Prime retail rents still showing growth, but looming pressures could cloud outlook: analysts

Prime retails rents in Singapore continued its upward trajectory in 1Q2026, according to research reports by Knight Frank Singapore and Cushman & Wakefield (Picture: Albert Chua/The Edge Singapore)

Prime retail rents in Singapore continued to grow in the first quarter of this year, despite a persistently challenging cost environment and the ongoing Middle East conflict, according to market observers.

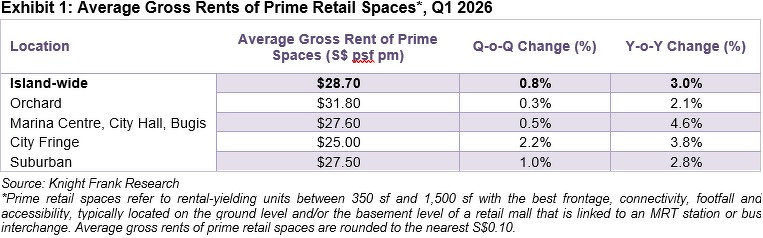

In a research report published on April 20, Knight Frank Singapore noted that average gross rents for prime retail spaces island-wide stood at $28.70 psf per month (psf pm) in 1Q2026, based on its basket of properties. This represents a growth of 0.8% q-o-q and 3% y-o-y.

Prime retail spaces in city-fringe areas were the biggest contributors to rental growth, with average gross rent in this segment climbing 2.2% q-o-q to $25 psf pm in 1Q2026. Suburban prime retail rents grew 1% q-o-q to $27.50 psf pm, followed by the Marina Centre, City Hall and Bugis cluster, which rose 0.5% q-o-q to $27.60 psf pm. Meanwhile, average gross rent for prime spaces in Orchard inched up 0.3% q-o-q to $31.80 psf pm.

In a separate report published on April 17, Cushman & Wakefield stated that gross effective rent for prime retail spaces it monitors across Singapore grew 0.4% q-o-q to $30.32 psf pm in 1Q2026. Rents in the Orchard submarket rose 0.4% q-o-q to $36.52 psf pm, followed by the suburban submarket (up 0.3% q-o-q to $33.29 psf pm) and other city areas (up 0.6% q-o-q to $21.14 psf pm).

Prime rents grew despite “a wave of closures” across the retail and F&B sectors in 1Q2026, Knight Frank highlights in its report. Notable brands that closed their doors last quarter include Australian tea brand T2 Tea, local beverage chain Fruce, and Hong Kong restaurant chain Itacho Sushi.

However, the closures were offset by expansion by existing retailers, as well as new entrants setting up in Singapore. For example, Italian restaurant Scarpetta debuted a new burger bar, Smash Street, on Amoy Street, while Chinese beverage chain Molly Tea made its debut at Orchard Central.

Cushman & Wakefield adds that demand from luxury retailers remains resilient, with new openings by high-end labels such as Zimmerman, Jil Sander, Mikimoto and Tudor in the Orchard area.

Source: Cushman & Wakefield

For Knight Frank, the ongoing churn within the retail landscape reflects both cost pressures faced by operators and fluid consumer preferences. “[This suggests] that growth is increasingly hinged on operators’ ability to innovate and refresh concepts to remain relevant and compelling to customers, while practising disciplined cost management,” it states in its report.

The firm expects cost pressures to continue impacting the retail sector in the near term. In addition, it cautions that a prolonged Middle East conflict could further drive up utility and material costs, while also dampening consumer sentiment and retail expansions. Cushman & Wakefield concurs, noting that Singapore’s retail sales “could come under pressure in 2026”, should the Middle East conflict persist or escalate.

That said, the conflict’s impact on Singapore’s tourist arrivals, a key contributor to retail activity, remains to be seen. While inbound tourism from Europe could be impacted in the near term as travellers avoid major routes that transit through the Gulf hub, Singapore could potentially benefit from diverted tourist demand from China and Japan, says Knight Frank.

Cushman & Wakefield also points out that Singapore’s safe haven status could draw further wealth management inflows, lending support to retail demand.

Amid this fluctuating landscape, it will be “increasingly crucial” for landlords and retailers to work together, says Galven Tan, CEO of Knight Frank Singapore.

“While geopolitical shocks may add more cost pressures and temper consumer confidence, these can also reshape demand flows that favour the most adaptive retail destinations and concepts,” he adds.

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search