Is every town a good town?

In Tampines, which has the largest land area set aside for residential use, 84,233 out of a projected 110,000 flats have been built as at end-March 2025 (Photo: Samuel Isaac Chua/EdgeProp Singapore)

Public housing in Singapore has come a long way since the formation of HDB in 1960. As of Mar 31, 2025, more than 1.1 million flats have been completed.

Due to land constraints in Singapore, each HDB town is limited in size and has a projected maximum number of flats that can be built. For example, Bukit Timah, the Central Area and Marine Parade have the smallest land area set aside for residential use at 126ha. As of March 31 last year, 22,406 flats have been built out of a projected ultimate 25,000 flats.

Bukit Timah, the Central Area and Marine Parade (pictured) have the smallest land area set aside for residential use at 126 hectares (Photo: Samuel Isaac Chua/EdgeProp Singapore)

Tampines will have the largest land area set aside for residential use at 549ha. Here, 84,233 flats, out of a projected ultimate 110,000 flats, have been built as at end-March 2025.

HDB has rolled out numerous programmes over the years to improve the flats and rejuvenate neighbourhoods across the island. These programmes include the Home Improvement Programme (HIP), HIP II, Main Upgrading Programme, Neighbourhood Renewal Programme, Lift Upgrading Programme and Renewing Our Heartland, to name a few.

It is well documented that some towns have higher selling prices and more million-dollar flats than others. Some agents attest that flats in certain towns or locations are difficult to sell, whereas others sell within a matter of days.

What drives the popularity of certain towns, and does that have a bigger influence on the selling price of flats?

Most popular HDB towns

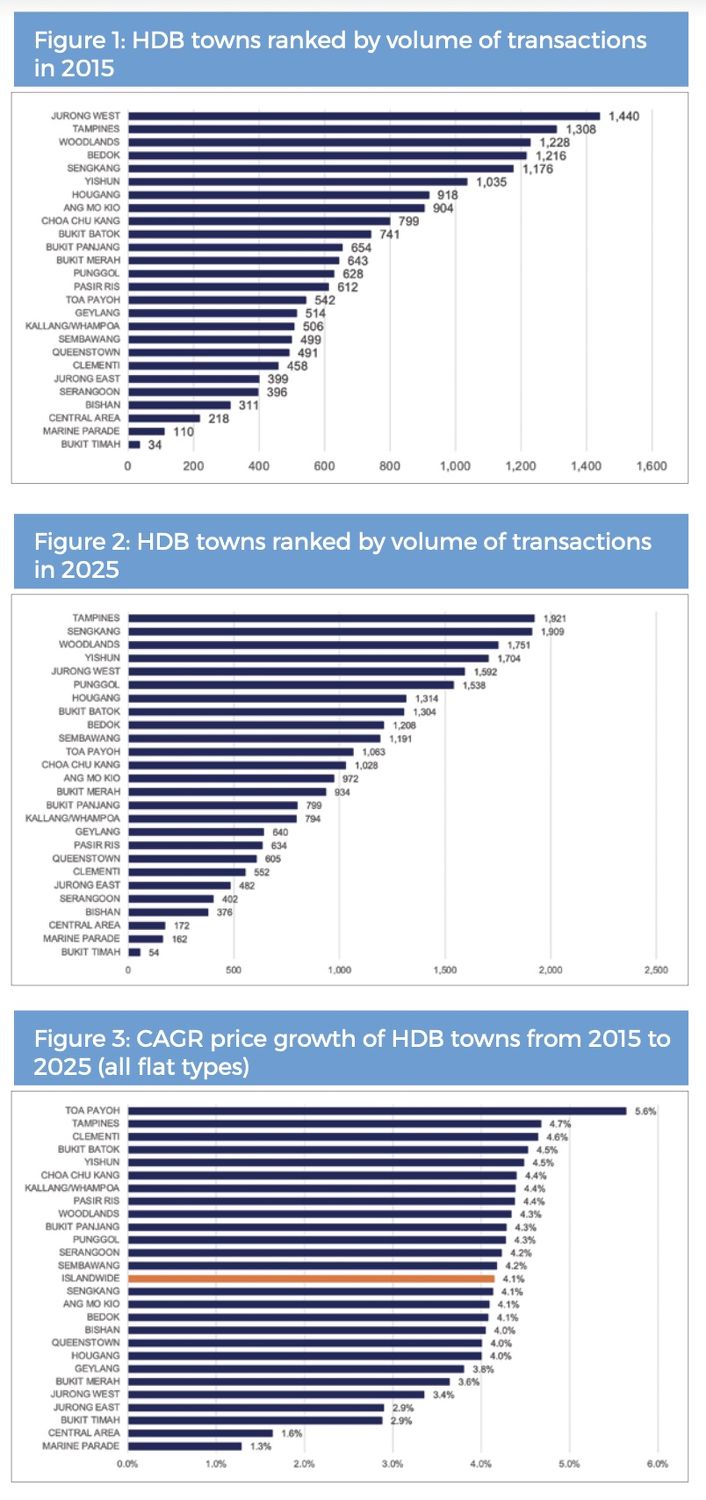

Based on caveats downloaded from data.gov.sg, the top five HDB towns by transaction volume in 2015 were Jurong West, Tampines, Woodlands, Bedok and Sengkang. At the other end of the spectrum were Bukit Timah, Marine Parade, Central Area, Bishan and Serangoon.

Data from HDB shows that Jurong West, Tampines, Woodlands, Bedok and Sengkang were among the largest HDB towns by dwelling units, whereas Bukit Timah, Marine Parade, the Central Area, Bishan and Serangoon were among the smallest HDB towns by dwelling units.

HDB data shows that Jurong West (pictured), Tampines, Woodlands, Bedok and Sengkang were among the largest HDB towns by dwelling units (Photo: Samuel Isaac Chua/EdgeProp Singapore)

Huttons Data Analytics estimates that from 2015 to 2025, the annual HDB resale volume was around 2.3% of the total number of dwelling units managed by HDB.

With more dwelling units in a town, there will be more resale flat transactions as well. Hence, a plausible explanation for the most popular town is the number of dwelling units.

The five most popular towns changed slightly in 2025. Bedok dropped to ninth place and was replaced by Yishun in the top five.

Did Bedok become less popular among buyers over the last 10 years? Not really. The number of resale flat transactions has remained relatively stable at around 1,200 units.

However, during this period, an estimated 18,000 flats in Yishun met the five-year minimum occupation period (MOP), whereas in Bedok the number increased by around 3,900. More buyers gravitated to the newer flats in Yishun. This may have propelled Yishun to rank among the top five towns.

Tampines overtook Jurong West as the top-ranked town because it had the largest number of dwelling units as at the end of March 2025. Similar to Yishun, more than 11,000 flats met the MOP during this period, which may have attracted more buyers.

In contrast, Bukit Timah, Marine Parade and the Central Area saw a negligible increase in dwelling units. Thus, their rankings remained unchanged.

Hence, a steady supply of Build-To-Order (BTO) flats will ensure a constant stock of new homes and may keep buyers interested in staying in the town. This suggests that the most popular towns by transaction volume may reflect policy design more than underlying market conditions.

CHARTS: DATA.GOV.SG, HUTTONS DATA ANALYTICS (DATA DOWNLOADED AS AT JAN 23)

HDB towns with the highest price growth

Will the steady supply of new flats cap price growth because of higher competition, or will it push prices up because of the “newness” of the flats? Conversely, does it mean that price growth will be better if there is limited or no supply?

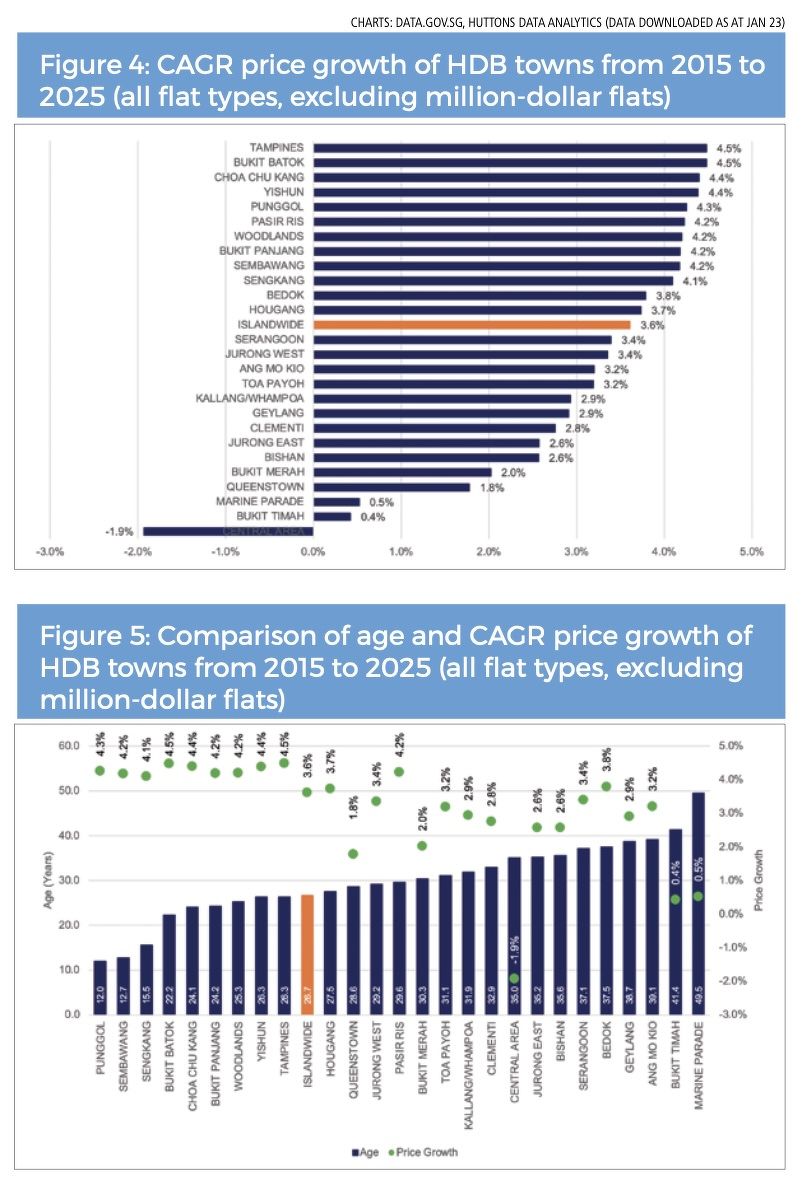

In Bukit Timah, Marine Parade and the Central Area, the supply of new flats is negligibl,e but their price growth over the last 10 years ranged from 1.3% to 2.9% per annum — well below the 4.1% annual growth islandwide. It did not appear that limited or no supply resulted in better annual price growth.

On the other hand, the three towns with the highest annual price growth were Toa Payoh, Tampines and Clementi. They had a steady supply of new flats over these 10 years. It appeared that the effect of new flats on price growth was stronger than that of supply.

In fact, the annual price growth for Toa Payoh outpaced many other towns. A deeper dive showed that there was an overwhelming number of million-dollar flat transactions in Toa Payoh in 2025 — that is, 302 or 28.4% of total transactions in the estate. That may have skewed the price growth upwards.

The annual price growth for Toa Payoh outpaced that of many other towns (Photo: Samuel Isaac Chua/EdgeProp Singapore)

If the million-dollar flat transactions in Toa Payoh were excluded, the annual price growth would decline to 3.2% from 5.6%.

As almost all HDB towns, with the exception of Choa Chu Kang, Jurong West and Sembawang, had million-dollar flat transactions, they could have skewed the annual price growth, as was the case for Toa Payoh.

When the million-dollar flat transactions were excluded from the analysis, the ranking of annual price growth across HDB towns changed drastically.

The top five towns with the highest annual price growth were Tampines, Bukit Batok, Choa Chu Kang, Yishun and Punggol. The prices of flats in Marine Parade and Bukit Timah were almost unchanged over the past 10 years, while those in the Central Area contracted by 1.9%.

Age does matter

A further analysis was conducted to determine whether the age of the flats or lease decay influenced annual price growth. The average age of flats transacted islandwide in 2025 was 26.7 years, and the corresponding annual price growth was 3.6%.

Towns with an average age below 26.7 years experienced annual price growth of 4.1%-4.5%, substantially higher than the islandwide annual price growth of 3.6%.

All these towns — Punggol, Sembawang, Sengkang, Bukit Batok, Choa Chu Kang, Bukit Panjang, Woodlands, Yishun and Tampines — are considered non-mature estates or non-Plus/Prime locations, and saw a steady supply of new flats over the last 10 years.

Sengkang, a non-mature estate or non-Plus/Prime location, saw a steady supply of new flats over the last 10 years (Photo: Samuel Isaac Chua/EdgeProp Singapore)

By contrast, towns with a higher average age experienced smaller annual price growth over the last 10 years. Flats in Bukit Timah and Marine Parade experienced near-zero price growth over the last 10 years due to their age.

Effects of lease decay

The popularity of certain towns among buyers may be a direct result of government policies on BTO supply.

The age of flats or leases matters in determining price growth over time. Younger flats tend to see better price growth than older ones.

HDB towns which outperformed the islandwide price growth were all in non-mature or non-Plus/Prime locations.

While the government has rolled out various programmes over the years to improve flats and rejuvenate neighbourhoods, these may only partially slow the effects of lease decay.

Lee Sze Teck is the senior director of data analytics at Huttons Asia

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search