Non-landed residential land betterment charges rise 4.1% in strongest uptick since 2022

Sector 50 saw a 3.2% increase, with the sale of the first GLS plot in Tanjong Rhu since 1997 attracting a top bid of $1,455 psf ppr (Photo: Albert Chua/EdgeProp Singapore)

The land betterment charge (LBC) rates for the March–August 2026 cycle have been raised across several use groups, led by a 4.1% increase for non-landed residential (B2) — the largest revision since September 2022.

Landed residential (B1) rates rose 4.0% on average, industrial (D) increased 3.2%, while commercial (A) edged up 0.5%. Hotel (C) rates remained unchanged, says Chua Yang Liang, head of research and consultancy, Southeast Asia, JLL.

The LBC is payable when landowners enhance a site’s value — whether through rezoning, intensifying plot ratio or topping up a lease. Revised twice a year, the rates reflect the government’s assessment of underlying land values across different sectors.

According to Mark Yip, CEO of Huttons Asia, the 4.1% increase for non-landed residential is the largest since September 2022. He attributes the upward revision to robust developer interest, supported by lower interest rates that have eased borrowing costs.

The revision also comes on the back of stronger-than-expected economic growth, says Tricia Song, head of research for Singapore and Southeast Asia at CBRE.

“It has boosted homebuying sentiment, with new home sales rebounding to a four-year high of 10,815 units in 2025,” says Song.

Developers’ sales in 2025 were the strongest since September 2022, adds Yip. Strong take-up rates at project launches renewed urgency among developers to replenish their land banks. Lower financing costs in 2025 also enhanced developers’ ability to bid more competitively for government land sale (GLS) sites amid intensifying competition.

“On the other hand, higher LBC rates may discourage collective sales of ageing 99-year developments, as the premium required to top up to a fresh 99-year lease has increased,” Yip notes.

With just one small residential collective sale concluded in the preceding half-year, revisions for the B2 group largely tracked performance at GLS tenders, says Song.

While the new LBC estimation tool on onemap.gov.sg is useful for developers and owners in the collective sale market, “it will not materially improve the probability of a sale,” observes Yip. “A realistic selling price and the development’s locational attributes remain the key determining factors.”

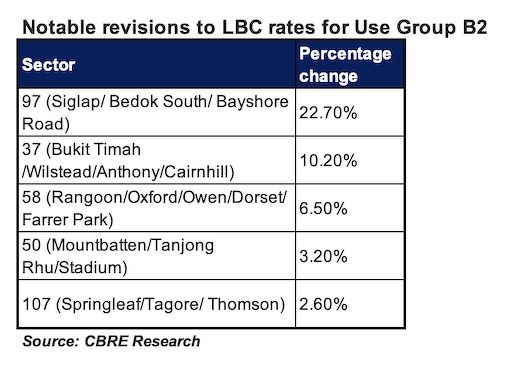

Residential non-landed (B2)

Within the non-landed residential (B2) group, Sector 97 recorded the sharpest increase of 22.7%, largely driven by the 10 bids received for the Bedok Rise GLS site next to Tanah Merah MRT Station. The site was awarded at $1,330 psf per plot ratio (ppr).

Sector 37 rose 10.2%, supported by the Bukit Timah Road GLS site, which attracted a top bid of $1,820 psf ppr — the highest land bid for a Core Central Region (CCR) site since Cuscaden Road in May 2018.

Meanwhile, Sector 50 saw a 3.2% increase, with the sale of the first GLS plot in Tanjong Rhu since 1997 attracting a top bid of $1,455 psf ppr.

Sector 115 increased 7.1%, with the executive condo (EC) site at Woodlands Drive 17 drawing a top bid of $794 psf ppr.

Meanwhile, Sector 50 climbed 3.2%, following the sale of the first GLS site in Tanjong Rhu since 1997, which garnered a top bid of $1,455 psf ppr.

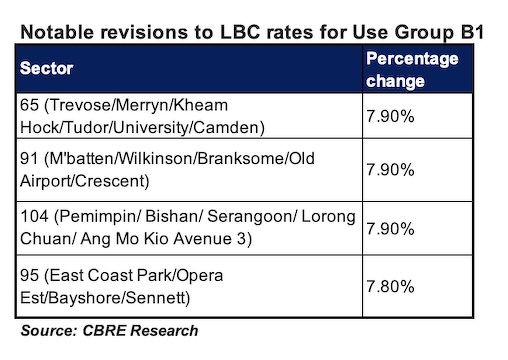

Landed residential (B1)

Landed residential (B1) rates rose 4% on average. The increase was supported by firm home prices, including recent Good Class Bungalow (GCB) transactions such as the $148 million sale at Peirce Road, the $61 million sale at Dalvey Road and a $60 million deal in Dalvey Estate, notes Huttons’ Yip.

“The largest increase for landed residential sites was recorded in Sector 98, spanning Tampines, Simei and Bedok, pointing to firmer underlying land values in the East,” says Marcus Chu, CEO of ERA Singapore. “Landed homes in these estates continue to see resilient demand, particularly from affluent owner-occupiers upgrading within the region.”

Chu adds that double-digit LBC adjustments across several CCR sectors reflect “sustained confidence in Singapore’s prime landed segment and the long-term value of centrally located housing”.

He highlights central areas around Mount Emily and the Monk’s Hill/Newton neighbourhoods, which stand to benefit from rejuvenation plans under the URA Master Plan 2025. “Plans such as the Monk’s Hill Linear Park will enhance connectivity between Newton and Emerald Hill within the prime Orchard precinct,” says Chu.

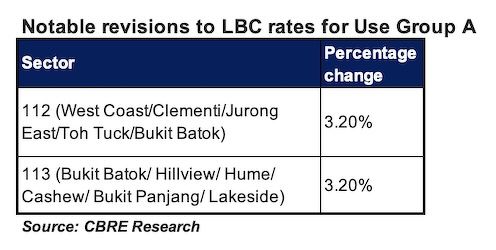

Commercial (A)

The commercial segment registered a marginal average increase of 0.5%, slightly faster than the 0.1% rise in the previous cycle, says CBRE’s Song.

She attributes the revision to several high-value suburban mall transactions in the Outside Central Region (OCR), including The Clementi Mall, which sold for $809 million ($4,132 psf) in December 2025, and Bukit Panjang Plaza, which changed hands for $428 million ($2,602 psf) in January 2026.

Office-dominant areas such as the CBD and Orchard Road saw no change in LBC rates, notes Song.

JLL’s Chua says the limited uplift likely reflects muted underlying land transactions in these sectors, although recent deals — including Reclaims Global’s acquisition of equity interest in Lasidon Holdings, owner of Serangoon Building, and Keppel REIT’s purchase of an additional one-third stake in Marina Bay Financial Centre Tower 3 — may have supported the marginal increase.

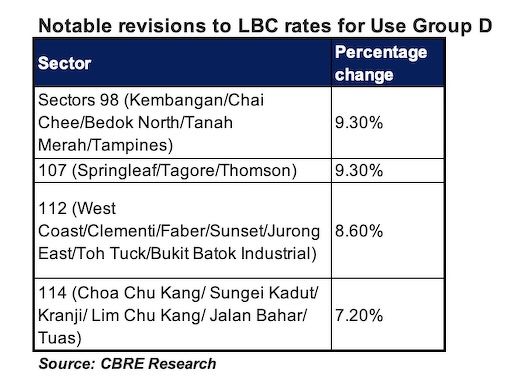

Industrial (D)

Industrial LBC rates rose by an average of 3.2%, up from 1.6% in the previous cycle. “The increase was broad-based, with all 118 sectors recording gains ranging from 1.9% to 9.3%,” says Song.

She attributes this to sustained investor interest driven by attractive yields, alongside portfolio transactions as REITs divested older assets and redeployed capital into yield-accretive investments.

Sectors 98 (Kembangan/Chai Chee/Bedok North/Tanah Merah/Tampines) and 107 (Springleaf/Tagore/Thomson) recorded the largest increases of 9.3%. The uplift was supported by the $14 million sale of Katospring ($109 psf on gross floor area) and the award of a JTC self-storage site at Kaki Bukit Avenue 5 to Extra Space Asia for $31.39 million ($169 psf ppr).

Sector 107 was buoyed by the $351 million acquisition of the freehold site at 680 Upper Thomson Road by a consortium comprising LHN Group, KSH Holdings, Soon Hock Enterprise, Centurion Properties’ controlling shareholders, Petrus Capital and other private investors.

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search