Industrial rents notch 19th straight quarterly gain in 2Q2025 as demand shifts to newer assets

Business parks continue to reflect a two-tier market, with well-located, amenity-rich assets performing well, while older stock faces leasing challenges (Photo: Samuel Isaac Chua/EdgeProp Singapore)

Ask Buddy

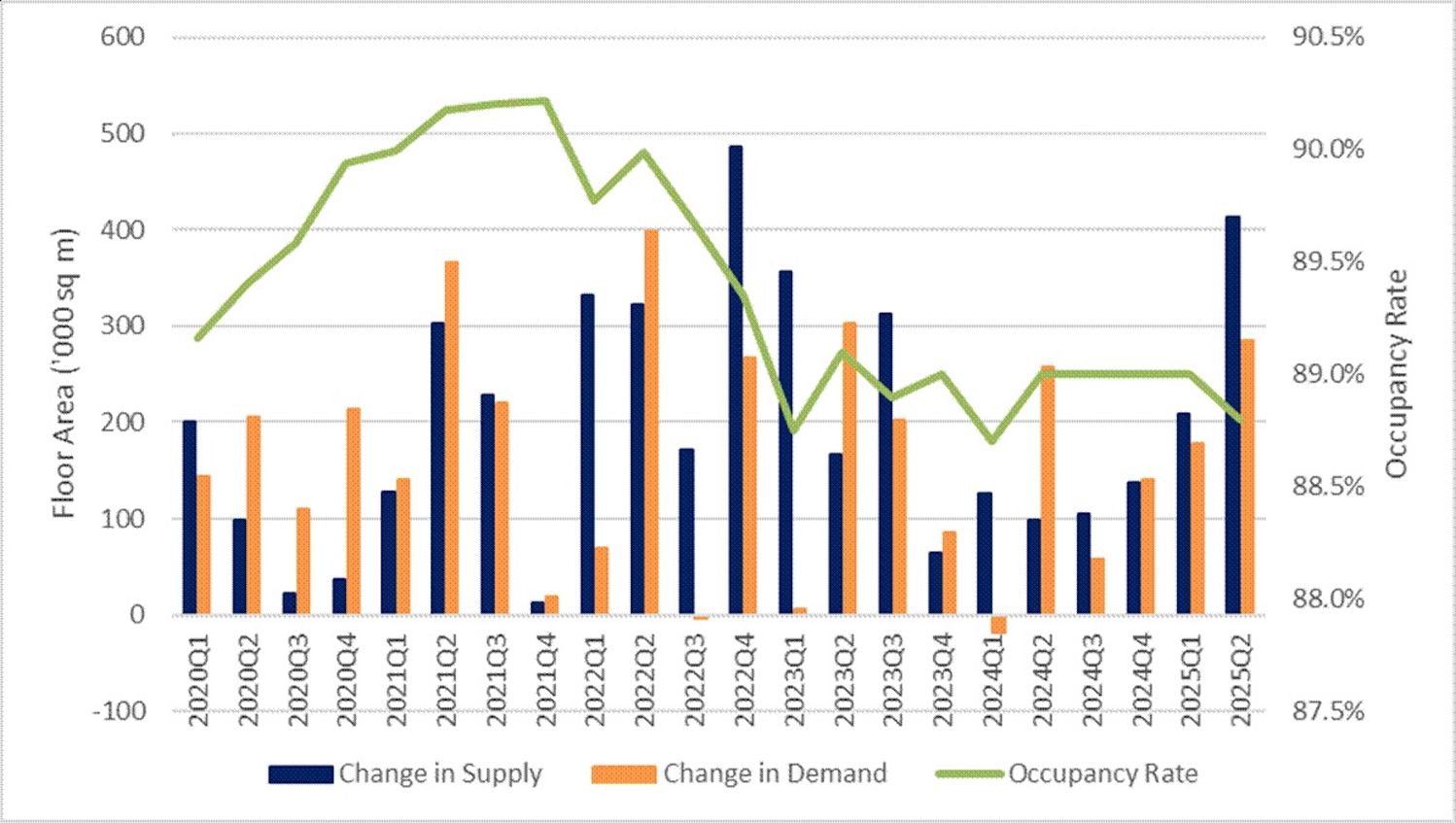

Overall industrial rents rose 0.7% q-o-q in 2Q2025, extending the 0.5% increase in 1Q2025, according to JTC statistics released on July 24. This marks the 19th consecutive quarter of growth, bringing the JTC All Industrial Rental Index 24.6% above its 3Q2020 trough.

“New developments, which have maintained steady asking rents due to higher construction costs, continued to support rental growth,” says Wong Xian Yang, head of research for Singapore and Southeast Asia at Cushman & Wakefield (C&W).

Change in Supply, Demand and Occupancy Rate of Industrial Space

Source: JTC, Huttons Data Analytics as of 24 Jul 2025

Tricia Song, CBRE’s head of research for Singapore and Southeast Asia, notes that leasing activity was buoyed by relocations and new market entrants, with demand from banking, finance, and non-traditional tenants such as educational institutions. This contributed to a decline in the overall vacancy rate from 24.1% in 1Q2025 to 23.3% in 2Q2025.

CBRE also observed increased leasing activity across logistics, hi-tech, and business park segments, supported by landlord initiatives such as fitted units and capital expenditure (capex) support, which helped accelerate tenant decision-making.

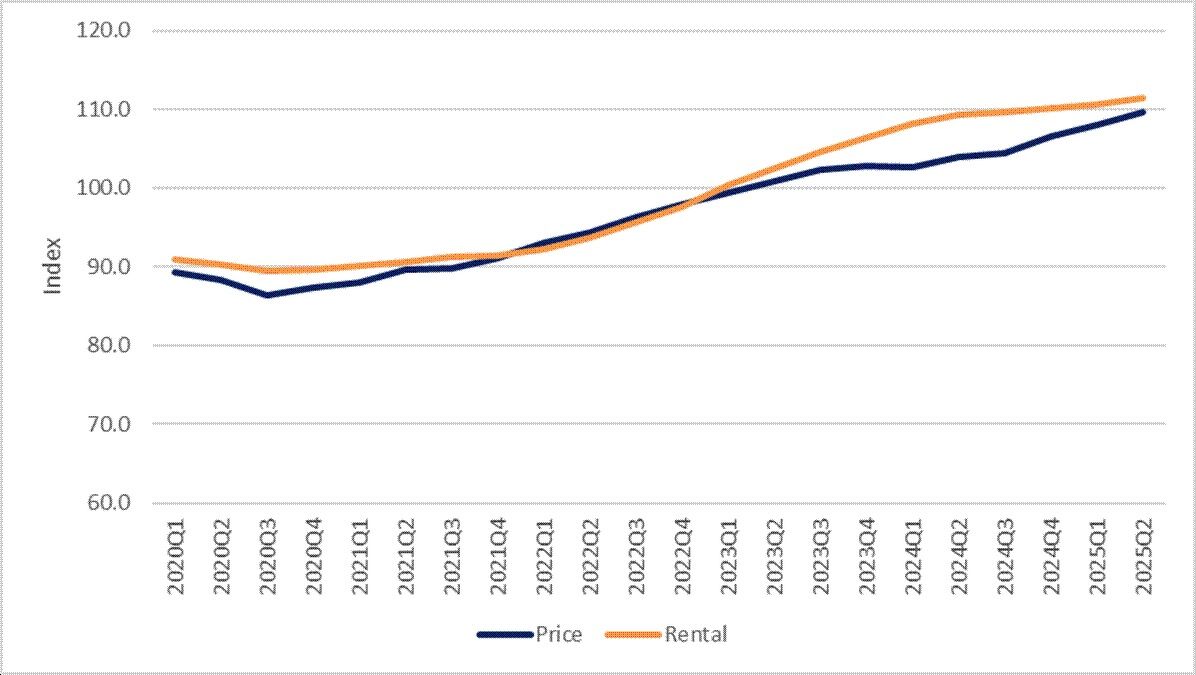

Transactions of Multi-User Factory and Warehouse Space

Source: JTC, Huttons Data Analytics as of 24 Jul 2025

Rental growth strongest for business parks

Across industrial segments, business parks recorded the strongest rental growth of 1.2% q-o-q, followed by multiple-user factories at 0.9%, and both warehouses and single-user factories at 0.4%. In 1H2025, overall industrial rents rose 1.3% ytd, moderating from 2.7% over the same period last year.

Business park rents were supported by strong take-up in new developments such as Punggol Digital District (TOP in 2Q2025) and 1 Science Park Drive (TOP in 1Q2025). The segment continues to reflect a two-tier market, with well-located, amenity-rich assets performing well, while older stock faces challenges in leasing.

Business park rents were supported by strong take-up in new developments such as Punggol Digital District (TOP in 2Q2025) [Photo: Samuel Isaac Chua/EdgeProp Singapore]

Industrial prices rose 1.4% q-o-q in 2Q2025 — the fifth consecutive quarter of growth — and 2.9% ytd in 1H2025, up from 1.0% in 1H2024.

C&W notes that overall industrial vacancy edged up 0.2 percentage points to 11.2% in 2Q2025, ending four consecutive quarters of stability. However, vacancy rates fell for business parks and single-user factories.

Rents for single-user factories rose 0.4% q-o-q, easing from 0.8% in 1Q2025, with occupancy improving by 0.4 percentage points to 89.0%. Despite new completions such as Kok Tong Transport and Engineering Works’ facility at 6 Terusan Edge and VDL Enabling Technologies Group’s factory at 259 Jalan Ahmad Ibrahim, the segment recorded a negative net supply of 0.13 million sq ft due to demolitions.

Transactions of Multi-User Factory and Warehouse Space

Source: JTC, Huttons Data Analytics as of 24 Jul 2025

Warehouse vacancy highest since 2Q2020

Warehouse vacancy climbed to 11.2% — the highest since 2Q2020 — driven by a surge in new completions that outpaced net demand. Notable completions included 15 Benoi Sector (1.1 million sq ft), Mapletree Joo Koon Logistics Hub (0.9 million sq ft), and DSV Pearl (0.7 million sq ft).

Prime logistics rents declined 0.5% q-o-q, easing from a 1.6% drop in 1Q2025. Rent softness was more pronounced in older facilities with lower ceiling heights. However, newly completed multi-user projects, such as 36 Tuas Road and Mapletree Joo Koon Logistics Hub, have recorded healthy occupancy.

Multiple-user factory rents rose 0.9% q-o-q, accelerating from 0.3% in the previous quarter. The uplift was driven by a flight to quality and proactive leasing strategies. However, occupancy declined by 0.3 percentage points to 91.0%, following the completion of JTC Space @ Ang Mo Kio (1.26 million sq ft).

Transaction volumes climbed in 2Q2025

Transaction volumes also climbed, with 435 caveats lodged in 2Q2025 — a 7.1% q-o-q increase and well above the 2019 quarterly average of 310. Investor interest remained robust, particularly in new economy assets such as data centres and life science facilities, with en bloc activity also picking up — two freehold deals were completed in 1H2025, the highest since 2017.

Transaction value surged 185.5% q-o-q to $2.2 billion in 2Q2025, up from $766.9 million the previous quarter, according to Leonard Tay, head of research at Knight Frank Singapore. Total transactions rose 4.7% q-o-q to 424 deals.

“Investor and buyer interest remained robust, supported by a wide variety of property types,” adds Tay. Key deals concluded in May included the $455.2 million sale of a data centre at 9 Tai Seng Drive, as well as business park assets The Strategy ($280 million) and 5 Science Park Drive ($245 million).

The $455.2 million sale of a data centre at 9 Tai Seng Drive (photo above), as well as business park assets The Strategy ($280 million) and 5 Science Park Drive ($245 million) [Picture: CapitaLand[

Temporary boost in front-loading activities

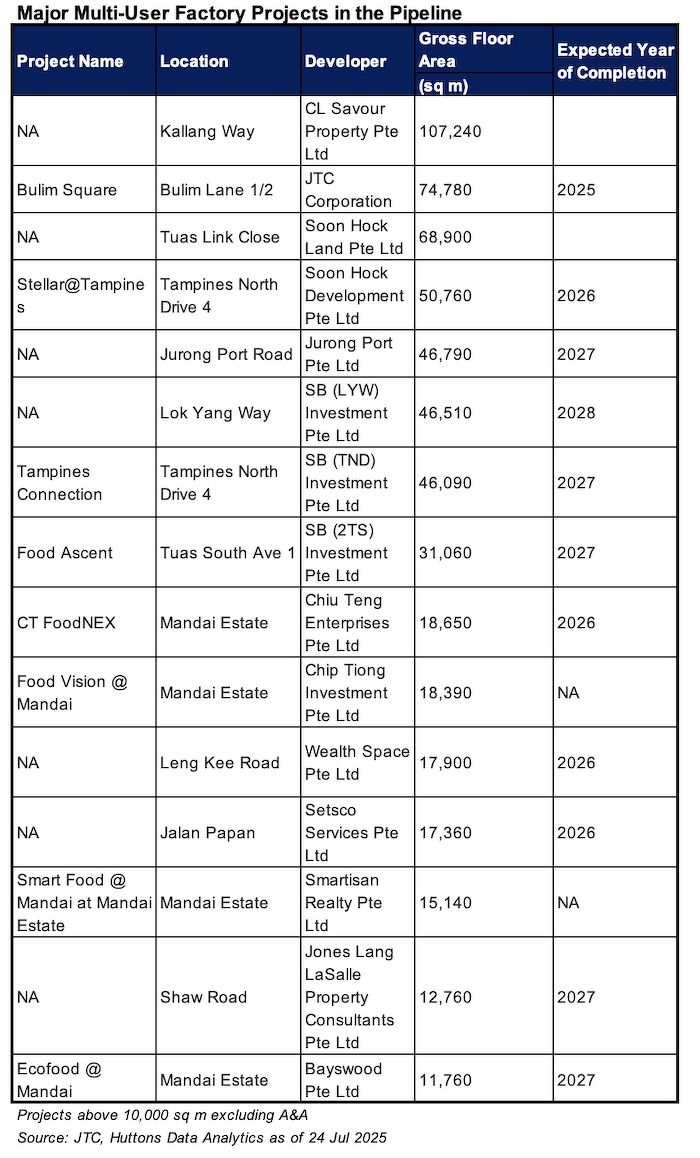

As of the end of June 2025, 2.98 million sq ft of new industrial space — equivalent to 0.5% of the total stock — is slated for completion in 2H2025. Multiple-user factories make up 48.4% of this pipeline, followed by single-user factories (27.0%) and warehouses (24.6%).

No new business park completions are expected in 2H2025. The only major upcoming project over the next three years is 27 International Business Park (0.21 million sq ft), scheduled for 2026. Supply may tighten as landlords continue to enhance their assets in older stock.

Despite global trade uncertainties, Singapore’s industrial real estate sector demonstrated resilience in 2Q2025, underpinned by growth in trade-related sectors such as wholesale, retail, and transportation and storage, says Catherine He, head of research at Colliers. “This momentum was partly driven by a temporary boost in front-loading activities during the 90-day pause in US reciprocal tariffs, prompting companies to accelerate shipments and build up inventories.”

As a result, warehouse demand — especially near logistics nodes such as ports and airports — rose noticeably, supporting rental growth in logistics and high-spec segments.

Warehouse demand — especially near logistics nodes such as ports and airports — rose noticeably, supporting rental growth in logistics and high-spec segments (Photo: Samuel Isaac Chua/EdgeProp Singapore)

‘Front-loading effect’ to taper in 2H2025

Colliers cautions that the front-loading effect is expected to taper in 2H2025 as activity normalises. “Singapore’s high degree of trade reliance — with re-exports comprising nearly two-thirds of total trade — makes it highly sensitive to external headwinds, particularly from US trade policy," says He.

She adds that potential new tariffs on key exports such as semiconductors and pharmaceuticals could weigh on those sectors. While leasing remains active, sentiment has become more measured, and rental growth is forecast to moderate in the coming quarters.

“Amid rising uncertainty, occupiers are shifting toward high-spec and bonded logistics facilities near ports and airports to mitigate customs disruptions,” notes Colliers’ He. DP World’s recent launch of a multi-user bonded warehouse at Mapletree Benoi Logistics Hub illustrates this trend. Such assets are seeing strong demand from industries such as electronics, pharmaceuticals, precision engineering, and luxury goods.

Developers and REITs may find repositioning or redevelopment opportunities in strategic nodes such as Tuas, Jurong, and Changi.

Industrial supply – higher than the historical average

Colliers forecasts that the average annual industrial supply will reach 1.3 million sqm by 2027, significantly higher than the historical averages of 0.9 million sqm for supply and 0.6 million sqm for demand. This elevated pipeline could place pressure on rents if absorption fails to keep pace.

Rental growth is expected to moderate to between 0% and 2% in 2025, down from 3.5% in 2024. However, modern, well-located, and future-ready assets are expected to remain resilient. Industrial prices are likely to match or exceed the 2024 annual growth rate of 3.5%, supported by stable yields and strong investor interest.

Huttons’ Lee Sze Teck shares a similarly cautious view. “While some trade deals have been made, tariffs have not been reset to zero. Higher import costs may dampen consumer demand and trade, which could affect Singapore’s economy.” He expects industrial space demand to hold steady, with rents and prices likely to remain flat for the rest of the year.

Ask Buddy

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search