Galloping into 2026: Singapore’s residential market powers ahead

With so many choice projects in the pipeline, particularly in the Outside Central Region, new home demand is expected to continue being driven by HDB upgraders (Picture: Samuel Isaac Chua/EdgeProp)

2025 looks set to be an intriguing year. Key events, such as “Liberation Day,” have intensified the trade war, thereby raising geopolitical risks. Nonetheless, the bright side is the lower interest rate environment, following the Fed’s successive rate cuts aimed at managing inflation and supporting employment. This continues to bolster global liquidity and risk appetite.

The signs are clear: we are likely to experience more significant structural changes in global trade and capital flows as economies adapt to new geopolitical realities in the medium to long term.

Despite the underlying headwinds, Singapore’s economy and financial markets have demonstrated notable resilience, forging their own path. The optimism has carried over to the Singapore residential market, which has achieved its strongest performance since 2021, with impressive sales volumes.

New home sales in the first ten months of 2025 has exceeded 10,000 units, while transactions in the secondary market remained steady at around 12,000 units during the same period. However, the bigger question remains: can this momentum be sustained through to 2026, and what new forces are expected to shape the market in the year ahead?

In the true ERA spirit, let us share our outlook for 2026 as we gallop into the year of the H-O-R-S-E, a perfect metaphor for momentum and strength expected for the residential market ahead.

Homebuyers shifting from HDB to the private market as rules tighten

From the rise in Build-to-Order (BTO) supply and the HDB’s reclassification framework, to the reduced HDB loan quantum and the latest shift towards the Voluntary Early Redevelopment Scheme (VERS) from the Selective En-bloc Redevelopment Scheme (SERS), all these steps send a clear message.

That is, HDB aims to curb resale price growth and steer the market towards a more sustainable rate of price increase.

Generally, the tightening of regulations has had positive effects on the market. For example, in the first nine months of 2025, the HDB Resale Price Index increased by an average of 1% q-o-q, down from 2.3% during the same period in 2024.

Some might argue that the number of million-dollar HDB flats continued to rise in 2025, with 1,336 units sold in the first ten months, already surpassing the 1,035 units recorded for the entire 2024. However, the reclassification framework could help further slow price growth over the next decade as Prime flats gradually enter the resale market.

Limited by the resale income cap and subsidy clawback, Prime flats are unlikely to see runaway prices like newer, centrally located resale flats. Instead, they may be more likely to experience a slower, more sustainable rate of price increase over time.

Additionally, once the VERS programme is implemented, the HDB resale price trajectory may also slow down further, reinforcing a more stable and fair housing market that reflects the long-term balance of lease tenures.

In the long term, HDB flats will continue to provide value-for-money housing options, but the chances of significant capital gains may decline.

For those aiming to benefit from better future price growth, the private home market might offer more promising upside potential, and here is why.

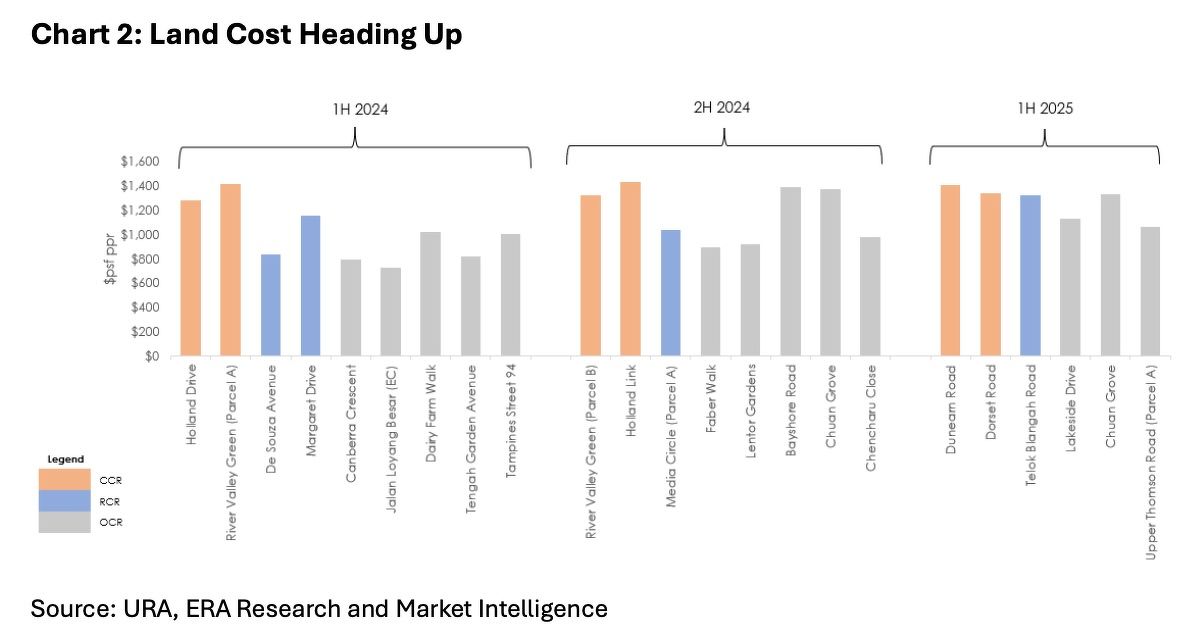

Ongoing rise in land costs keeps home prices resilient

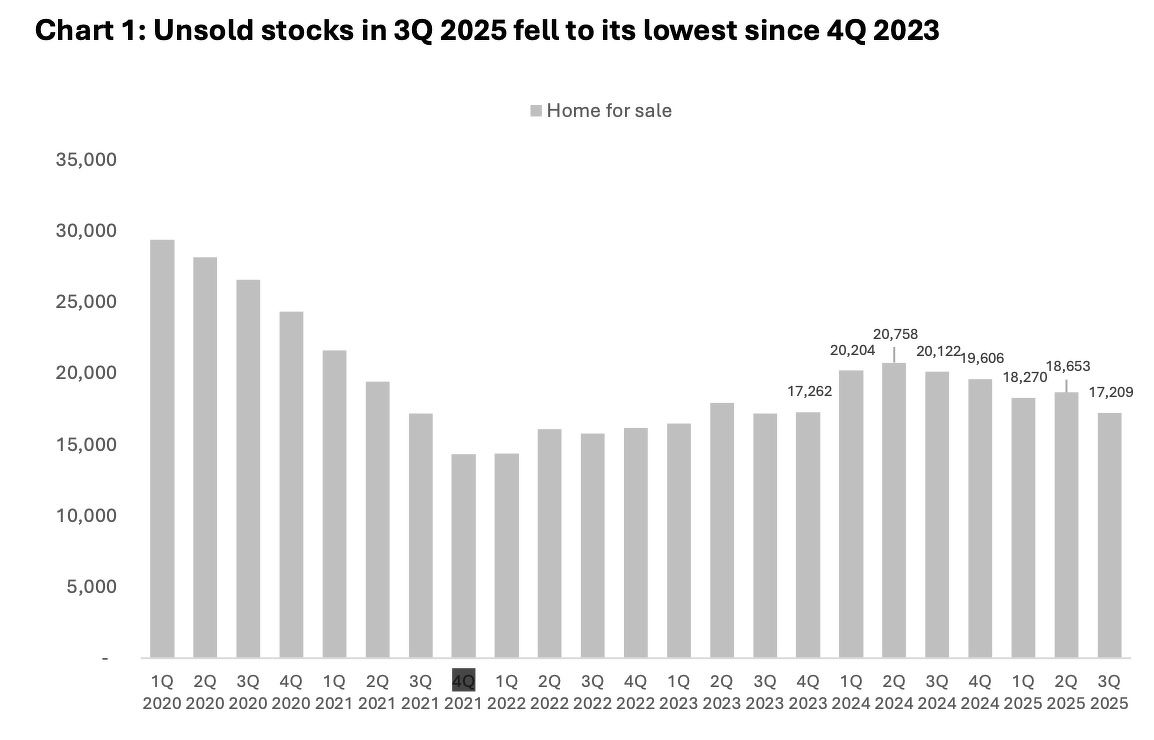

Throughout 2025, overall land prices increased noticeably, though at different rates across various market segments. The consistent decline in unsold inventory mainly supported this trend. In simple terms, the strong demand at recent launches has further decreased the supply of available units for sale, leaving some developers with diminishing stock and a growing urgency to restore their land banks.

Source: URA, ERA Research, market intelligence

Unsurprisingly, as more developers gravitate towards sites with strong locational attributes, land prices have continued to rise.

Simultaneously, the release of the Draft Master Plan 2025 has revealed new housing opportunities across the island. Emerging residential precincts such as Bayshore Road have drawn increased interest and competition among developers. As a result, several sites in the Outside Central Region (OCR), including Bayshore Road and Chuan Grove, have established new benchmark land prices.

Overall, the higher land costs have created a new baseline for home prices when these new projects come to market.

Renewed wave of OCR launches

Not only was 2025 a booming year for new home sales, but it was also the year when the Core Central Region (CCR) saw a resurgence, driven by a wave of launches that rekindled interest in the luxury segment. The momentum is expected to continue into 2026, with attention shifting towards the OCR market.

Altogether, we anticipate approximately 18 project launches in 2026, leading to around 9,500 private residential units. Furthermore, as many as five executive condo (EC) projects might be introduced, adding a further 2,300 units to the pipeline. Of these, nine projects are situated within the OCR, while the Rest of the Central Region (RCR) and CCR could see about four and five launches, respectively.

With so many choice projects in the pipeline, particularly in the OCR, new home demand is expected to continue being driven by HDB upgraders. That said, another key factor shaping home sales is interest rates. In the following section, we explore why we believe rates will continue to ease, further supporting market momentum.

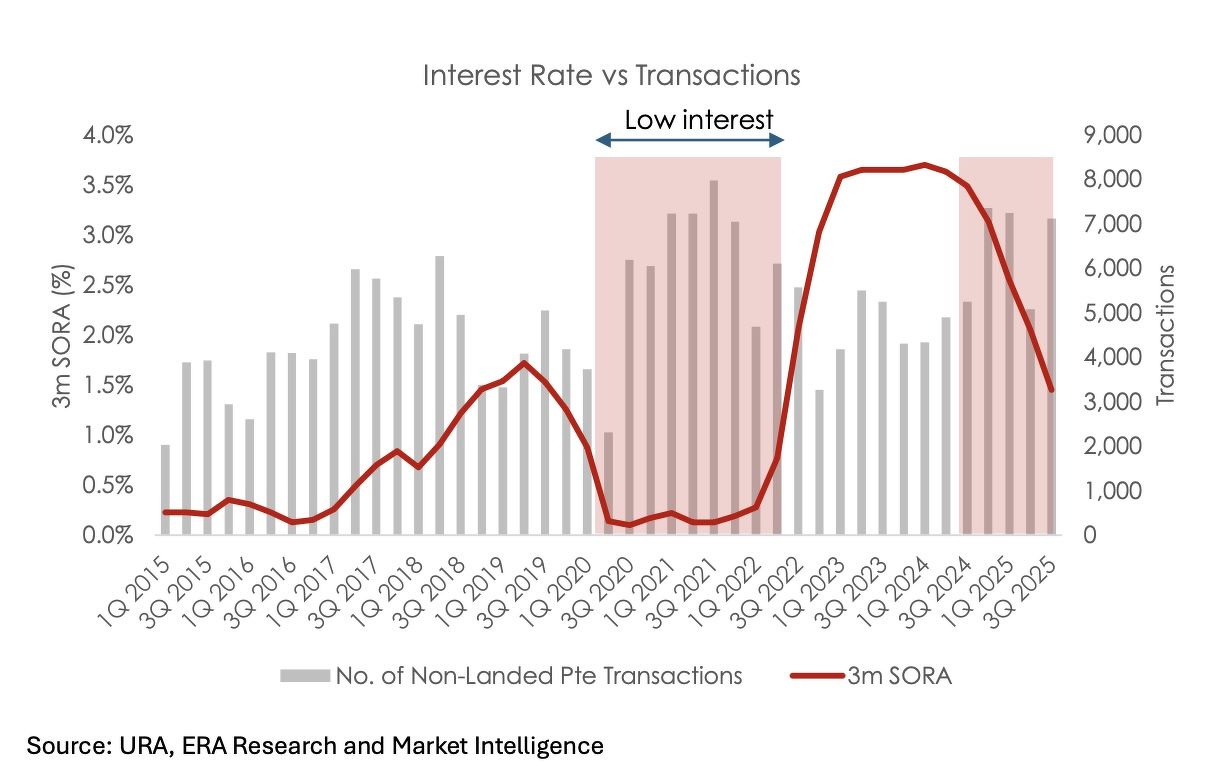

Stable (markets) gallop ahead as interest rates ease, spurring transactions

The Federal Reserve’s (Fed) first interest rate cut in September 2024 provided the residential market with a much-needed respite. Since then, the market has continued to grow; strong sales were supported by positive sentiment, a series of new home launches, and lower borrowing costs, even amid major events like the “Liberation Day”.

New home sales in the first ten months of 2025 have exceeded 10,000 units, reaching the highest level since 2021, while secondary market transactions remained steady at around 12,000 units during the same period.

Given the increased economic uncertainty, analysts surveyed by CME FedWatch anticipate that the Fed will keep interest rates low for the next 24 months.

Generally, this could continue to boost homebuying activity and help maintain transaction momentum even as broader economic challenges persist.

Expect prices to rise higher, but waiting may cost more

Summarising our discussions, 2026 could be another promising year for Singapore’s residential market, as long as there are no unforeseen setbacks. Over the long term, DBS projects Singapore’s economy could reach S$1.5 trillion by 2040, supported by strong GDP growth and a resilient Singdollar, with the STI potentially rising to 10,000.

Against this backdrop, demand fundamentals remain strong, supported by a stable labour market, ongoing income growth, and healthy household balance sheets.

For buyers who remain undecided, hesitation could end up costing them later.

Upcoming launches are expected to attract significant interest, especially in well-connected and amenity-rich neighbourhoods. Waiting too long might mean missing the current opportunity and watching prices surge towards the next peak.

Marcus Chu is the CEO of ERA Singapore

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search