New private home sales in December sluggish in holiday lull; full-year volumes highest since 2021

Developers sold 197 new units in December, down 39.4% from November. But the 2025 tally hits a multi-year high.

Ask Buddy

Amid a dearth of new launches during the holiday season, Singapore property developers sold a total of just 197 new homes — excluding executive condominiums (ECs) — in December 2025, according to data released by the Urban Redevelopment Authority (URA) on Jan 15.

New private home sales sank by 39.4% from the 325 units sold in November, dipping for a second consecutive month, as many prospective buyers were on holiday and developers typically held off on their launches during the year-end festivities. On a year-on-year basis, it inched down by 3% from the 203 units shifted in December 2024.

This takes the 2025 full-year tally of new homes sold by developers to about 10,821 units, according to Huttons Data Analytics estimates — a surge of 67.3% from the 6,469 units in 2024 and the highest annual volume since 2021, when 13,027 transactions were recorded.

Explore comprehensive data about all ECs, including the average profit at 5 and 10 years

The strong sales across the whole of 2025 could be due to a combination of factors, including the substantial decline in interest rates which has lowered borrowing costs and thus enabled more buyers such as young families and HDB homeowners to upgrade, said Christine Sun, chief researcher and strategist of Realion (OrangeTee & ETC) Group.

There were also many large-scale project launches in attractive locations that appealed to many buyers during the year, Sun added. Meanwhile, the global economy stabilised more quickly than anticipated amid US tariff tensions, and Singapore’s economic performance exceeded expectations, in part boosting property buyers’ confidence and improving market sentiment.

Mohan Sandrasegeran, head of research and data analytics at SRI, noted that transaction volumes in 2025 surpassed 2024 levels across all market segments.

“The broad-based improvement across all regions points to a more active and balanced primary market in 2025. This recovery was supported by a ramp up in government land sales (GLS) supply from earlier awarded GLS sites, stabilising interest rate conditions and a more confident buyer pool,” he said.

Newmark director and head of research, Wong Shanting, observed that rising HDB flat prices have narrowed the price gap between HDB flats in mature estates with new private homes in the Outside Central Region (OCR) or suburbs, prompting some buyers to seize the opportunity to upgrade to the condominium segment.

Limited fresh supply

Sustaining the recent lull in new launch activity, 52 units were launched for sale in December. This is 85% lower than November, though 160% higher than the previous year, when there was no new project launch in December 2024, said Huttons Asia CEO Mark Yip.

Transactions were thus primarily driven by existing launches rather than fresh supply.

Only one new project was put on the market last month: the 186-unit Pollen Collection II landed housing development by Bukit Sembawang Estates, in the Seletar Hills landed enclave in District 28 in the OCR.

With the average quantum for a resale terrace house reaching $4.4 million in 4Q2025, the average quantum of $4.29 million for a new terrace house in Pollen Collection II “offers a very compelling proposition”, says Yip from Huttons. Earlier, the 132-unit Pollen Collection had been launched in January 2023.

Previously, in November, only one non-landed project, the 347-unit The Sen by Sustained Land, made its debut in the market. October had recorded four new launches.

Buyer interest is expected to re-emerge once new supply enters the market, as the moderation in sales reflects timing and launch dynamics rather than a weakening of underlying demand, said SRI’s Sandrasegeran.

With several projects slated to go on the market soon, new home sales are expected to pick up in January. Upcoming launches include the 246-unit Newport Residences along Anson Road in the central business district, the 540-unit Narra Residences at Dairy Farm in the OCR, and the 748-unit Coastal Cabana EC in Pasir Ris.

City fringe housing drive activity

Sales in the Rest of Central Region (RCR) or city fringe made up more than half of the month’s transaction volume.

Demand was supported by a tight supply of new homes in the area, with only 417 units remaining and no upcoming launches currently slated for the highly sought-after RCR district, said Marcus Chu, CEO, ERA Singapore.

The Continuum, developed by Hoi Hup Realty and Sunway Developments, topped the list with 31 homes sold in the month, at a median price of $2,498 psf. Of the 31 units sold, 22 of them are smaller homes spanning about 650 sq ft each, according to caveats lodged, PropNex noted. The freehold development along Thiam Siew Avenue has sold 672 out of its 816 units, or 82%, since it was launched in May 2023.

Tricia Song, CBRE head of research, Singapore and Southeast Asia, noted that The Continuum’s robust take-up came as it dangled a “one price” promotion for the one-bedroom-plus-study units starting at $1.338 million, implying a discount of about 10–15% from its launch price of $2,800 psf. “The price looks attractive for a freehold project in a RCR location, comparable to most of the 99-year leasehold projects in an equivalent location,” she said.

Another project that supported sales in the RCR was Nava Grove, jointly developed by Sunway MCL and Sinarmas Land, which moved 15 units at a median price of $2,641 psf. Sales for the 552-unit, 99-year leasehold development in District 21 kicked off in November 2024. It was 94% sold as at the end of December, according to PropNex.

Meanwhile, in the OCR, developers sold 67 new homes (excluding ECs). The newly launched Pollen Collection was the best-selling in this sub-market, with buyers scooping up 17 of its landed homes in December at a median price of $2,599 psf.

Over in the Core Central Region (CCR), developers’ sales fell to 20 units in December, from 30 units in the previous month. Clocking the highest volume was UpperHouse at Orchard Boulevard, which sold seven units at a median price of $3,410 psf.

Executive condo sales pick up

As for executive condominiums or ECs, 37 units were transacted — the highest monthly volume in the quarter, according to ERA Singapore. This is up by 76% from the 21 units moved in November.

The most popular EC project in the month was again the 600-unit Otto Place in Tengah, which accounted for 28 units sold or 75.7% of total new EC sales in December, said Marcus Chu, CEO, ERA Singapore. These went at a median price of $1,571 psf.

With the Coastal Cabana EC project coming on the market in January, EC sales are likely to see a “big boost”, given that demand tends to be strong for such housing among first-time homebuyers and HDB upgraders, said Wong Siew Ying, Head of Research and Content, PropNex. As at the end of December, there were just 17 unsold new EC units available, based on URA data.

Prime and luxury market muted

Buying activity for luxury properties was subdued in December, with only four new non-landed homes sold for between $5 million and $10 million, according to Realion’s Sun.

These four units were from Watten House, Union Square Residences, Aurea, and The Reserve Residences, which sold for S$5.06 million, S$5.23 million, S$5.68 million, and S$6.72 million, respectively, she said.

For the ultra-luxury segment, or those $10 million and above, only one transaction was recorded in December, down from two in the previous month. The sole unit was a 4,489 sq ft unit on the fifth storey at 21 Anderson, which changed hands for S$23.3 million, Sun noted.

Buyer profile

Singaporeans continued to dominate the market in December, accounting for 88.1% of new private home sales, excluding ECs, or 208 units, Chu from ERA said.

Overall, more than half of the sales during the month were in the range of $2.5 million to less than $5 million. That makes it the fifth consecutive month where the bulk of sales were in the price range, with the launch of Pollen Collection II partly contributing to it, Huttons’ Yip pointed out. Singaporeans made up more than 80% of the buyers of properties in this price range.

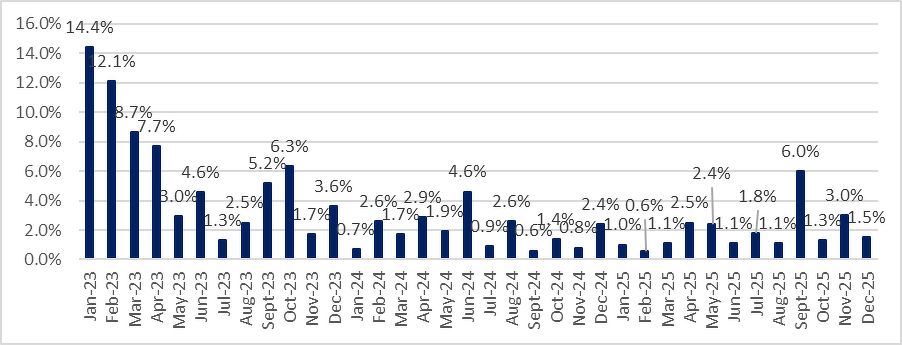

A foreigner purchased the 4,489 sq ft unit at 21 Anderson. In 2025, the proportion of foreign buyers was 1.4%, similar to 2024, but a steep drop from the 11.5% in 1Q2023 before the additional buyer’s stamp duty (ABSD) was increased to 60% for foreigners buying a residential property in Singapore, said Yip from Huttons.

Proportion of purchases by foreigners:

Source: URA, Huttons Data Analytics as of Jan 15, 2026.

Demand may stay resilient in 2026

Attention now turns to how much of 2025’s momentum can be carried into 2026. Buyers can look forward to a pipeline of 18 private residential projects and five EC launches slated for the year. While this is fewer than 2025, which saw 24 private developments and 2 EC launches, demand is expected to remain robust, Chu from ERA noted.

Newmark’s Wong foresees demand for new private homes this year being uneven across locations, although projects in locations that have not seen new launches in recent years could benefit from stronger pent-up demand.

Overall, the outlook for the 2026 new sale market remains stable, in SRI’s view. While sales volumes may ease from the “exceptional” levels of 2025, buyer demand is likely to stay resilient, said Sandrasegeran.

He added that a strong GLS pipeline has provided developers with sufficient opportunities to replenish their land banks, and developers today are more disciplined in managing project releases, responding to buyer absorption rates and prevailing market conditions. This has resulted in a steadier and more orderly flow of new launches.

Realion reckons some 8,500 to 9,500 new homes may be sold this year, which will be less than the 10,821 new units sold in 2025, but more than the 6,469 units transacted in 2024.

CBRE Research predicts buying sentiment and appetite remaining strong, though sales volumes may ease to about 7,500 to 8,500 sold this year, amid fewer launches expected and as interest rate declines taper, said Song.

Prices of private homes, which rose 3.4% in 2025 (based on 4Q2025 flash estimates), could grow at a slower or similar pace in 2026, in CBRE’s view.

Huttons predicts transaction volumes to total between 8,000 and 10,000 units for the whole of 2026, with prices estimated to grow about 2–5%.

For more news and analysis, read our weekly e-paper. Prefer a print copy? Get it delivered to your home every Monday.

Ask Buddy

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search