Grade-A office rents to climb for fourth straight year: Colliers

SINGAPORE (EDGEPROP) - Colliers International released its quarterly office market report for 4Q2019, which stated that Singapore CBD Grade- A office rents climbed by 7% y-o-y for the whole of 2019. This followed a 15% growth rate posted in 2018, as well as a 2.3% increase in 2017. Rental growth in this office segment is expected to continue this year, and Colliers forecasts rents will increase by 1% y-o-y this year.

The anticipation of higher supply of new office space in 2022 is also expected to slow down the rental growth next year; rents are expected to decline by 4% y-o-y in 2021. However, Singapore’s office market remains an attractive occupier market, and Colliers expects average rents in the city state to increase by 3.3% per year over the next four years.

According to Tricia Song, head of research for Singapore at Colliers International, “2019 was a year of two halves: 1H2019 saw a steady 5.4% y-o-y rental growth on the back of strong net absorption led by flexible workspace and technology sectors; while 2H2019 witnessed lower net demand from a weaker economic growth, rising vacancy and slowing rental momentum as tenants showed increasing resistance to further rent rise”.

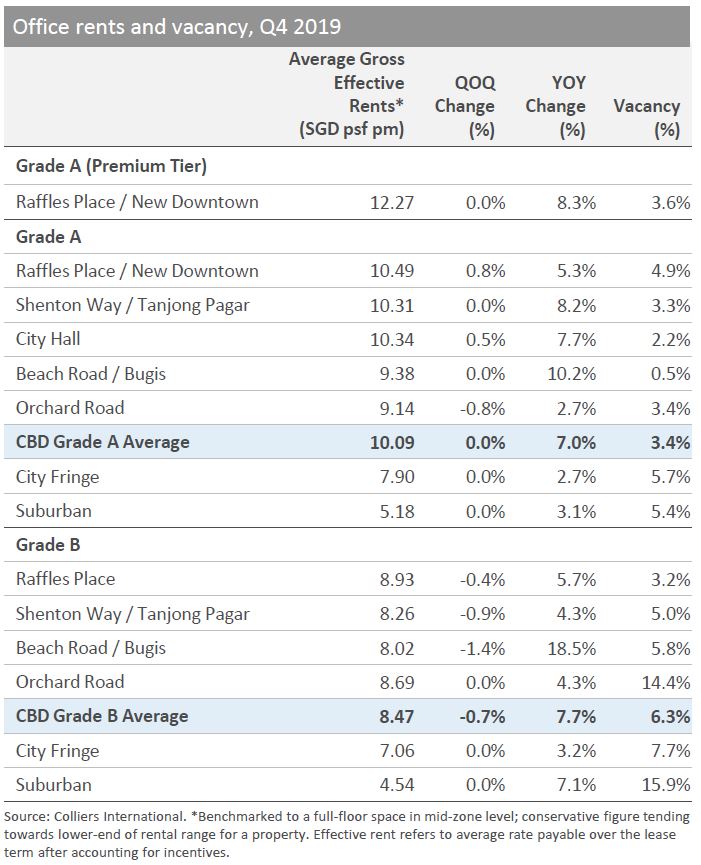

In 4Q2019, CBD Grade-A office rental growth was flat at $10.09 psf per month (pm), while rents of Grade-B office space slipped 0.7% q-o-q to $8.47 psf pm, the first quarterly decline in this segment since 3Q2017.

Colliers expects average rents in the city state to increase by 3.3% per year over the next four years. (Picture: Pixabay)

Colliers attributes this to reservation on the part of occupiers and landlords. Occupiers were more conservative about their space needs due to subdued economic growth, while landlords were being more realistic on asking rents as occupiers also faced increased cost pressures.

The Beach Road/Bugis submarket posted the best performance in 2019, climbing 10.2% y-o-y, as landlords priced in the upcoming rejuvenation of the precinct, including the planned completion of Guoco Midtown in 2022 and the redevelopment of Shaw Tower in 2023.

Meanwhile, the Raffles Place/New Downtown (premium) submarket grew 8.3% y-o-y, and the Shenton Way/Tanjong Pagar area climbed 8.2% y-o-y. These two submarkets performed well, driven by the completion of new office buildings.

According to Song, the modest pickup in economic activity in 2020 could provide some lift to business sentiment and could boost rents. Meanwhile, new CBD Grade-A supply is expected to remain limited at about 820,000 sq ft per year over 2020-2021. This will keep vacancy rates below the 10-year average of 6.2% during this time.

“We believe there are opportunities for occupiers to plan ahead and make their moves this year – be it renewals or relocation – as the office rental growth is likely to ease relative to the stronger increases seen in the past two years. Meanwhile, the next wave of office supply coming in 2022 could trigger a ‘flight to efficiency’ as some occupiers may look to relocate from their existing premises to new builds,” says Rick Thomas, head of occupier services for Singapore at Colliers International.

Read also:

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search