Sitting on Goldmine – The Landed Housing Segment

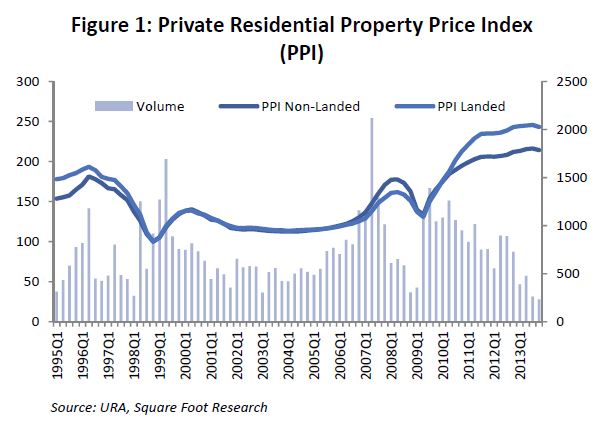

The private landed residential segment has outperformed its non‐landed counterpart for 12 consecutive quarters since 1Q10. Property prices have appreciated by 85.9% and 60.8% respectively in 4Q13 since the trough in 2Q09. However, there is more to it than just price performance when it comes to landed properties. We uncover a sub‐segment that has an unfair advantage.

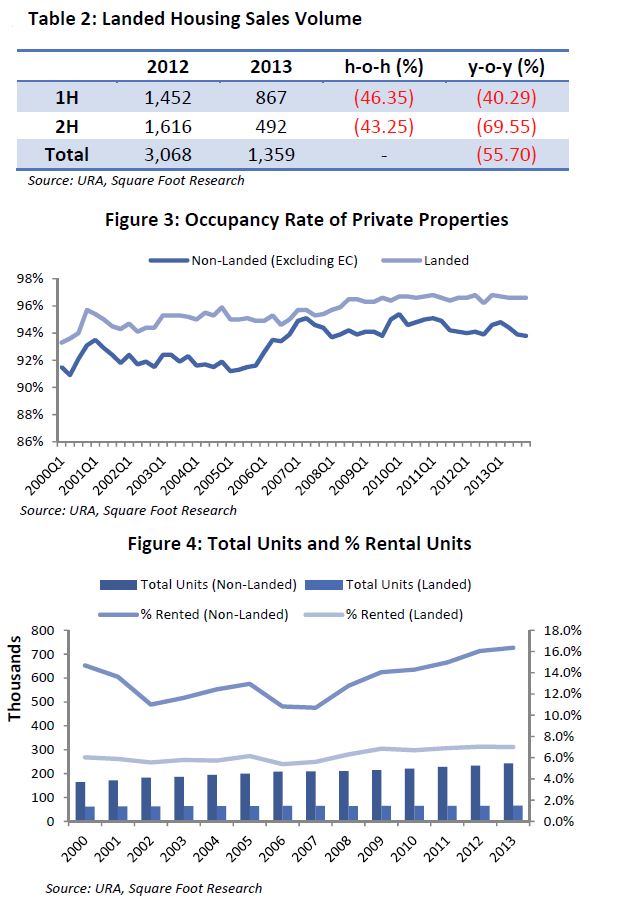

In 2013, the private landed residential property segment in Singapore registered the lowest number of transactions since 1995. Sales dived by 55.7% y‐o‐y from 3,068 transactions in 2012 to 1,359 transactions (excluding bulk sales) in 2013 despite its raving performance in terms of capital appreciation. Based on URA’s Property Price Index (PPI), landed property prices appreciated by 85.9% in 4Q13 since its last trough in 2Q09, whereas non‐landed property prices rose 60.8% during the same period.

Landed property prices have outperformed non‐landed property prices in two previous cycles. The first happened from 1993 to 1998 and the second, occurring 12 years later, from 2010 to the present (Figure 1). Owners who bought their landed properties during the peak of the cycle in 1996 were the worst hit when property prices toppled in tandem with the declining economy as a result of the Asian Financial Crisis. The property market remained bleak in the early years of the new millennium. Although the market recovered slightly in 1999 but the recovery was short‐lived as a result of a series of economic shocks that followed during the early 2000s such as the dot com bubble and SARS. Vacancy rate spiked to an average of 8%, the property market was oversupplied.

It took a good 7 years for the property market to recover. The oversupply in the property market was finally reversed in 2006 following a rapid increase in population, especially nonresidents with immediate housing needs, which brought back demand for housing. In addition, the onslaught of new launches as well as a growing interest from foreign investors also helped to invigorate the property market. Owners who bought their landed properties at the peak of the property market in 1996 finally saw the day when they could divest their decade long investment at a profitable price. Transaction volume (excluding bulk sales) in the secondary market grew by 40.1% y‐o‐y in 2006 and 54.4% in 2007 where it peaked with a total of 4,848 transactions, according to URA.

Foreign Ownership

In general, the private landed residential market can be divided into 3 main classes, namely, Good Class Bungalows (GCB), conventional landed units and strata landed units. Unlike non‐landed properties, foreigners are not allowed to purchase landed properties (restricted residential property under the Residential Property Act) with two main exceptions, (1) landed units located in Sentosa Cove, in which approval from the authority is still required and (2) strata landed units built within a nonlanded development that has been accorded Condominium status.

Foreigners who are interested to buy landed properties beyond the two exceptions can seek approval from the Singapore Land Dealings (Approval) Unit if they are permanent residents. The applicant would need to go through a stringent screening process and fulfill criteria such as having significant contributions to Singapore’s economy. Successful candidates are then entitled to purchase only 1 landed home in Singapore slated for their own occupancy.

Appeal of Landed Housings

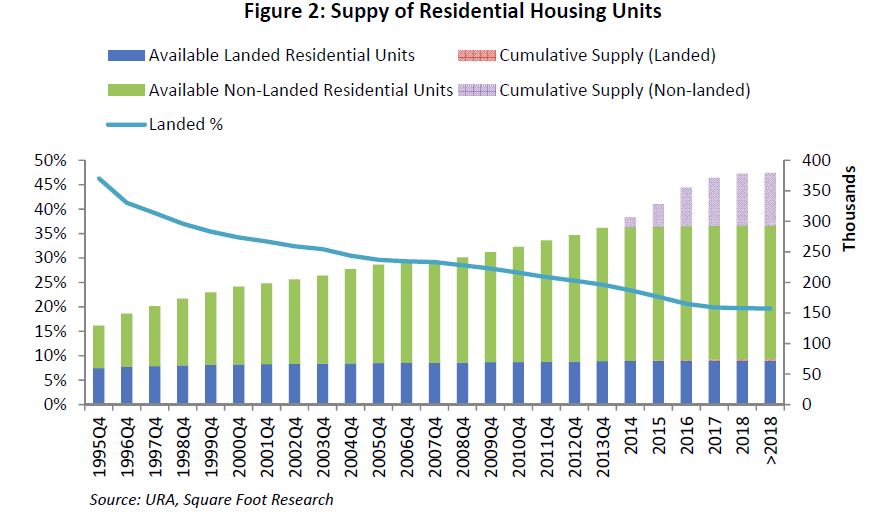

The landed segment of the private residential market is mainly driven by home‐stayers’ penchant to own a landed house, which is often associated with prestige and exclusivity. In addition, the scarcity of land in the second most densely populated country in the world heightens the appeal and intrinsic value of landed housing in Singapore. As Singapore continues to grow its population from the current 5.4m to the estimated 6.9m in 2030, the need to optimise and intensify land usage will translate to a declining proportion of landed housings in Singapore, adding on to its appeal (Figure 2).

Landed housings are less susceptible to speculative purchases due to its high premium, which raises the entry bar. The restriction imposed on foreigners acts as a safety net to prevent speculative bubbles from arising as the inflow of ‘hot money’ brought about by foreign investors will have limited impact on this segment of the property market. A good proportion of landed units are bought for owner occupation as seen from the significantly higher occupancy rate and low rental volume relative to nonlanded units (Figures 3 and 4). Occupancy rate of landed housings is also observed to be relatively more stable.

However, as the segment sees low volume, average prices can fluctuate widely in the short to medium term if market conditions turn unfavourable. The ability to tide through difficult period is essential to getting the most out of the segment, financially speaking.

Recent Trends

The private residential market reached its pinnacle in 3Q13 where the landed segment appreciated 87.8% since its last trough in 2Q19 and 27% peak to‐peak since its previous historical high in 2Q96 whereas its non‐landed counterpart grew by 62.3% and 19.2% respectively during the same period. Sales in the landed segment, however, remained feeble with transaction volume falling by 55.7% y‐o‐y to only 1,359 transactions in 2013, the lowest since 1995. The significant drop in sales in 2H13 (Table 2) may be inherent to the introduction of total debt servicing ratio (TDSR) introduced in 3Q13, where the tighter financing rules may have a direct impact on one’s buying power. A collective decline in prices across all landed types, the first since 2Q09, observed in 4Q13 may hint at a price correction in the landed segment as we move towards a buyer’s market.

Freehold versus Leasehold

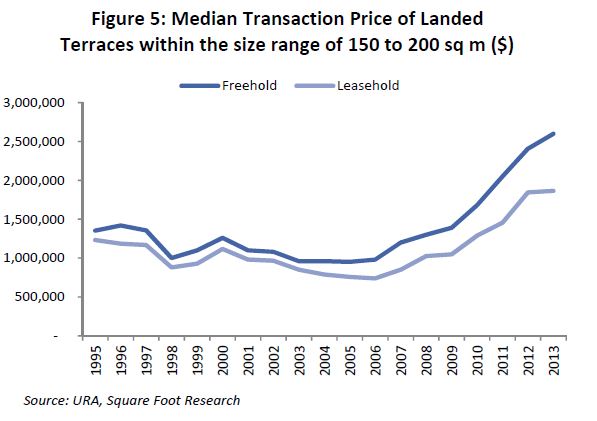

Freehold landed properties (including 999‐year) have been shown to be more resilient. In terms of capital appreciation, freehold landed properties performed better than leasehold landed properties (Figure 4) with price growth of 96.5% (nearly doubled) and 74.1% respectively from 2Q09 to 4Q13. This is also evident from the widening gap between median transaction price for freehold landed terrace and median transaction price for leasehold landed terrace (Figure 5).

Strata Landed

Unlike conventional landed housings, owners of strata landed do not actually own the land title but rather the strata title of their landed units. Similar to high‐rise developments, strata‐titled cluster housings/townhouses get to enjoy communal facilities where owners collectively maintain by paying a fee monthly. Another key difference is that a landed unit can be rebuilt whereas a strata‐titled landed unit cannot be rebuilt on its own.

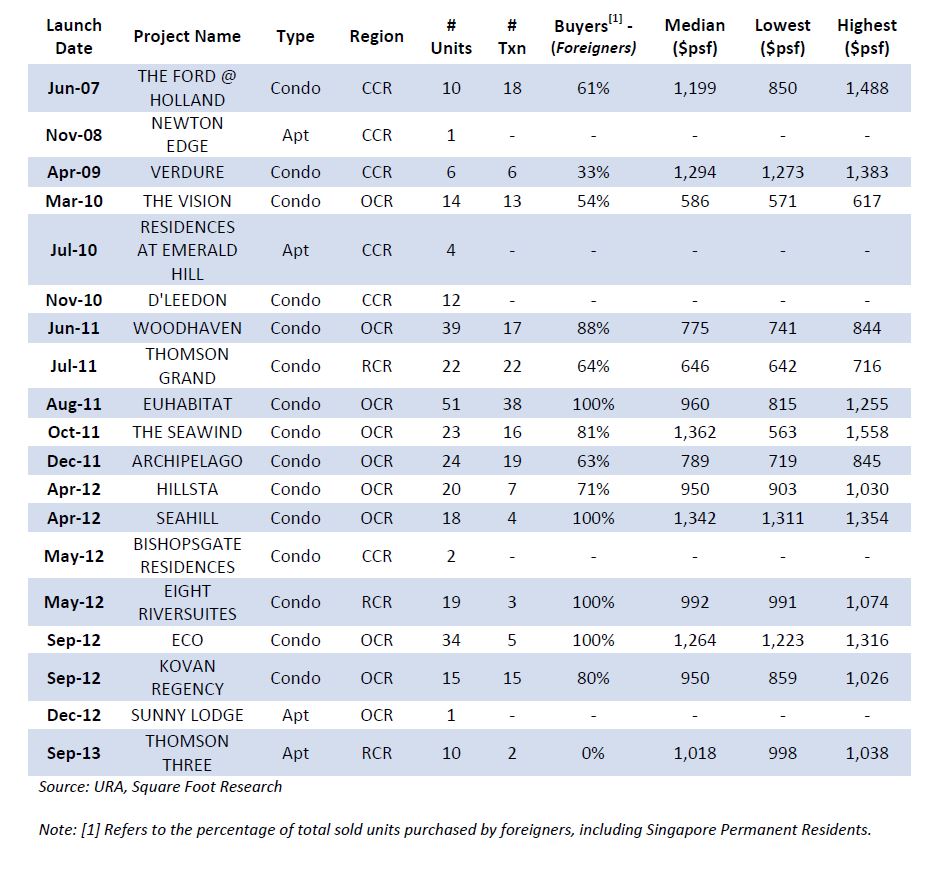

As described previously, foreigners are generally not allowed to own landed properties with two main exceptions. Purchasing a strata‐titled landed unit within a development with Condominium status is the only option where approval is not required. However, this avenue has been tightened in 2012 after URA announced that it will no longer grant condominium status to new high‐rise developments that comprise strata‐landed units, thus limiting the number of such developments available. We believe this category of landed properties will do well given that it remains the only avenue where foreigners are able to purchase without approval. In fact, about 75% of the total buyers of landed units in this category are foreigners based on new projects launched since 2007 (Table 3).

Conclusion

A decreasing proportion of landed housing bodes well for the segment. The 1H2014 GLS Confirmed List is expected to yield more than 4,600 new non‐landed units but not any landed units. Similarly, the 1H2014 GLS Reserve List does not have any landed residential sites. In areas where the government still has a stockpile of vacant sites such as Sengkang and Punggol, the current supply of landed units is not expected to increase in the future (except for cases where existing landed units are collectively purchased and developed into more units), as all of the residential sites have been set aside for high‐rise developments, based on details from the Draft Master Plan 2013.

Landed properties may not be the best segment to invest if a quick return is expected. Due to its high price tag, rental yield is generally unattractively low. In addition, due to the low transaction volume, average prices can fluctuate widely so speculators can be caught wrong‐footed should market conditions turn unfavourable quickly. However, due to its increasing scarcity, we believe the segment remains fundamentally attractive in the long run.

Strata Landed in High-rise

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search