Private wealth is reshaping who's funding real estate; global volatility a 'major test of nerve' for investors

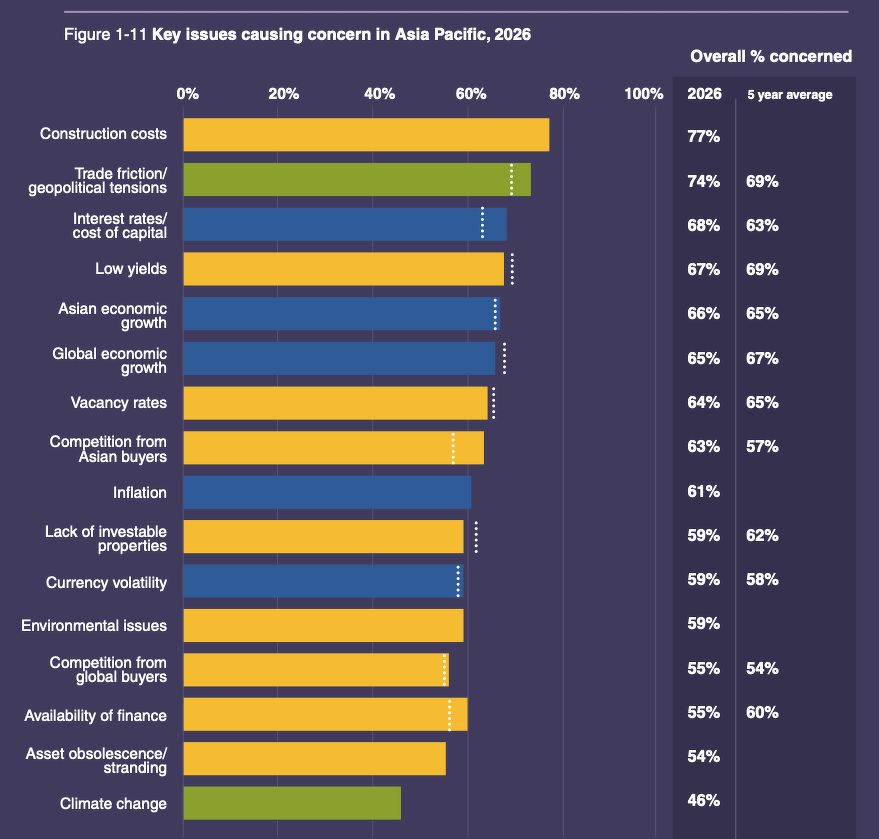

Beijing, China. The most pressing concerns in Apac include rising construction costs, trade friction, geopolitics, interest rates, and low yields. (Photo: Unsplash)

Ask Buddy

The composition of capital flowing into global real estate investments is changing, with the rise of private wealth supplementing — and in some cases displacing — the traditional institutional investor base.

This comes as institutional investors’ target allocations to real estate declined for the first time in 13 years in 2025, which reflects stiff competition for capital from infrastructure and private credit, according to the Emerging Trends in Real Estate Global Outlook 2026 published by PwC and the Urban Land Institute (ULI).

The report, which captures the views of thousands of senior property professionals in Europe, the US and the Asia Pacific (Apac), also found that the prevailing uncertainty from volatile geopolitics and challenging economic conditions continue to post a “major test of nerve” for investors.

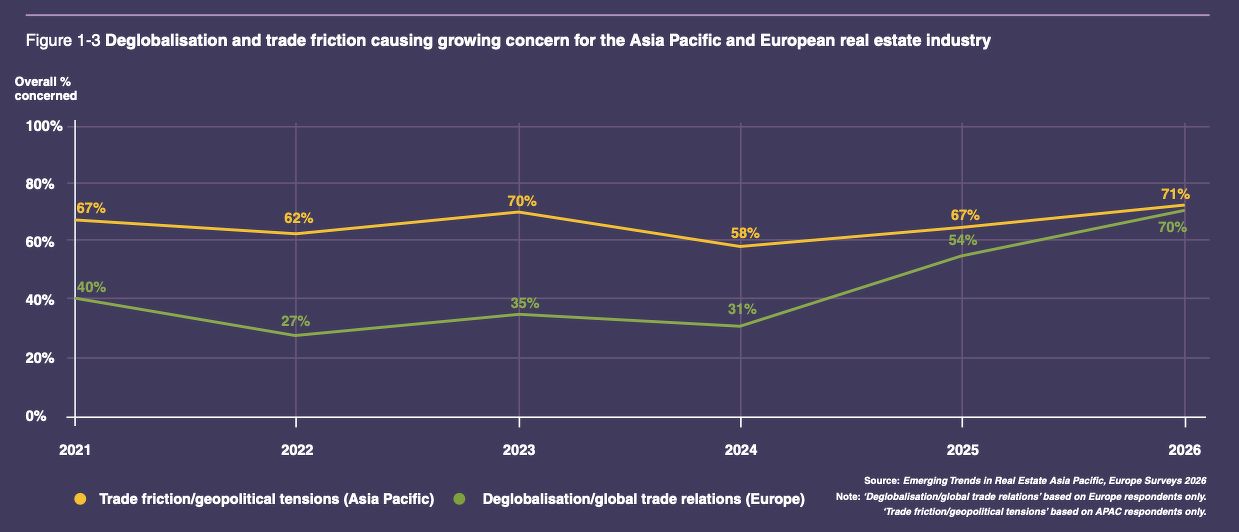

Deglobalisation and trade friction causing growing concern for the Asia Pacific and European real estate industry:

Source: Emerging Trends in Real Estate 2026, Asia Pacific and Europe Surveys.

As for the biggest opportunities for investment and development prospects in the coming year, sectors to watch include data centres, senior housing and assisted living, industrial and logistics, private rented residential, student housing, healthcare, storage facilities, hotels, and affordable housing.

Changing capital currents

The report findings point to a structural shift towards equity that is more agile and driven by private wealth. Institutional capital remains central, but its growth is slowing.

In Apac, expanding family offices, private banks, insurers and newer sovereign wealth funds are driving capital flows into real estate.

While this trend is most pronounced in Apac, Europe and the US are similarly seeing private equity, family offices, high-net-worth individuals and private local investors becoming more prominent sources of funding, acting as a counterbalance to the continued caution of traditional institutions.

Unlike institutions, retail investors typically prefer semi-liquid structures — such as open-ended funds or publicly traded vehicles — which require different deal structures, liquidity planning, and investor communications. The ULI-PwC report notes that retail investors are already demonstrating the ability to adapt structures, strategies and operations to a rapidly evolving global market.

Large institutional investors, such as endowments, pension funds, insurers and sovereign wealth funds, have dominated private real estate through closed-end and open-end fund structures, while retail investors have tended to access exposure via public markets or mutual funds. That balance is shifting today as public markets consolidate and private markets expand.

Taken together, retail investor flows, as well as “household” wealth more generally through the growth of defined contribution pensions, could total hundreds of billions to trillions in potential capital globally, according to the interviews conducted for the report.

“While family offices and high-net-worth individuals may not match private equity in scale, they are increasingly flexible and opportunistic, often co-investing with partners to access development returns without taking full execution risk,” ULI and PwC write.

Institutional investors are generally more active in core assets, while family offices and high-net-worth individuals focus on opportunistic or value-add strategies, and domestic private capital is increasingly active in under-penetrated markets.

The influence of the increased retail capital flows and “household” wealth could have significant ramifications for how the asset class evolves to appeal to this type of capital, the report notes.

Construction costs, geopolitics are main concerns

For 2026, greater stability around inflation and interest rates is supporting many real estate markets. But that has to be balanced against volatile geopolitics and challenging economic conditions amid deglobalisation.

In the Apac region, respondents said their most pressing concerns this year were construction costs (77%), trade friction and geopolitical tensions (74%), and interest rates (68%).

Other key issues they flagged include low yields, regional and global economic growth, vacancy rates, competition from Asian buyers, inflation, and lack of investable properties.

Key issues causing concern in Asia Pacific:

Source: Emerging Trends in Real Estate 2026, Asia Pacific Survey.

Construction costs have risen sharply since the Covid-19 pandemic, and continue to increase in markets where inflation remains an issue.

Interviews for the report indicate signs of caution about rising rates and inflation in Australia and Japan. Some investors are also worried that Japan’s elevated interest rates will affect the underlying real estate values.

When it comes to trade friction and geopolitics, while they remain a key business concern for property professionals, a more sanguine sentiment appears to be growing among investors worldwide.

The impact of deglobalisation in Asia is creating major shifts in relationships between east and west, including China’s engagement in international trade.

There may also be opportunities emerging from deglobalisation. In Asia, there continues to be a focus in investing in diversified supply chains, with the “China plus 1” strategy — a manufacturing hedge against tariffs on China — leading some occupiers to lease additional space in Vietnam, Thailand and the Philippines.

Data centres and other sectors to watch

Once again, data centres dominate the study’s “Sectors to Watch” rankings as one of the biggest opportunities across Europe and North America respondents, while Apac respondents favour them as the most attractive niche property type for the coming year.

That said, the report also points out concerns about an “AI bubble” arising mainly from the vast capital expenditure on data-centre mega campuses in the US, as well as the challenges, which include water and energy consumption and the risk of obsolescence from technology advances.

In Apac, respondents also named industrial and logistics and multifamily residential as their preferred targets, staying loyal to sectors they have backed since 2023.

Interviewees for the Emerging Trends in Real Estate Global Outlook 2026 report included senior professionals from AEW, Barclays Capital, CBRE Investment Management, DLA Piper, Hines, ING, KKR Real Estate, PGIM Real Estate, Savills Investment Management, and more.

For more news and analysis, read our weekly e-paper. Prefer a print copy? Get it delivered to your home every Monday.

Ask Buddy

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Related Articles

Top Articles

Search