Homeowners chase the lowest rate. Investors build the right structure. Here’s why that gap matters

A homeowner who has set up their loan correctly, with aligned lock-in periods, an equity term loan in place, and funds positioned in an offset account, is in a fundamentally different position from one who has simply chased and locked in the lowest rate (Photo: Shutterstock)

Most people, when their home loan lock-in ends, ask the same question: which bank has the lowest rate now?

I understand why. Over a 25-year tenure, a 0.2% difference in interest rate is real money. Rates have fallen significantly from their 2023 highs. Banks are competing aggressively. Paying attention to rates is not just reasonable. It is responsible.

But here is what I have observed after years of working with both everyday homeowners and experienced property investors. The ones who consistently build more wealth, more flexibility and more financial control through property are not the ones who always find the lowest rate.

They are the ones who ask completely different questions: What does this mortgage need to do for me over the next five years, and is the structure I am choosing built for that?

There is a large gap between those two questions. In my experience, the cost of that gap far exceeds whatever the interest rate differential might have saved.

This article addresses that gap, and what the top property investors in Singapore are doing differently on the other side of it.

Homeowners play one game; investors play another

Here is the reality that most people do not see until it is too late.

When a homeowner focuses entirely on securing the lowest rate, they are optimising one variable in a multivariable equation. The rate is visible. The savings feel immediate. The monthly instalment goes down. It feels like the right decision.

But a mortgage is not a standalone transaction. It is a position on a balance sheet. And positions have to fit coherently with everything else on that balance sheet, including what you plan to do with your property in the years ahead.

Experienced investors know this intuitively. I have sat across from enough of them to notice the pattern. When a sophisticated investor reviews their mortgage, the rate is usually the last thing they discuss, not the first.

For the homeowner, the fundamental questions are structural.

What is the lock-in period, and does it align with my next move?

A two-year fixed rate that looks attractive today is the wrong tool for a homeowner planning to upgrade in 18 months. The early redemption penalty, the timing of the exit and the impact on a subsequent loan — all these come before the rate question, not after.

Does this loan structure preserve my borrowing capacity for the next purchase?

If an upgrade, second property or decoupling arrangement is on the horizon, the current loan structure has a direct bearing on total debt servicing ratio headroom and future eligibility. Investors model this in advance. Most homeowners discover it at the point of application.

Am I optimising for cash flow, total interest cost or flexibility?

These three objectives point towards different loan tenures, package types and repayment strategies. Conflating them produces decisions that feel right in the moment but drift away from the actual goal.

The worst mortgage decision is not always the one with the highest rate. It is the one with the wrong structure for the wrong moment.

The rate matters. But it is the last piece of the puzzle, not the first.

How do you make your equity work harder without deploying it?

Let me start with a move that is available to any homeowner, but that most have not been told about. It is not an investor play. It is a wealth-preservation play. But done correctly, it improves a homeowner’s financial position without requiring them to take on meaningful risk.

When CPF funds are used for a property purchase, they do not simply sit inside the property. They continue to accrue interest at 2.5% per annum, compounding annually. This is the notional interest the Central Provident Fund (CPF) would have earned had the money remained in the Ordinary Account (OA).

It builds quietly, year after year, and is added to the amount that must be returned to CPF when the property is sold. Most homeowners have no idea how large this obligation has grown until they see the sale proceeds and realise that a significant portion is going straight back to CPF.

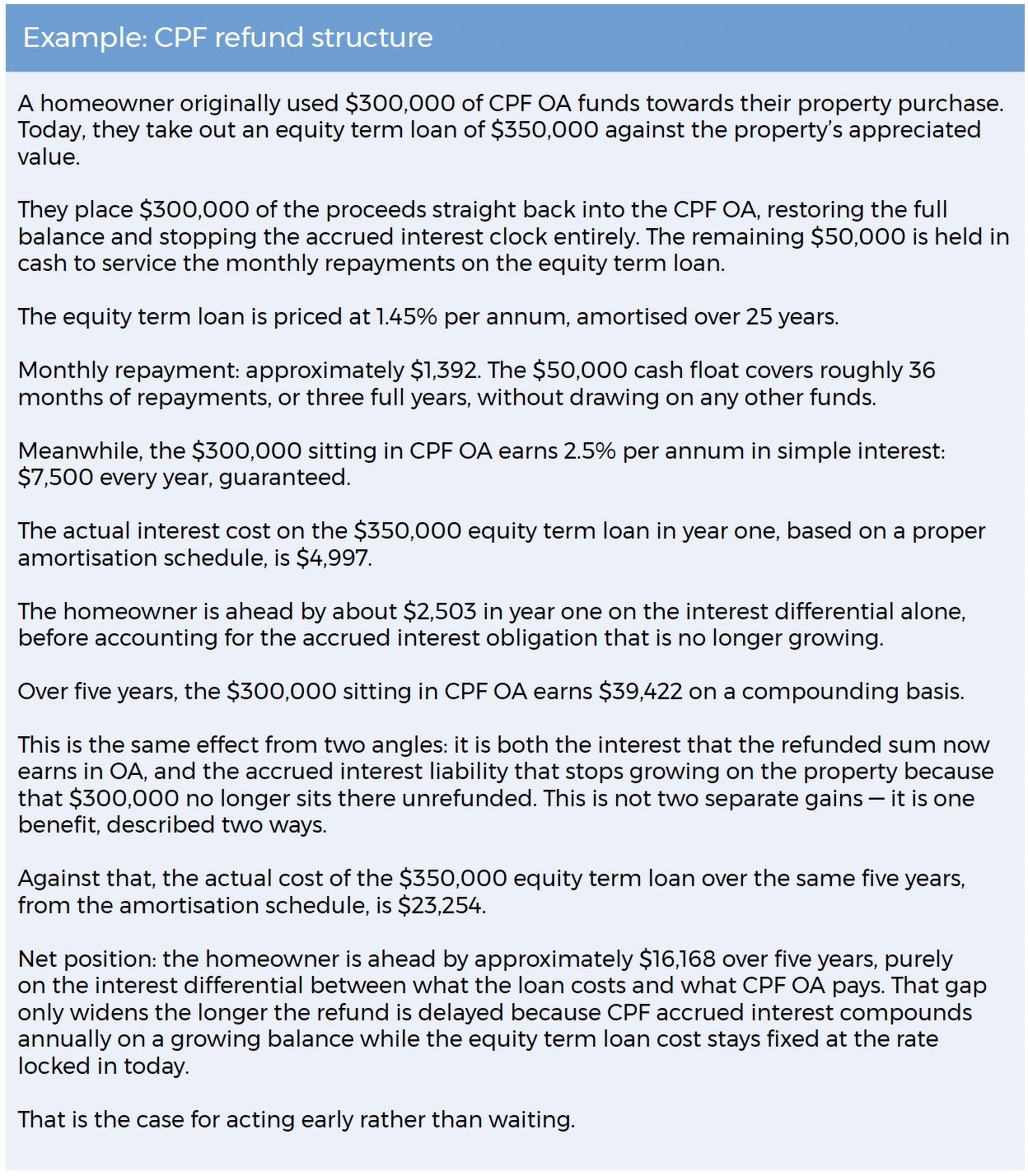

Savvy homeowners treat this as a problem to solve, not a fact to accept. The move: take out an equity term loan against the property’s appreciated value and use the proceeds to refund CPF.

The effect is immediate and structural. The accrued-interest clock stops. The CPF balance is restored, and that restored balance is available for the next purchase, including downpayment and fees on an upgrade.

And here is the part that most people miss: if the equity term loan rate is below 2.5%, the homeowner is not just stopping a bleeding. They are coming out ahead on the interest differential.

There is one important distinction to understand. Housing loan repayments can be financed using CPF funds. Equity term loan repayments must be made entirely in cash. This shapes how the structure is set up.

The question becomes: Does it make sense to take a slightly larger equity term loan quantum, keep some cash to service the repayments, and let the refunded CPF sit in the OA earning 2.5%?

Let me show you the numbers (see “Example: CPF refund structure”).

This is not an exotic strategy. It is straightforward arithmetic. But it requires someone to work through the numbers with you rather than simply showing you a rate-comparison table.

The CPF refund play is a smart move for homeowners who want to reduce a growing liability and improve their financial position without taking on meaningful risk. But for investors, the conversation around equity goes considerably further.

For the investor: Equity trapped in a property is equity not working

I want to address a mindset I encounter constantly, and it is one that costs homeowners more than almost anything else.

Most people think about accessing equity from their property only when they need it. A business opportunity surfaces. An investment becomes available. A family expense requires capital. At that point, they approach the bank, explain the situation, and begin the process.

This is the wrong sequence. And by the time most people realise it, the damage is already done.

Here are the mechanics of what actually happens when you try to extract equity reactively — at the point of need.

If you have an existing housing loan with a live lock-in period, the bank will impose a cancellation fee before it structures a new equity term loan. That is the first cost, and it is visible. The second cost is invisible but far more damaging.

The lock-in periods of your housing loan and the new equity term loan will no longer be aligned. They will expire at different times.

That misalignment follows you into every subsequent refinancing exercise. When you try to refinance in the future, you cannot move both facilities cleanly at the same time. You are always caught.

One facility is always mid-cycle. And the bank knows it. The result: you perpetually negotiate from the weaker position, and you perpetually accept worse terms than the market would otherwise offer you.

If you wait until you need the money and then act, you have already lost the advantage. Rates may have shifted, your loan structure is misaligned, and the bank holds the leverage.

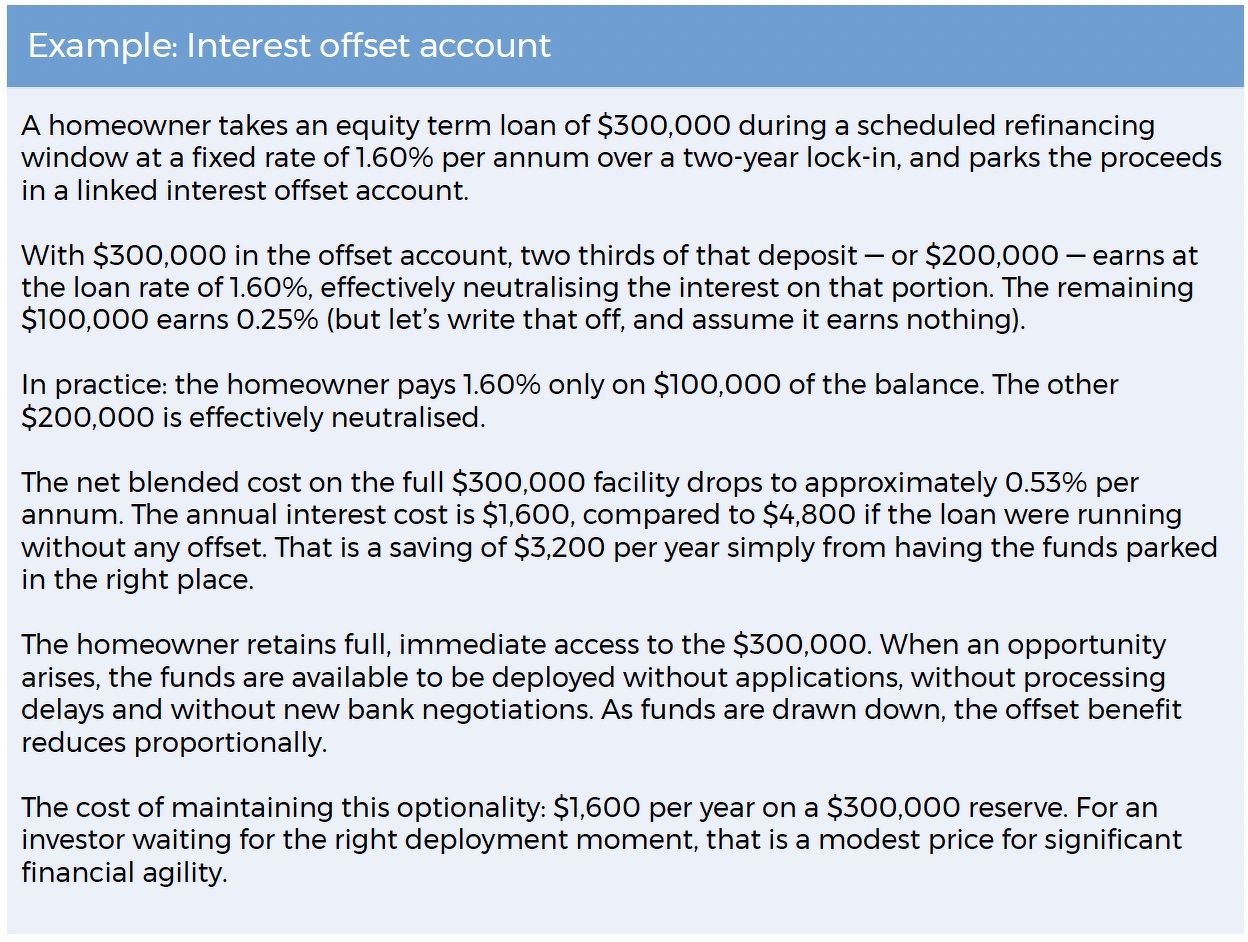

Investors understand this. They do not access equity when they need it. They access it when conditions are right, which is always during a scheduled refinancing window when both facilities can be structured together cleanly, with aligned lock-in periods and no penalty implications.

The funds are drawn and placed into an interest offset account, where they sit as a pre-positioned capital reserve until the right deployment opportunity arrives. This is the mechanism that makes proactive equity extraction not just smart, but genuinely low cost while the investor waits for the right moment to deploy.

Here is how it works.

An interest offset account is a facility, offered by several Singapore banks, where deposits held in a linked account offset the outstanding loan balance for interest calculation purposes.

The key mechanic: two thirds of every dollar deposited earns at the same rate as the housing loan, effectively neutralising the interest cost on that portion. The remaining one third earns nothing. The account is approximately 67% efficient as an offset tool.

This means the cost of parking equity in the offset account is not the full loan rate. It is approximately one third of it (see “Example: Interest offset account”).

The homeowner who says they do not need to access equity today because they have no immediate use for it is making a logical-sounding argument — but one that misses the point entirely.

The best time to set this up is precisely when there is no urgency. That is when the lock-in periods align cleanly, the penalties are zero, and the offset account keeps the cost of waiting to a fraction of the loan rate.

When urgency arrives, every one of those conditions has deteriorated.

Rates will shift; your structure decides if you’re ready

Rates will move. They always do. The question is not whether they will shift, but whether your loan structure leaves you in a position to respond well when they do.

This is where the structural approach to mortgages pays off in a way that rate optimisation never can. A homeowner who has set up their loan correctly, with aligned lock-in periods, an equity term loan in place, and funds positioned in an offset account, is in a fundamentally different position from one who has simply chased the lowest rate and locked in.

When rates fall, the homeowner with a well-structured loan has options. They can refinance cleanly when the lock-in expires, with both facilities moving together, and capture the new environment from a position of strength. They are not scrambling to exit a misaligned structure or absorbing penalties to get there.

When rates rise, the same homeowner is protected by the structure they put in place earlier. Their equity is accessible. Their lock-ins are aligned. Their cash is liquid.

Conversely, the homeowner who optimised only for today’s lowest rate finds themselves with fewer options and more friction. They did not make a wrong bet. But they never built the structure that would have let them respond well regardless of how things unfolded.

That is the difference between managing a rate and managing a position.

Thinking about your mortgage as it stands, means you are already behind

This is the mindset shift that separates the top investors from everyone else. It has nothing to do with net worth or access to information.

Most homeowners come to a mortgage review thinking about the present. What are rates doing right now? What is the cheapest package today? What does this do to my instalment this month?

These questions produce locally reasonable decisions and globally fragile ones.They feel right in the moment. They frequently create constraints that are only discovered later, at the worst possible time.

The investors who manage their property finances well are already five years ahead in their thinking when they sit down to review. They are asking:

- Where will I be in five years?

- Have I upgraded? Am I still holding this property?

- Do I intend to acquire another?

- What does my borrowing capacity look like then?

- Does the structure I put in place today give me more or fewer options when I get there?

That frame changes everything.

A lock-in period is no longer just a rate decision. It is a timing decision that has to fit a future transaction.

An equity term loan is no longer an unnecessary liability. It is a pre-positioned capital reserve that is waiting for the right deployment moment.

A mortgage review is no longer an administrative exercise. It is a portfolio checkpoint.

The right time to make a mortgage decision is before the situation forces one on you. Reactive decisions in property financing are almost always more expensive than proactive ones.

Compounded across a full property journey, the homeowner who consistently plans five years ahead builds meaningfully more financial flexibility than the one who optimises each review in isolation. This is not because they are smarter or richer, but because they are further ahead in their thinking.

Different kind of mortgage conversation

Singapore homeowners are more financially aware than they have ever been. People monitor the Singapore Overnight Rate Average (Sora). They compare packages. They understand the difference between fixed and floating. This is a genuinely positive development.

But financial awareness is not the same as financial strategy.

The next evolution in how Singapore homeowners manage their mortgages is not about finding cheaper rates. It is about moving from rate optimisation to position management. (Photo: Shutterstock)

Knowing where Sora is today does not tell you whether your CPF accrued interest has been quietly compounding into a liability you have not accounted for.

It does not tell you whether your equity term loan and housing loan lock-in periods are aligned for clean future refinancing. It does not tell you whether your access to liquidity from your property is available when you need it, or whether the conditions to set it up cleanly have already passed.

These are the questions that experienced property investors ask. They are also the questions that most homeowners have not been prompted to consider.

The next evolution in how Singapore homeowners manage their mortgages is not about finding cheaper rates. It is about moving from rate optimisation to position management. From asking what the cheapest option is today to asking what the right structure is for the next five years.

The homeowners who build lasting wealth through property are not the ones who always find the lowest rate. They are the ones who always ask the right question at the right time.

That is a different game. And it is available to any homeowner who is willing to look beyond what the cheapest rates are.

Clive Chng is associate director of Redbrick Mortgage Advisory

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search