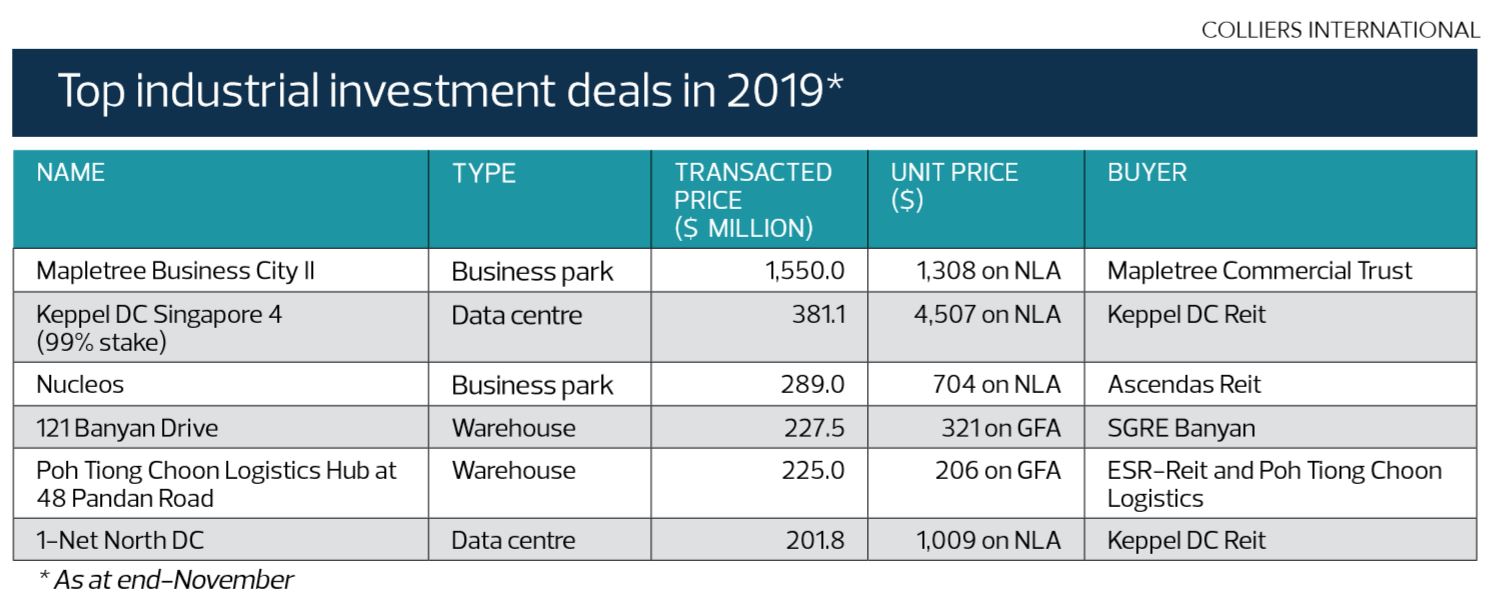

The biggest deal of the year was Mapletree Commercial Trust acquisition of Mapletree Business City II from its sponsor Mapletree Investments for $1.55 billion. (Picture: Samuel Isaac Chua/The Edge Singapore)

She adds that the rent disparity could widen going forward, as centrally-located business parks with good amenities are expected to record rental growth, while rents in older business park spaces could remain flat over the next few years.

C&W’s Li says that “with office rents near the peak, cost-conscious occupiers are choosing to locate at business parks as an alternative to the CBD”. The segment saw improved absorption of 452,000 sq ft during the first three quarters this year, she says.

“The specs of newly completed business parks are almost no different from that of Grade-A offices which can compete for the same tenant pool if such tenants qualify for both business park and office spaces. That could help to put a lid on the rental upside should there be more decentralised office supply in the pipeline,” Li adds.

However, decentralised office supply does not necessarily cannibalise the business park demand, as they offer different specifications, eco-systems and different value propositions for different types of tenants, says Colliers’ Song.

Reits dive into specialised assets

Industrial investment activity has been relatively healthy in 2019, clocking in deals worth about $2.99 billion. The biggest deal of the year, in terms of transacted prices, occurred in November when Mapletree Commercial Trust acquired Mapletree Business City II, a premium campus-style business park development, from its sponsor Mapletree Investments for $1.55 billion.

The second largest deal was in September, when Keppel DC Reit acquired a 99% stake in Keppel DC Singapore 4 for $381.1 million. The Reit also acquired a second data centre, 1-Net North DC, for $201.8 million. In November, Ascendas Reit acquired two business-park properties, Nucleos and FM Global Centre, from its sponsor CapitaLand for a combined value of $380 million.

In April this year, CapitaLand sold the group of companies that own and manage the self- storage business StorHub, for $179.5 million. This comprises StorHub’s portfolio of 12 self-storage properties with a total lettable area of about 800,000 sq ft.

The largest industrial leasing deal in 2019 was Google’s expansion into Alexandra Technopark, taking up 344,100 sq ft (Picture: Samuel Isaac Chua/The Edge Singapore)

Meanwhile, the largest industrial leasing deal in 2019 was Google’s expansion into Alexandra Technopark, taking up close to 344,100 sq ft of industrial space. The development is adjacent to Google’s Asia-Pacific headquarters in Mapletree Business City II.

Another notable leasing deal occurred in January when e-commerce firm Shopee leased all 240,000 sq ft at 5 Science Park Drive, a redevelopment of the former Fleming and Faraday buildings by Ascendas-Singbridge, for its expansion needs.

Read also:

Ask Buddy

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search