Private home prices up 0.9% in 1Q2026, as non-landed segment rebounds

Price growth in 1Q2026 was supported by a rebound in non-landed property prices, led by OOCR, which saw a 2.2% gain on the back of benchmark prices —an average of $2,546 psf — achieved at the launch of Pinery Residences (Photo: Hoi Hup)

Ask Buddy

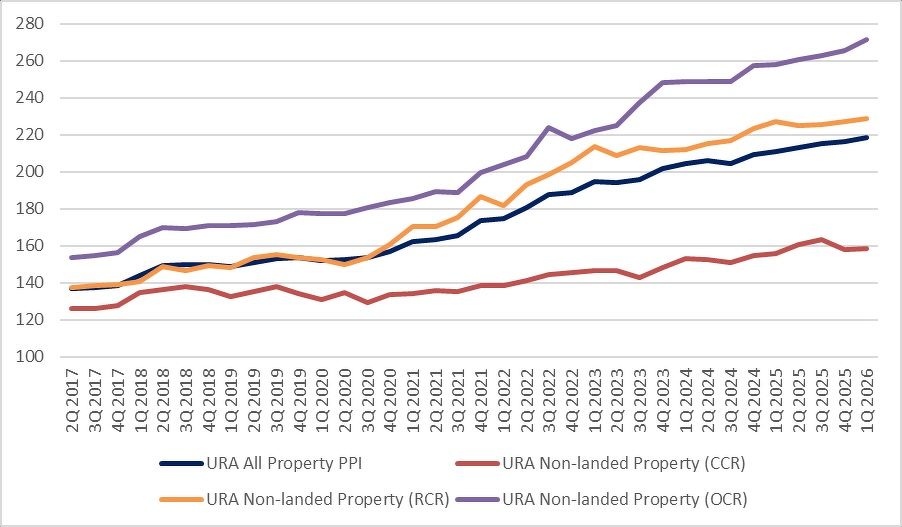

Private home prices in Singapore rose 0.9% q-o-q in 1Q2026, faster than the 0.6% increase in the previous quarter, and slightly above the average quarterly increase of 0.8% recorded in 2025.

It points to "possible stabilisation" in the private residential market, says Lee Sze Teck, senior director of data analytics, Huttons Asia. Price growth in 1Q2026 was supported by a rebound in non-landed property prices, led by suburban or Outside Central Region (OCR), which saw a 2.2% gain on the back of benchmark prices —an average of $2,546 psf — achieved at the launch of Pinery Residences.

URA Private Property Price Index

Source: URA

Landed property prices slipped 0.4% in 1Q2026, reversing the 3.4% jump in 4Q2025.

Non-landed property prices rose 1.3% in 1Q2026, a turnaround from the 0.2% decline in the previous quarter. OCR price growth was the strongest at 2.2% q-o-q, up from 1% the previous quarter.

Search for the latest New Launches, to find out the transaction prices and available units

In the prime Core Central Region (CCR), non-landed prices increased 0.6% in 1Q2026, following a 3.5% decline in the preceding quarter.

In the city fringe or Rest of Central Region (RCR), prices rose 0.8%, slightly higher than the 0.7% increase in 4Q2025.

Source: URA

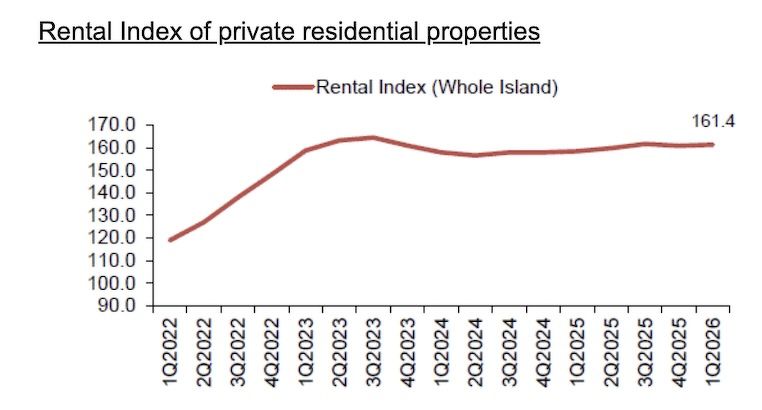

Rental market stabilises after prior decline

The overall private residential rental index rose 0.5% in 1Q2026, reversing the 0.5% decline in the previous quarter.

Rentals of non-landed private homes increased 0.4%, compared with a 0.1% drop in 4Q2025, while landed home rents edged up 0.1%, recovering from a 3% decline previously.

By region, non-landed rents in the CCR rose 0.5%, following a 0.7% increase in the previous quarter.

In the RCR, rents slipped 0.2%, reversing the 0.6% increase in 4Q2025.

Meanwhile, the OCR recorded the strongest rental growth, with rents rising 1%, compared with a 2% decline in the preceding quarter.

River Modern (above) sold 410 units (90.1%), while Newport Residences moved 184 units (75%) [Photo: GuocoLand]

New launches in 1Q2026 see strong take-up

On the supply side, developers launched 1,844 private residential units (excluding executive condominiums, or ECs) in 1Q2026, down from 2,632 units in the previous quarter. Sales also moderated, with 2,013 units sold, down from 2,940 in 4Q2025.

Four major non-landed projects — Narra Residences, Newport Residences, Pinery Residences and River Modern — were launched during the quarter.

Two of the projects, Newport Residences and River Modern, are located in the CCR, while Narra Residences and Pinery Residences are in the OCR.

The top three best-selling projects in 1Q2026 were Pinery Residences, Newport Residences and River Modern.

The first mixed-use development in Tampines West, Pinery Residences, sold 542 units, or 92.2% of its total units, making it the best-performing integrated development by take-up rate in Tampines, according to Huttons.

The 246-unit, freehold Newport Residences in the CCR moved 184 units (75%) [Photo: Samuel Isaac Chua/EdgeProp Singapore]

River Modern sold 410 units (90.1%), while Newport Residences moved 184 units (75%). The project attracted both owner-occupiers and investors due to its relatively accessible quantum and the strong rental prospects in River Valley, notes Huttons’ Lee. Meanwhile, buyers were drawn to Newport Residences’ freehold tenure, which remains rare in the CBD.

“The high sales take-up of more than 90% for Pinery Residences and River Modern was remarkable, given that they were achieved after the outbreak of conflict in the Middle East,” he adds. “This reflects buyers’ confidence in the mid- to long-term prospects of the Singapore property market, and possibly a flight to safety.”

Resale market sees pullback

Despite strong take-up in new launches, activity in the secondary market softened over the quarter. Overall transaction volume fell to 5,413 units in 1Q2026, down 19.2% from the previous quarter and 25.5% y-o-y.

The resale market recorded 3,225 transactions, down 8.6% from 3,529 in 4Q2025 and 9.5% y-o-y.

Sub-sale activity also eased, with 175 units transacted in 1Q2026, compared with 230 units in the previous quarter. According to Huttons’ Lee, sub-sales remain constrained by the longer seller’s stamp duty (SSD) holding period, which was extended from three to four years in July 2025.

Resale activity softened amid heightened uncertainty linked to the Middle East conflict. Based on caveats, resale transactions in March fell 7.3% m-o-m, as some buyers and sellers adopted a wait-and-see approach, he adds.

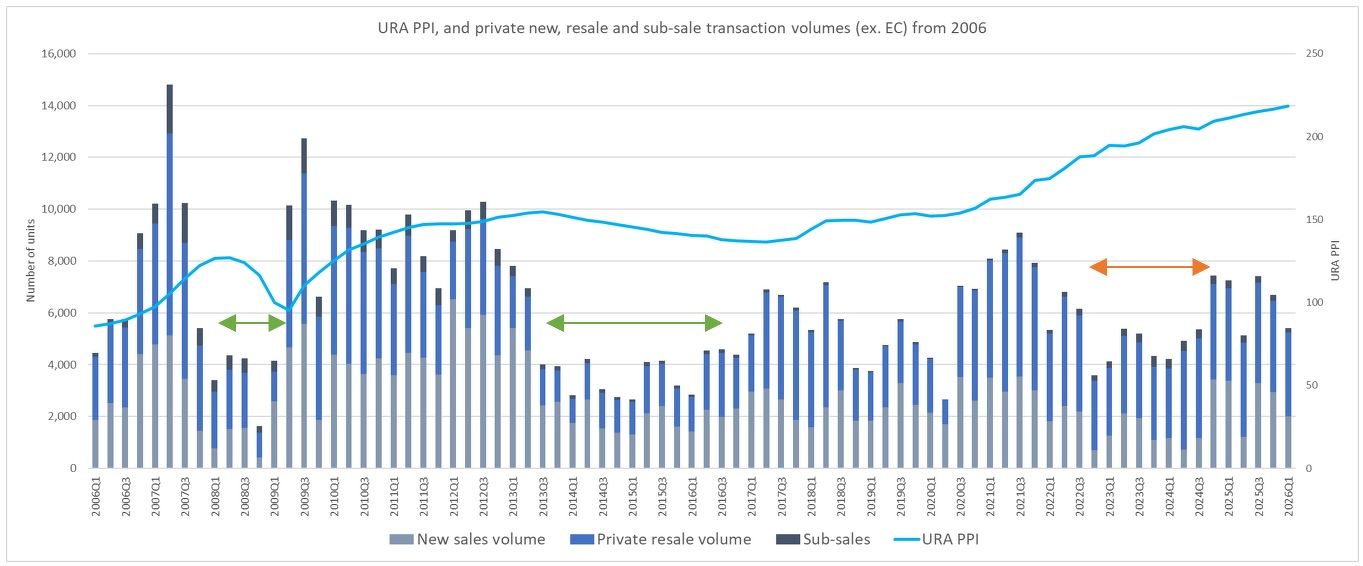

Private home prices 'less sensitive' to weaker sales

Prices of resale private homes slipped 0.5% q-o-q in 1Q2026 — the first decline since 3Q2024.

Based on PropNex's analysis of the URA private property price index over the last 20 years, private home prices have become "less sensitive " to weaker sales volumes post-Covid, notes PropNex CEO Kelvin Fong.

Prices have remained sticky and continued to climb despite slower sales during the period from around 2022 to mid-2024 (orange arrow in the chart), comapred with the period during the global financial crisis in 2008, notes Fong. During the stretch from mid-2013 to 2016, lower volumes had tracked quite closely with the decline in the PPI (green arrows).

Several factors have underpinned price stickiness in the market, notes PropNex's Fong. Stronger household balance sheets and rising wealth have improved owners’ financial resilience, he adds, while new launches continue to demonstrate pricing power. At the same time, unsold inventory remains at manageable levels, and speculative activity is more muted than in the 2007–2008 cycle.

In addition, robust growth in HDB resale prices in the post-Covid period has likely boosted upgraders' purchasing power, further supporting price resilience in the private housing segment, he reckons.

Landed housing in short-term ‘price stand-off’

Landed home prices, which slipped 0.4% in 1Q2026, saw transactions fall 20.2% q-o-q to 416 units over the quarter (Photo: Samuel Isaac Chua/EdgeProp Singapore)

Landed home prices slipped 0.4% in 1Q2026, while transactions fell 20.2% q-o-q to 416 units for the quarter.

The decline in sales may reflect a mismatch in price expectations between sellers and buyers. “The war in the Middle East could possibly have affected sentiment in the landed housing market,” says PropNex's Fong.

Marcus Chu, CEO of ERA Singapore, attributes the pullback in both prices and transaction volumes to a “price stand-off”, with sellers holding firm even as buyers turn more cautious.

“Despite the moderation, the landed market remains resilient, with the downturn reflecting a seasonal dip, as activity typically slows in the first quarter,” adds Chu. He expects the softness to be temporary, noting that the underlying demand for landed homes remains firm.

Landed Property Price Quantum: 1Q2026 vs 4Q2025

Source: URA as of 24 Apr 2026, ERA Research and Market Intelligence

“These properties continue to be regarded as a long-term store of value and a key wealth asset,” notes Chu.

He also believes the current interest rate environment will continue to support buying confidence among high-income earners, underpinning demand for landed homes.

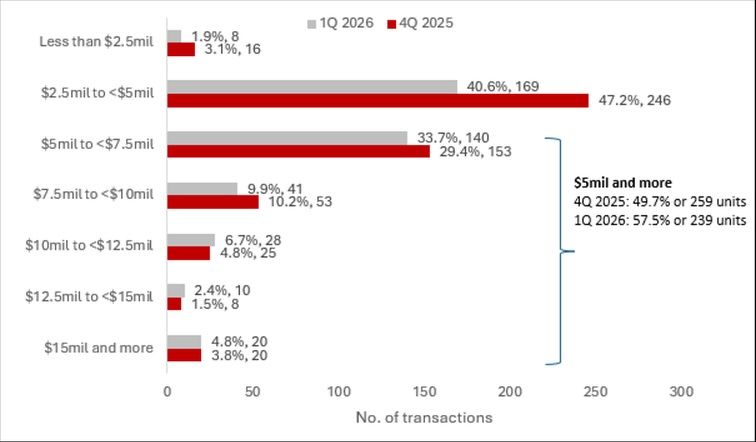

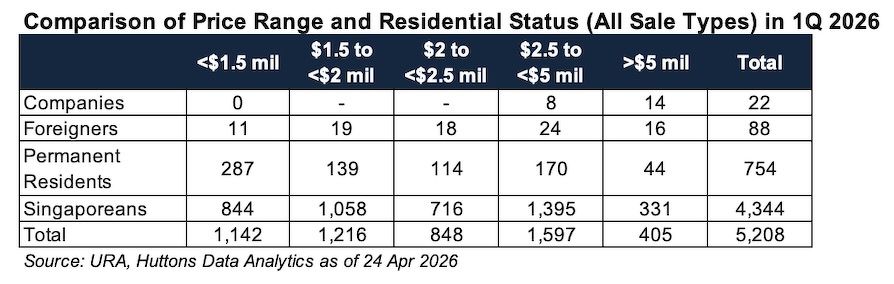

Singaporeans, PRs dominate high-value transactions

Singaporeans and permanent residents accounted for 97.9% of private residential purchases in 1Q2026, while foreigners made up just 1.7%.

The top five foreign buyer nationalities were from China, India, Malaysia, the US and Indonesia.

For the first time, transactions in the $2.5 million to below $5 million range formed the largest proportion of sales, notes Huttons. This may reflect the high level of wealth among resident households, as well as the strong take-up of CCR projects, says Lee.

A Singaporean purchased a unit at The Marq on Paterson Hill for $37 million, making it the top transaction in the non-landed property segment in 1Q2026 (Photo: Samuel Isaac Chua/EdgeProp Singapore)

Among the top transactions in 1Q2026 were units at The Marq on Paterson Hill, Seven Palms Sentosa Cove and 21 Anderson.

The $37 million unit at The Marq on Paterson Hill was purchased by a Singaporean, as were two units at Seven Palms Sentosa Cove. In contrast, a unit at 21 Anderson was acquired by a US citizen for $23.1 million.

Executive condo segment sees strong rebound

The EC segment recorded a sharp pickup in activity in 1Q2026. Developers launched two EC projects totalling 1,320 units and sold 1,168 units, compared with no new launches and just 80 units sold in the previous quarter.

Coastal Cabana, the first EC launch in the Jalan Loyang Besar area in 12 years, saw strong demand, with 593 of 748 units sold at a median price of $1,792 psf.

Coastal Cabana, the first EC launch in the Jalan Loyang Besar area in 12 years, saw strong demand, with 593 of 748 units sold at a median price of $1,792 psf (Photo: Qingjian Realty)

The 572-unit Rivelle Tampines moved 530 units, or 92.7% of its total units, at a median price of $1,937 psf, making it the best-selling EC by take-up rate in 2026.

“This reflects strong demand from eligible buyers for attractively priced projects, and continued acceptance of ECs as an alternative to private housing,” says Lee.

The 572-unit Rivelle Tampines moved 530 units, or 92.7% of its total units, at a median price of $1,937 psf, making it the best-selling EC by take-up rate in 2026 (Photo: Sim Lian Group)

Demand from second-timers was particularly robust, with allocated units snapped up within hours of launch.”

Meanwhile, the median price of ECs reached a high of $2,052 psf at Aurelle of Tampines.

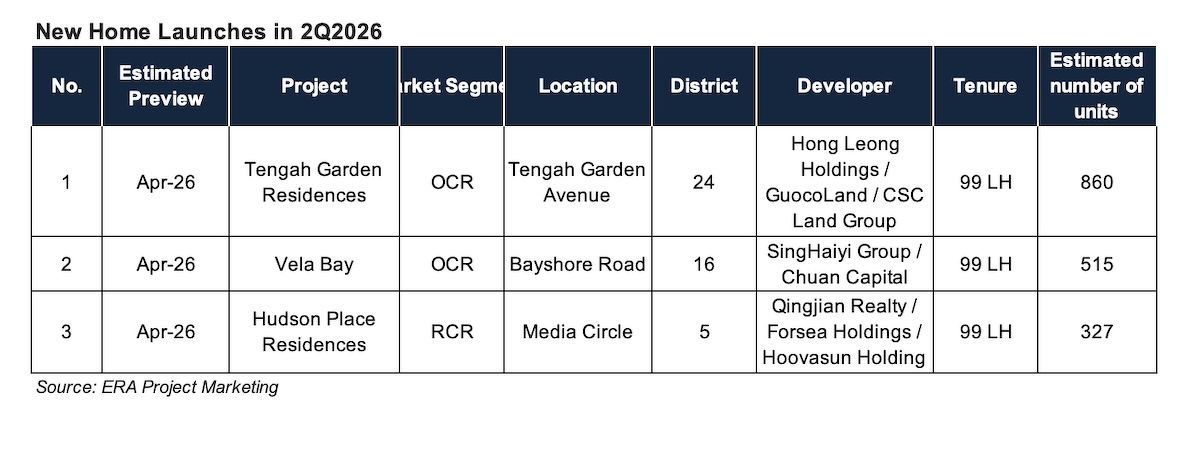

Upcoming launches

Upcoming launches in 2Q2026 include Tengah Garden Residences and Vela Bay in the OCR, as well as Hudson Place Residences in the RCR.

Sales momentum is expected to remain resilient in the OCR, underpinned by strong interest this weekend (April 25-26) at the 515-unit Vela Bay in the Bayshore precinct and the 863-unit Tengah Garden Residences in Tengah Town.

Both projects are located near existing or future MRT stations within precincts earmarked for transformation by URA. "They are likely to attract healthy demand from upgraders and first-time buyers seeking to tap into the areas’ longer-term growth potential," says Tricia Song, CBRE head of research for Singapore and Southeast Asia.

The 515-unit Vela Bay will be the first new private residential project launch in the new Bayshore precinct and scehduled for launch this weekend (Photo: Samuel Isaac Chua/EdgeProp Singapore)

Chu expects about 18 new private residential launches and five EC launches in total for 2026.

“These projects are located across all regions, offering a range of product niches that cater to buyers’ varied needs, such as affordability and locational preferences,” he says.

Supply pipeline rises as uncertainty lingers

The conflict in the Middle East has contributed to rising costs and slower growth momentum in 1Q2026, notes Huttons.

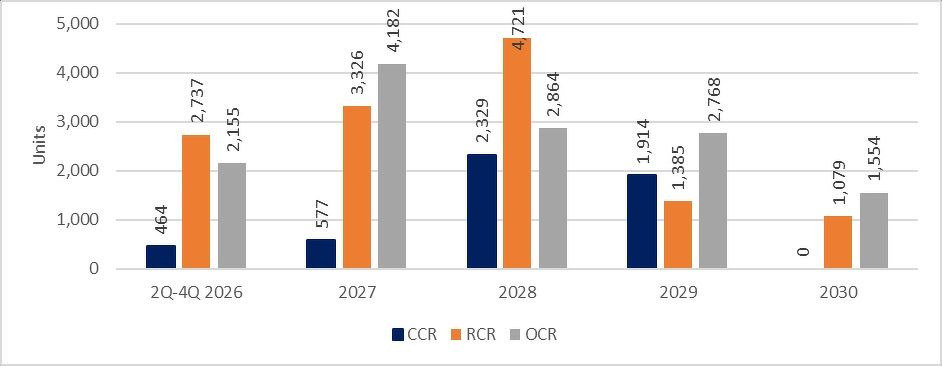

Looking ahead, about 55,800 private residential units, including ECs, are expected to be completed in the coming years.

This includes approximately 4,600 units from the Confirmed List of the 1H2026 Government Land Sales (GLS) programme — about 50% higher than the average half-yearly supply over the past decade.

"Momentum in the private residential market — underpinned by strong new launch take-up and relatively low unsold inventory — has continued to support developer confidence and landbanking appetite," says Wong Xian Yang, Cushman & Wakefield (C&W) head of research for Singapore and Southeast Asia.

In 1Q2026, unsold stock rose 8.1% q-o-q to 16,219 units, but remains below the 10-year average of 21,498 units.

Upcoming Private Residential Supply (Under Construction)

Source: URA, Huttons Data Analytics as of 24 Apr 2026

While the GLS programme remains the primary landbanking channel, the collective sale market is re-emerging as a source of freehold and well-located mid-sized sites, notes C&W's Wong.

Competition for GLS plots has also intensified, with the average number of bidders per site rising to 4.5 in 1Q2026, up from 4.2 a year earlier. Land prices have stayed firm, with recent deals such as the Dover Drive GLS site setting a new benchmark of $1,556 psf ppr in the RCR.

The en bloc market has also surprised on the upside, led by the $880 million sale of Loyang Valley in April — the first successful residential collective sale of the year. "While activity is expected to pick up, deals are likely to skew towards smaller, well-located sites, reflecting developers’ sensitivity to execution risks." says Wong.

'Prolonged conflict to weigh on demand'

Looking ahead, elevated energy prices — and the potential for higher construction costs — could temper bidding appetite, with developers likely to adopt a more measured approach to new acquisitions.

URA cautions that the macroeconomic outlook remains uncertain. “Households should continue to exercise prudence when purchasing property and taking out mortgage loans,” it says.

CBRE’s Song notes that while homebuying sentiment has held up amid low mortgage rates and steady income growth, a prolonged conflict in the Middle East could weigh on demand. “Buyers may become more discerning in their purchase decisions, especially given inflationary pressures from higher fuel and food prices,” she says.

In this environment, competitive and realistic pricing will be critical. CBRE Research projects that 7,500 to 8,500 new homes could be sold in 2026, down from 10,815 units in 2025 and slightly below the five-year average (2021–2025) of 8,766 units.

Correspondingly, private home prices — which rose 0.9% in 1Q2026 and are up 43.5% since the Covid trough in 1Q2020 — are expected to grow at a steadier pace, with CBRE forecasting full-year price growth of 2% to 4%.

Check out the latest listings for Pinery Residences, Rivelle Tampines, Narra Residences , Newport Residences, Coastal Cabana, River Modern properties

Ask Buddy

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search