Non-landed private home prices fell by 0.1% in second quarter, with 1.4% drop in RCR: flash estimates

Non-landed CCR property prices went up by 2%. Landed homes got 2.6% pricier, reversing from the 0.4% dip previously. (Photo: Samuel Isaac Chua/EdgeProp Singapore)

Overall, Singapore's private homes got 0.5% pricier in the April–June period this year as compared to the previous three months, according to URA’s flash estimates of the 2Q2026 price index for private residential property released on July 1.

The pace of growth has eased from the 0.9% increase in the first quarter, though the volume of sale transactions was broadly comparable.

For non-landed private residential properties, prices decreased by 0.1% in the second quarter, reversing from the 1.3% gain in the previous quarter.

The steepest decline in prices was in the Rest of Central Region (RCR) or city fringe with a 1.4% drop, in contrast to the 0.8% increase in 1Q2026.

Hudson Place Residences was the sole new launch project in the RCR during the quarter. The condo’s median new-sale price of $2,465 psf was 6.5% lower than the six-month RCR median of $2,643 psf, which highlights "underlying demand for affordably priced homes in the city fringe, particularly among young families holding jobs in one of one-north’s emerging industries", said ERA Singapore chief executive Marcus Chu.

In the Outside Central Region (OCR) or suburbs, non-landed home prices inched down by 0.2%, versus the 2.2% rise in the previous quarter.

Tengah Garden Residences’ launch may have contributed to the slightly softer OCR prices, said CBRE head of research for Singapore and Southeast Asia, Tricia Song. As the first private condo launch in Tengah, the project saw overwhelming take-up due to its "attractive pricing" relative to recent OCR launches, she noted.

This also coincided with the HDB resale price index falling for a second consecutive quarter, which may be indicative of weaker upgrading power, Song shared.

On the other hand, prices of non-landed private residential properties in the Core Central Region (CCR) went up by 2%, speeding up from the 0.6% increase in the previous quarter.

On the CCR price gains, Knight Frank Singapore head of research Leonard Tay pointed out that demand for higher-end non-landed homes was contributed by wealth from an increasing buyer pool of citizens and permanent residents, some of whom decided to upgrade from being renters to homeowners.

Despite not having any new launches during the quarter, the CCR outperformed on firm pricing at existing projects River Modern and The Robertson Opus.

Song said that those projects' units traded at higher median prices than in preceding quarters, as buyers scooped up remaining units, "recognising value in these prime projects amid the narrowing price gap between the CCR and RCR/OCR".

More suburban launches, lower-priced sales weighed on price growth

Developers launched three major non-landed projects for sale during the quarter: Hudson Place Residences in Media Circle, Tengah Garden Residences in Tengah, and Vela Bay in Bayshore, during April and May.

These three new launches were "priced sensitively with buyers in mind" and did not breach existing levels already established in the RCR and OCR, Tay said.

As a result, prices of non-landed private homes were stable in 2Q2026 with a slight easing. This is characteristic of the transition from the rapid post-pandemic expansion towards a more sustainable and balanced phase of growth from 2024.

That said, while this stability is positive, "an eye should be kept on private residential development sites awarded by the government as a precursor to probable price increases in the remainder of 2026 and early 2027", Tay added.

Overall, the smaller price appreciation of private homes in Singapore in 2Q2026 could have been due to a higher proportion of sales being in the OCR, said Huttons Asia chief executive Mark Yip.

Nearly 60% of sales during the quarter were in the OCR — the highest proportion since 3Q2015. "Usually, homes in the OCR are more affordable, hence it may have a bigger influence on the price index in 2Q2026," Yip noted.

On the other hand, the proportion of transactions in the CCR, which are often higher priced, dipped to 12.3%, Christine Sun, chief researcher and strategist at Realion (OrangeTee & ETC) Group highlighted.

As more suburban units were transacted in the second quarter, the number of new private homes (excluding ECs) transacted below $2 million rose sharply to 1,016 units, as compared to 631 units in the previous quarter. This may have dragged down the overall price index in 2Q2026, Sun remarked.

And on a psf basis, she noted that the number of new private homes, excluding ECs, that were sold at below $2,000 psf also climbed from 24 units in the first quarter to 144 units in the latest quarter this year.

Landed property values could grow further

Meanwhile, landed homes saw prices climbing 2.6% in the latest three months, reversing from the 0.4% dip in the previous quarter.

This is now the highest the landed price index has ever been. Knight Frank expects activity to remain "fairly resilient" with most deals closing within the $5 million to $10 million price bands, Tay said.

He foresees landed home values growing by about 3–5% for the year, in tandem with the overall private housing market.

Transaction volume holds steady

URA’s flash estimates showed that sale transactions totalled 5,420 in the latest three months, up to mid-June, roughly stable from the 5,413 in the first quarter of the year.

Market activity was shaped by a relatively limited pipeline of new project launches, the announcement of changes to the executive condo (EC) policy framework, as well as seasonal factors such as the June school holidays, said Mohan Sandrasegeran, head of research and data analytics at SRI.

He added that the school holiday period traditionally sees a temporary moderation in transaction activity as some households defer major purchasing decisions.

Huttons noted that the transaction volume in 2Q2026 is around 4.5% higher than a year ago.

Yip reckoned that sentiment in the property market might have gotten a boost from the stronger-than-expected economic growth, low unemployment rate, and tentative truce between US and Iran amid the geopolitical conflict.

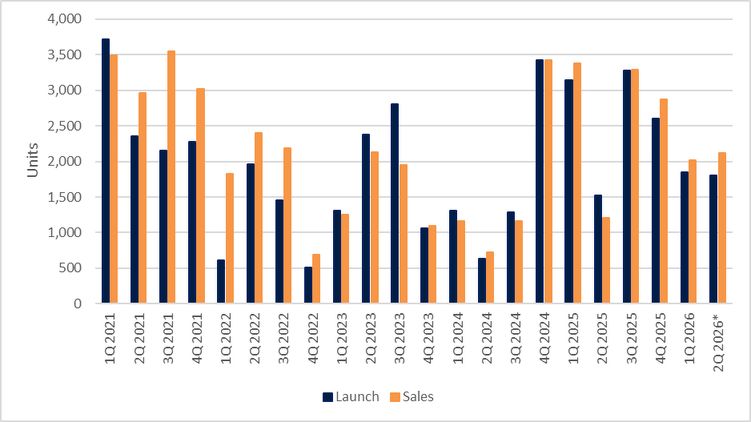

Developers' new-sale volumes:

*Estimates. Source: URA, Huttons Data Analytics as of July 1, 2026.

In terms of new sales, about 2,116 units were transacted in 2Q2026, going by Huttons' estimates. That is 5.1% higher than the previous quarter and a 74.6% surge from the same period a year ago.

As for resales, transaction volumes for non-landed private homes (excluding ECs) shrank by 18.3% q-o-q to 2,634 units in the second quarter this year, according to caveats lodged as at July 1.

ERA’s Chu noted that this is the lowest level since the second quarter of 2020, and is a departure from the stable pattern of about 3,000 resale units per quarter for the past eight quarters.

Within the subsale segment, volumes continued to decline, falling by 20% q-o-q to 140 transactions in the latest period — the lowest since the peak of 411 subsales in 4Q2023. Chu attributed this to the increase in new launches, which have longer remaining tenures and more attractive pricing.

Despite the decline in subsale volumes, the median price for the segment rose 4.6% q-o-q to $2,430 psf in 2Q2026.

Fresh wave of launches coming up

Realion's Sun reckons that challenges in the global economy such as structural unemployment, a dimmer hiring outlook, and sticky inflation may cause some prospective homebuyers to exercise more caution for big-ticket purchases.

This may impact housing demand and slow the pace of price growth. At the same time, expats and highly skilled local professionals in high-value tech sectors that are expanding will likely be well paid, which may prop up demand for private homes, Sun said.

Given these countervailing factors, Realion expects overall prices in the private residential market to grow modestly by 2.5–3.5% this year.

Other analysts anticipate that momentum may pick up again in the second half of the year as a fresh wave of project launches hits the market.

Huttons estimates that about a dozen private residential launches with about 3,567 units are slated to debut in 2H2026.

Upcoming projects in the second half of 2026:

Note: In alphabetical order, followed by chronological order. Source: URA, Huttons Data Analytics as of July 1, 2026.

Sandrasegeran of SRI said: "Buyers can look forward to a diverse pipeline of projects across the OCR, RCR and CCR segments, with many of these developments originating from government land sales (GLS) sites awarded over the past few years."

These include Lentor Gardens Residences, which is expected to offer around 499 units in the Lentor area, and Dunearn House, with an estimated 380 units in District 11.

Both upcoming condos are likely to attract buyers due to their "strategic locations, connectivity and appeal to owner-occupiers seeking well-connected residential neighbourhoods", Sandrasegeran added.

A significant anticipated launch, likely debuting in 2H2026, is Thomson Reserve — a mega redevelopment of the former Thomson View Condominium, with an estimated yield of more than 1,200 units.

Thomson Reserve is noteworthy as it will inject substantial new supply into the RCR at a time when new launch activity in the region has been relatively limited, said Sandrasegeran. The project could thus benefit from pent-up demand among buyers who have been waiting for fresh city-fringe options in the RCR, he added.

Other upcoming major condo projects in 3Q2026 include Amberwood at Holland, Lucerne Grand, and The Serra Residences. These will be followed by Bedok Rise and an EC project along Woodlands Drive 17, according to Huttons.

For the whole of 2026, around 7,300 units may be launched for sale, which will be 36.4% lower than the 11,482 units last year, Yip said.

In view of the fewer units to be launched in 2026, Huttons lowered its forecast for full-year transaction volumes to between 7,500 and 9,000 units, down from its previous projection of 8,000 to 10,000 units. It maintained its price growth forecast at 2–5%.

CBRE reckons about 7,500 to 8,500 new private homes will be sold in 2026 while overall private home prices may grow at 2–4%.

ERA projects new home sales to total 9,000 to 10,000 units this year, while the secondary market may see 13,000 to 14,000 transactions, indicating stable underlying demand.

"In 2026, the private residential market is expected to remain resilient, supported by moderate price growth driven by strong owner-occupier demand and ongoing right-sizing trends," Chu said.

For more news and analysis, read our weekly e-paper. Prefer a print copy? Get it delivered to your home every Monday.

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search