Industrial rents log longest growth streak since 1996 as prices see fastest rise in a decade

CapitaLand’s 27 IBP at International Business Park is the only new business park building slated for completion in 2026 (Photo: CapitaLand)

Ask Buddy

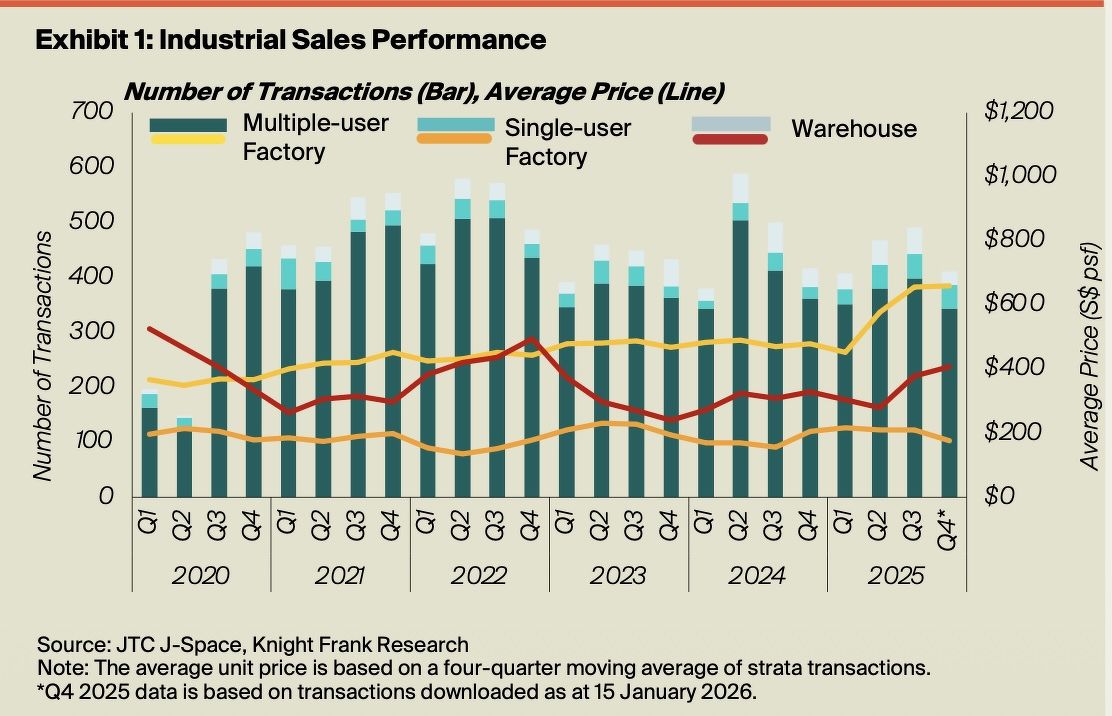

According to JTC’s property statistics, the All Industrial Rental Index rose 0.5% q-o-q and 2.4% y-o-y in 4Q2025. The latest quarterly increase marks 21 consecutive quarters of rental growth — the longest streak since 2Q1996, says Catherine He, head of research at Colliers. This implies a 25.9% increase in rents since the market’s last trough in 3Q2020.

Meanwhile, JTC’s All Industrial Price Index increased at a faster pace of 1.4% q-o-q in 4Q2025 and was 5% higher y-o-y. The quarterly growth is the strongest since 4Q2015, notes He, and represents a 30% increase from its 3Q2020 trough. She attributes the price momentum to active transactions involving industrial portfolios between institutional funds and REITs.

“Singapore’s industrial property market remained resilient through 2025, supported by ongoing global supply-chain realignment and periods of front-loaded trade flows amid tariff uncertainty,” says Chua Yang Liang, head of research and consultancy for Southeast Asia at JLL.

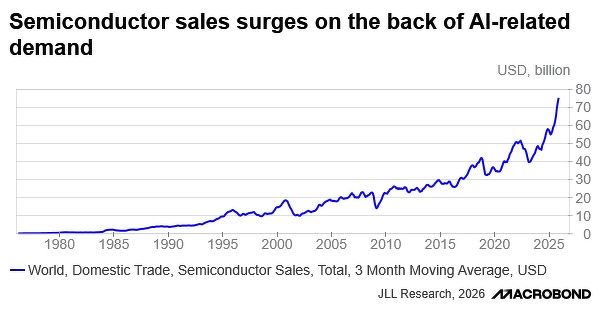

Macro indicators also point to steady underlying demand. Singapore's manufacturing purchasing managers’ index (PMI) edged up to 50.3 in December 2025 from 50.2 in November, marking the fifth consecutive month above the 50-point expansion threshold. The electronics PMI also remained expansionary at 50.9.

“The resilience is consistent with continued strength in the electronics and semiconductor ecosystem, supported by global AI-related investments, as seen in the surge in global semiconductor sales,” adds Chua.

While rental growth was positive across all industrial segments, overall occupancy eased marginally to 88.7% in 4Q2025 from 89.1% in 3Q2025. Vacancy rates tightened only at business parks and warehouses, He notes.

Warehouses: Modern logistics assets underpin demand

Warehouse rents rose 1.1% q-o-q in 4Q2025, bringing full-year rental growth to 3%. This represents a slight moderation from the 3.5% growth recorded in 2024. Occupancy improved by 0.2 percentage points to 89.8%, likely driven by positive take-up at newly completed projects.

Modern ramp-up warehouses continued to drive the bulk of demand, according to Colliers, as existing stock was often unable to meet tenants’ requirements for higher ceiling heights and larger floor plates. Demand came mainly from third-party logistics providers and electronics firms.

During the quarter, two major warehouse projects were completed, says Tricia Song, head of research for Singapore and Southeast Asia at CBRE. These are Sankyu’s Tuas Distribution Hub — a fully air-conditioned prime logistics facility spanning more than 400,000 sq ft — and Nippon Express’ expanded 100,000 sq ft warehouse at 29 Tuas Avenue 13.

Song notes that Nippon Express’ expanded facility is well-positioned to benefit from its proximity to Tuas Port and the development of the Johor-Singapore Special Economic Zone (JS-SEZ).

Across all industrial segments, warehouse occupancy rose the most in the quarter, increasing by 0.2 percentage points to 89.8%, adds CBRE.

With no new warehouse completions expected until next year, vacancy rates for prime logistics assets are set to tighten further. As a result, rents may accelerate in 2026, although increases are likely to be capped as occupiers become more cost-conscious and prioritise operational efficiency.

Factories: Diverging trends in multi- and single-user spaces

Performance within the factory segment continued to diverge between multiple-user and single-user facilities in 4Q2025.

Rents for multiple-user factories rose a modest 0.2% q-o-q, bringing full-year rental growth to 1.8%. According to Colliers, demand was driven mainly by newer and better-located developments, with some landlords offering fitted-out units and shorter lease terms to support take-up. Encouraging demand was also observed from biomedical and engineering firms.

Major completions during the quarter included Bulim Square (with remaining temporary occupation permit or TOP) and Stellar@Tampines (partial TOP), along with two food-factory developments — Food Ascent and Food Vision @ Mandai. Following these completions, occupancy for multiple-user factories declined by 1.1 percentage points to 89.9% in 4Q2025.

Food Vision (pictured) and Food Ascent are two multi-user food factories in Mandai that were newly completed in 4Q2025 (Photo: EL Development)

In contrast, rents for single-user factories rose 0.7% q-o-q, matching the pace of growth in the previous quarter, according to CBRE. For the full year, rents increased 2.7%, easing slightly from 3.2% growth in 2024.

Notable single-user factory completions in 4Q2025 included PaxOcean Engineering’s facility at 5 Jalan Samulun (partial TOP), Advanced Substrate Technologies’ facility at 9 Pesawat Drive (partial TOP), and Wuxi Biologics’ biopharmaceutical facility at 2 Tuas View Drive. Occupancy for the segment edged down by 0.3 percentage points to 88.8%, CBRE adds.

Looking ahead, growth in factory rents and prices is expected to moderate as global trade uncertainties continue to weigh on manufacturing activity and export demand.

“Vacancy rates continued to diverge between the multiple-user and single-user factory segments,” says Brenda Ong, executive director of logistics and industrial at Cushman & Wakefield. “Multiple-user factories recorded higher vacancy rates of 10.1% compared to a year ago, while vacancy rates for single-user factories appear to have peaked in 2024 and declined to 11.2% in 2025.”

Business parks: Recovery led by newer assets

Business park rents rebounded in 4Q2025, rising 0.4% q-o-q after a 0.2% decline in the previous quarter. For the full year, rents increased 2.6%, a marked improvement from the 0.2% contraction recorded in 2024. The recovery was largely driven by higher rents achieved at newly completed projects.

Occupancy improved marginally by 10 basis points to 77.1% in 4Q2025.

With only CapitaLand’s 27 IBP at International Business Park slated for completion in 2026, and several older assets being withdrawn for upgrading under asset enhancement initiatives, vacancy rates are expected to decline gradually as space is absorbed, notes Colliers.

“After several years of underperformance, business park space could emerge as a viable alternative for occupiers in 2026,” says He. This is expected to be supported by an anticipated pick-up in office rents and growing interest from cost-conscious occupiers seeking decentralised workspace options.

CBRE’s Song adds that newer business park developments in city-fringe locations remain highly sought-after, helping to lift average rents. In contrast, older assets in rest-of-island locations continue to face challenges due to ageing specifications and flight-to-quality trends, resulting in a two-tiered rental performance across the segment.

Supply pipeline expands, but unevenly across segments

About 10.66 million sq ft of new industrial space — equivalent to around 1.8% of total stock — is scheduled for completion in 2026. Single-user factories account for 53% of the pipeline, followed by warehouses (29%), multiple-user factories (15.5%) and business parks (2.5%).

Over the next three years, the only business park project in the pipeline is 27 IBP at International Business Park, which will add about 0.21 million sq ft on completion later this year. As more landlords undertake asset enhancement initiatives to upgrade ageing facilities, overall supply of business park space is expected to tighten, says Song.

Total industrial supply is projected to increase by about 3.4 million sq m (36.6 million sq ft) between 2026 and end-2028, averaging 1.1 million sq m (11.84 million sq ft) annually. This is higher than the historical three-year average annual supply and demand of 0.8 million sq m (8.6 million sq ft) and 0.6 million sq m (6.5 million sq ft) respectively, according to Colliers.

New supply in the prime logistics segment is expected to fall sharply to about 0.8 million sq ft in 2026, from 5.6 million sq ft in 2025. With most of the upcoming supply already pre-leased, options for occupiers could be limited, says CBRE’s Song. As at 4Q2025, prime logistics occupancy stood at 94.8%, and is projected to rise to 96%–97% by end-2026, pointing to stronger rental growth ahead.

JS-SEZ and cross-border dynamics

Some industrial demand could increasingly shift across the border with the JS-SEZ, which allows companies to adopt a “twinning model” by setting up complementary operations in both locations, says Song.

Data from the Ministry of Trade and Industry shows that Singapore-based companies have already committed more than $5.5 billion in investments in Johor following the JS-SEZ agreement.

Stellar@Tampines was one of the major project completions in 4Q2025 (Photo: Soon Hock Property Development)

For instance, Olam Food Ingredients has established a Customer Solutions Centre in Singapore to develop market insights, supported by an advanced production facility in Johor, to customise solutions for beverages, bakery products and frozen dairy desserts. Song expects the JS-SEZ to gain further momentum in 2026 as Singapore and Malaysia jointly compete for global investments.

‘Cautious optimism’

Advance GDP estimates show that Singapore’s economy ended 2025 on solid footing, although growth has begun to moderate as earlier external tailwinds fade. GDP growth is expected to ease from 4.8% in 2025 to about 3.8% in 2026.

Less favourable global conditions, coupled with the lagged impact of tariff-related pressures and a potential cooling of the AI-driven technology cycle — after its surge in 2025 — are likely to dampen business expansion and investment intentions in the year ahead, cautions Colliers.

“Against this backdrop, many firms are expected to adopt a more cautious approach in 2026,” says He. “Heightened global trade uncertainty and tariff-related risks could prompt occupiers to delay long-term commitments, favour shorter and more flexible leases, consolidate existing footprints, and seek fitted-out premises or landlord capital expenditure support to manage upfront costs.”

JLL, however, remains cautiously optimistic for 1H2026. While downside risks persist — particularly if tariff measures begin to bite as front-loaded inventories normalise — continued AI-led investment and resilient electronics demand should continue to support higher-specification industrial and logistics assets.

Chua projects the All Industrial Rental Index to record a moderate upside of 1–2% in 2026, reflecting higher expected completions and slower global growth. The All Industrial Price Index is expected to rise 3–4%, supported by ample liquidity and further yield compression in a lower capital cost environment.

Investment activity: Fewer deals, bigger tickets

Industrial leasing activity totalled 3,068 transactions in 4Q2025, a 3.2% q-o-q decline from 3,168 in the previous quarter, according to Knight Frank Singapore's head of research Leonard Tay.

Investor interest in industrial assets remained active in 4Q2025, despite a decline in transaction volume. Overall sales volume fell 16.1% q-o-q to 412 transactions, but total sales value surged 78.1% q-o-q to $2.3 billion, reflecting the outsized impact of several large-ticket deals.

Notable transactions included the $351 million sale of a freehold warehouse at 680 Upper Thomson Road, as well as the divestment of eight industrial properties by ESR Real Estate Investment Trust for $338.1 million.

“Prime, freehold industrial assets will continue to attract strong interest, particularly from buyers focused on business continuity and long-term capital preservation,” says Tridiana Ong, head of occupier strategy and solutions at Knight Frank Singapore. “At the same time, a growing segment of investors has become increasingly receptive to shorter-tenure factories and warehouses, attracted by higher yields supported by stable rental income and more affordable entry prices.”

Ask Buddy

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search