Central Region office rents ease 0.1% as demand stays firm amid tight supply

IOI Central Boulevard Towers in the CBD, completed in 3Q2024 was 90% occupied by 3Q2025 (Photo: Samuel Isaac Chua/EdgeProp Singapore)

Office rents in Singapore’s Central Region eased slightly in 3Q2025, as landlords adjusted expectations amid strong occupier demand and a limited pipeline of new supply.

According to data released by the Urban Redevelopment Authority (URA) on Oct 24, Central Region office rents dipped 0.1% q-o-q, driven by a 0.1% fall in the Central Area, while the Fringe Area posted a 0.2% gain.

“The marginal dip may have been driven by older offices, as landlords became more flexible on rents to retain tenants amid continued flight-to-quality trends and a softer economic backdrop,” says Wong Xian Yang, head of research for Singapore and Southeast Asia at Cushman & Wakefield (C&W).

Prime offices rebound with steady take-up

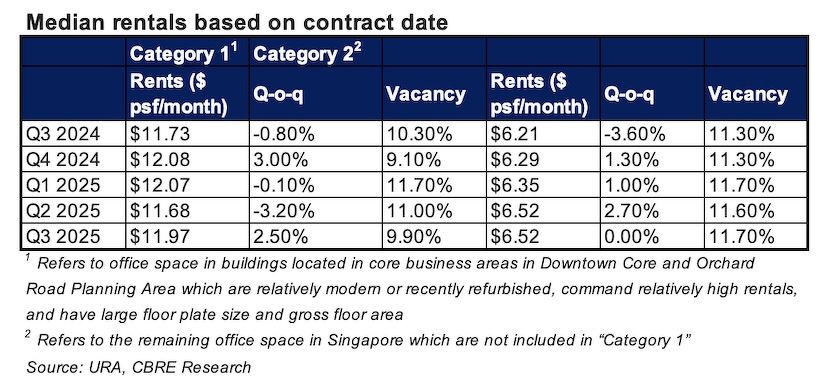

Category 1 offices — newer, higher-quality buildings in the Downtown Core and Orchard areas — saw rents rise 2.5% q-o-q after two quarters of decline, with vacancy tightening to 9.9% from 11% in 2Q2025.

“This reflects steady take-up of prime space amid easing interest rate concerns,” notes Wong.

C&W’s basket of Grade A CBD offices recorded strong net absorption of 197,000 sq ft in 3Q2025, up from 185,000 sq ft the previous quarter, underscoring sustained demand for modern, amenity-rich workplaces.

Meanwhile, Category 2 offices (outside Category 1) saw rents stabilise after three quarters of growth, with vacancy edging up marginally to 11.7% from 11.6%, as the market continued to rebalance amid ongoing flight-to-quality activity.

Source: URA

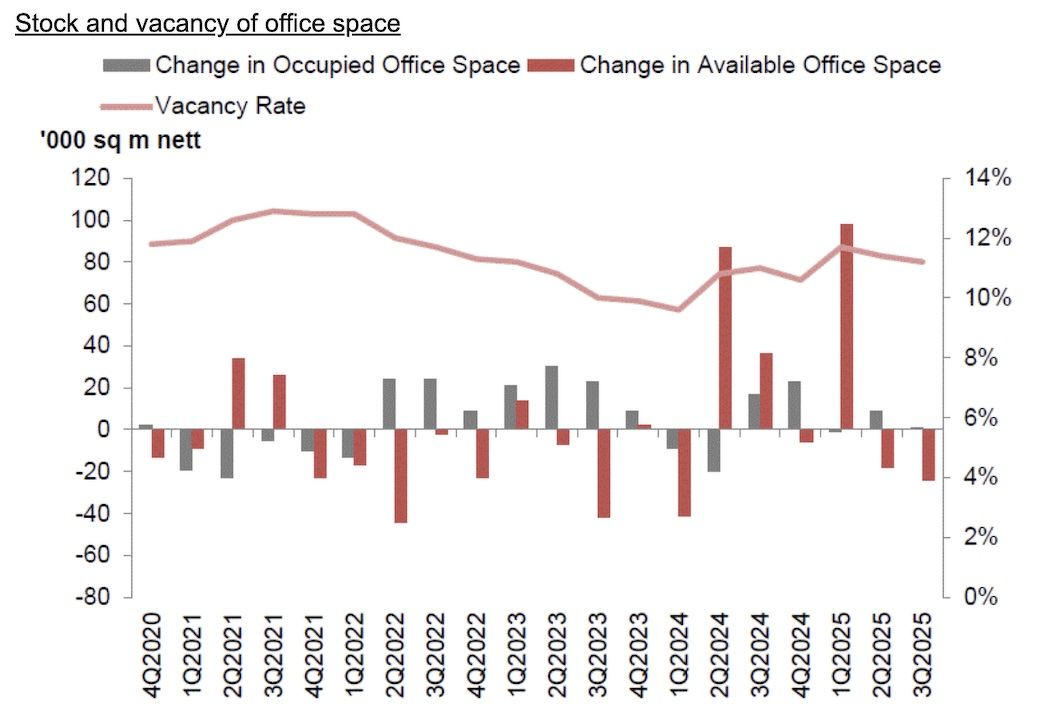

Vacancy rates fall as demolitions trim supply

Islandwide office demand remained modestly positive, with net absorption of about 11,000 sq ft in 3Q2025. This outpaced the negative net supply of 0.2 million sq ft, largely due to demolitions, driving overall vacancy down to 11.2% from 11.4% in the prior quarter.

In the Downtown Core, net demand held steady at 0.2 million sq ft, while vacancy improved to 9.8% from 10.3%.

Despite a cautious global outlook, the Core CBD Grade A segment remained resilient with rents up 0.8% q-o-q to $12.20 psf per month in the quarter. Vacancy tightened from 5.9% in 1Q2025 to 5.1% in 3Q2025, according to Tricia Song, head of research for Singapore and Southeast Asia at CBRE.

She points to IOI Central Boulevard Towers in the CBD, completed in 3Q2024 and 90% occupied by 3Q2025.

Outside the CBD, Paya Lebar Green reached full occupancy following Visa’s relocation, contributing to the 0.2% q-o-q and 2.9% y-o-y increase in the URA Fringe Area rental index.

“Occupier demand remains broad-based, led by banking and finance, transport, government, and flexible workspace operators,” Song adds.

Outside the CBD, Paya Lebar Green reached full occupancy following Visa’s relocation (Photo: DP Architects)

‘Landlords focus on tenant retention’

URA data showed no new office completions in 3Q2025. Net supply contracted by 0.26 million sq ft, while islandwide vacancy continued to tighten — from 11.7% in 1Q2025 to 11.4% in 2Q2025, and further to 11.2% in 3Q2025.

“The decline in vacancy reflects continued absorption of major 2024 completions such as IOI Central Boulevard Towers, Keppel South Central, and Paya Lebar Green,” says CBRE’s Song.

“While most quality buildings are near full occupancy, landlords remain focused on tenant retention,” adds Leonard Tay, head of research at Knight Frank Singapore.

Tay notes that a subtle flight-to-quality trend persists, as occupiers right-size or modestly expand upon lease renewals — capitalising on stable rents to upgrade into newer buildings offering better connectivity and amenities.

“Flexible coworking spaces also continue to attract creative and lifestyle tenants, while older, less connected buildings face growing obsolescence,” he adds.

Source: URA

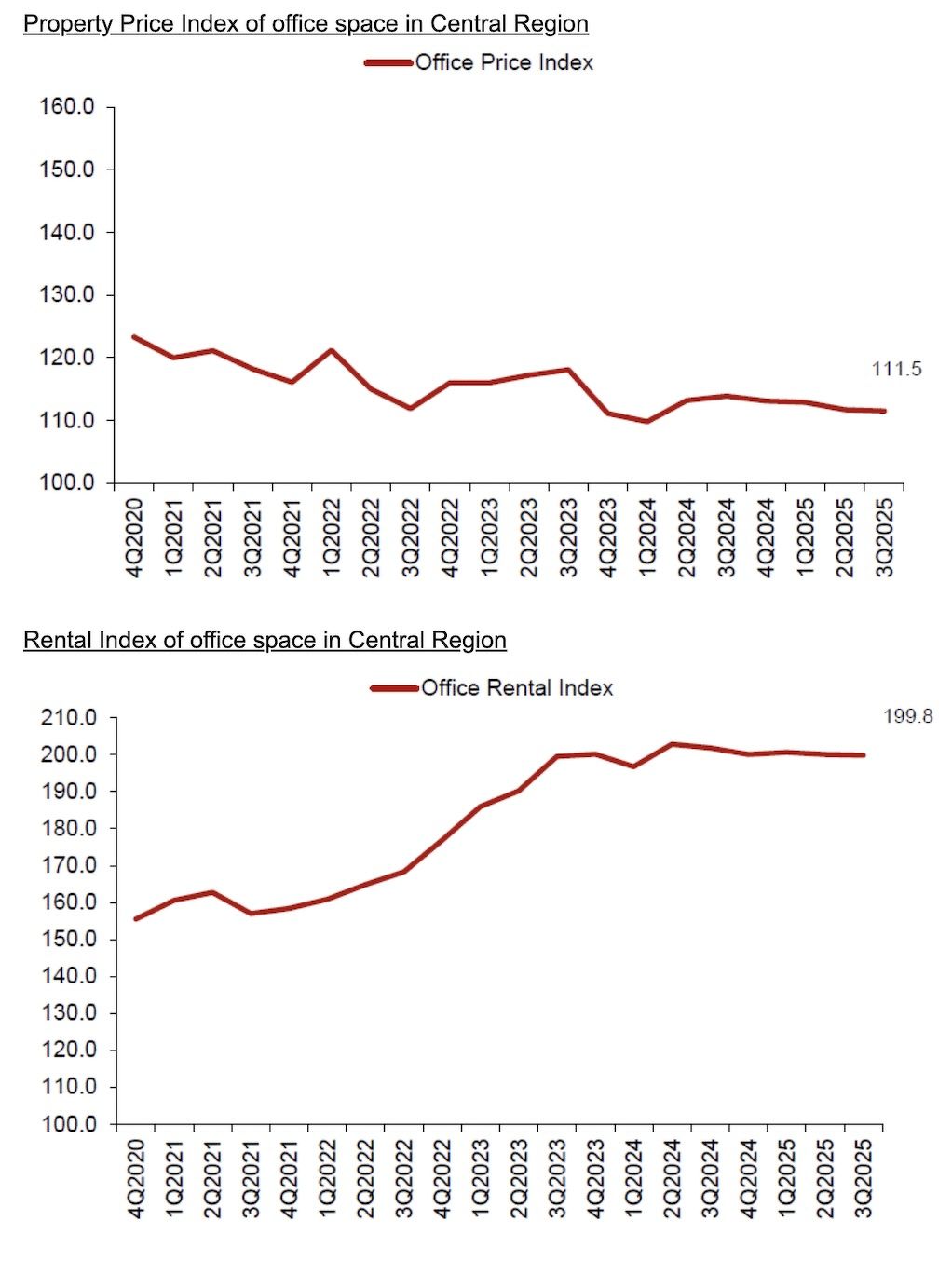

Prices show signs of bottoming

URA’s office price index for the Central Region fell 0.2% q-o-q in 3Q2025 — the fourth straight quarterly decline but a slower pace than the 1.1% drop in 2Q2025, suggesting the office capital market may be nearing a trough.

Prices have declined 1.4% year-to-date (YTD) and 2.1% y-o-y since 3Q2024.

According to C&W, the median unit price for Central Region office transactions eased to $1,995 psf, down from $2,127 psf the previous quarter, reflecting a higher proportion of lower-priced deals.

Nonetheless, the strata office segment remains resilient, says Wong, with 280 transactions lodged YTD — already 84% of 2024’s full-year total.

Source: URA

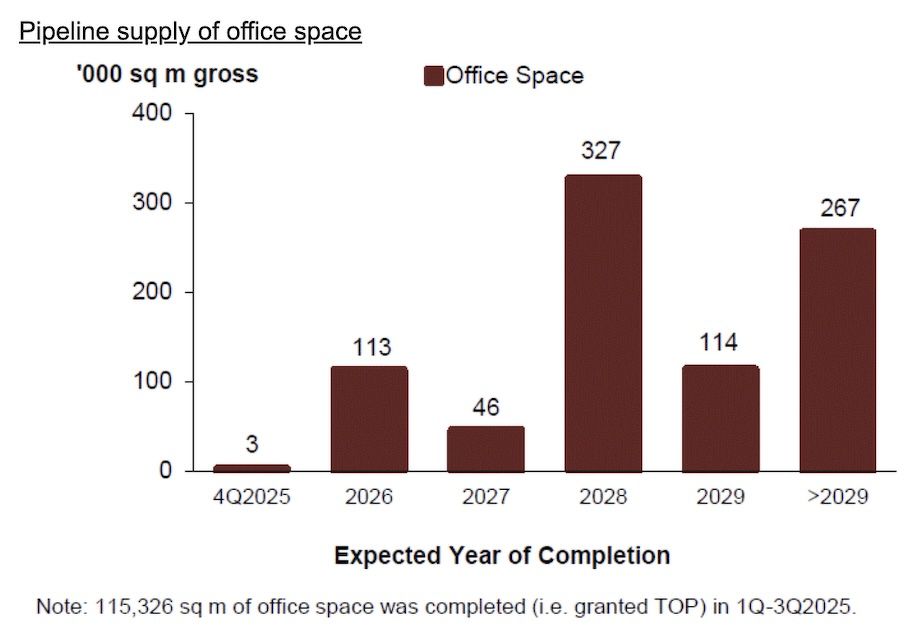

Tight pipeline through 2026-2027

The CBD Grade A pipeline remains limited, with only Shaw Tower (mid-2026) and Newport Tower (2027) expected to add about 0.6 million sq ft of net leasable area over the next two years — roughly one-third of historical annual demand.

C&W also observes that shadow space in CBD Grade A offices has fallen to 0.1 million sq ft — a nine-year low — underscoring healthy occupier interest.

While some negative net demand was recorded in the Outside Central Region (OCR) and Rest of Central Region (RCR) due to stock removals from demolitions, Wong expects relocation activity to accelerate from 2026.

“Demand for Grade A offices remains firm as occupiers prioritise modern, well-located developments,” says C&W’s Wong. “With lower global interest rates expected, expansion activity should pick up alongside renewed business confidence.”

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search