Singapore office market: Entering the age of uncertainty

Despite the ongoing conflict in the Middle East, Grade A CBD office rents in Singapore are still expected to rise through 2026 and 2027 (Photo: Albert Chua/The Edge Singapore)

Since early 2025, developments in the socio-economic landscape have increasingly drifted into what would previously have been considered outlier territory. Trade tariffs, corporate margin pressures, the rapid evolution of generative AI — from simple chatbots to autonomous agents — and geopolitical tensions arising from the war in the Middle East have disrupted the status quo.

It appears we are no longer simply managing risk, in which probabilities can be assigned to outcomes, but rather navigating uncertainty marked by incomplete information.

For the Singapore office market, heightened uncertainty, structural shifts in corporate profitability and geopolitical instability are beginning to reshape occupier behaviour and rental trajectories.

Corporate margins — a widening divide

Throughout 2025, many reports predicted that workplaces would experience a more pronounced impact from generative AI in 2026, including concerns that automation could drive headcount reductions. While such concerns are understandable, actual adoption in non-software industries is likely to be slower and more limited than many forecasts suggest.

Claims of significant retrenchments attributed solely to AI may, in some cases, reflect “AI-washing” rather than genuine technological displacement.

More immediate, however, is the pressure on corporate margins.

In 2026, both technology and non-technology firms are expected to remain focused on profitability. A JPMorgan report (August 2025) highlights a stark divergence: smaller US firms (S&P 600) exhibit significantly weaker financial metrics than large-cap peers — lower margins (6.5% vs 13%), higher leverage and reduced pricing power.

This gap is widening. At the 2026 World Economic Forum in Davos, BlackRock CEO Larry Fink warned that AI and macroeconomic conditions are concentrating wealth among a small group of mega-cap firms, and smaller firms — and the broader workforce — risk being left behind.

It is also likely that the strong profitability of the S&P 500 is concentrated within a relatively small set of mega-cap firms, skewing the overall distribution.

What this means for Singapore’s office sector

This divergence is already visible in Singapore’s office market. In 2025, AAA-grade CBD rents rose 2.5% y-o-y, outpacing AA- (1.8%) and A- (1.6%) grade rents. The trend was similar in 2024, though less pronounced.

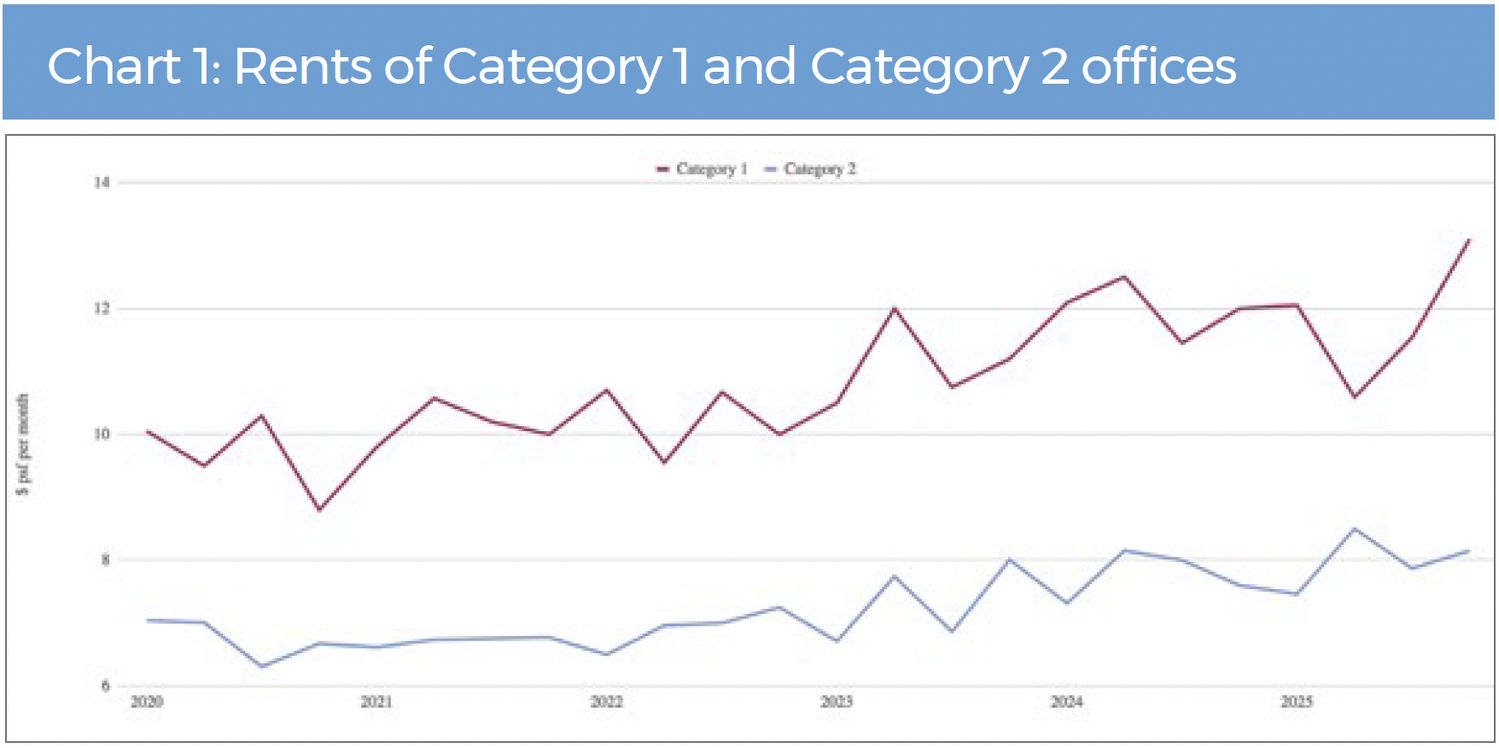

URA data indicates that rents for Category 1 office spaces — broadly aligned with Grade A buildings, encompassing AAA, AA and A sub-grades — have been rising; and Category 2 rents have also increased (refer to Chart 1).

Source: URA, Savills Research & Consultancy

The implication is clear: financial resilience is becoming a key driver of occupier behaviour. Larger firms continue to anchor demand in premium buildings, while smaller firms face growing constraints.

Geopolitics: A new layer of risk

The ongoing US–Israel conflict with Iran introduces another layer of uncertainty. Prolonged disruption to oil and LNG (liquefied natural gas) infrastructure could sustain elevated energy prices well into 2026.

For businesses, this translates into higher operating costs and softer demand. Even if hostilities ease, markets are likely to price in a persistent geopolitical risk premium.

The macro impact is broadly negative, though uneven. Energy producers may benefit, but most corporations will face tighter margins.

Singapore’s Grade A CBD office market, however, is partially cushioned by the relatively limited upcoming supply of new premium office spaces in 2026 and 2027. While smaller multinational firms may feel the strain of rising rents more acutely than larger corporations, these smaller players typically occupy space in Grade B and C buildings.

In contrast, large multinational corporations generally have the financial capacity to absorb higher rental costs.

For frontier start-ups, many are likely to establish lean operational teams and gravitate towards co-working or serviced office spaces within Grade A buildings in the CBD. This allows them to maintain a premium location at a manageable scale.

Nevertheless, even among larger corporations, rising rents do not necessarily translate into larger office footprints. Many firms are still rationalising headcount after the aggressive hiring cycle from late 2020 to early 2022. As a result, consolidation, rather than expansion, may be the dominant trend, with some companies moving operations into higher-quality Grade A buildings — particularly AAA sub-grade buildings.

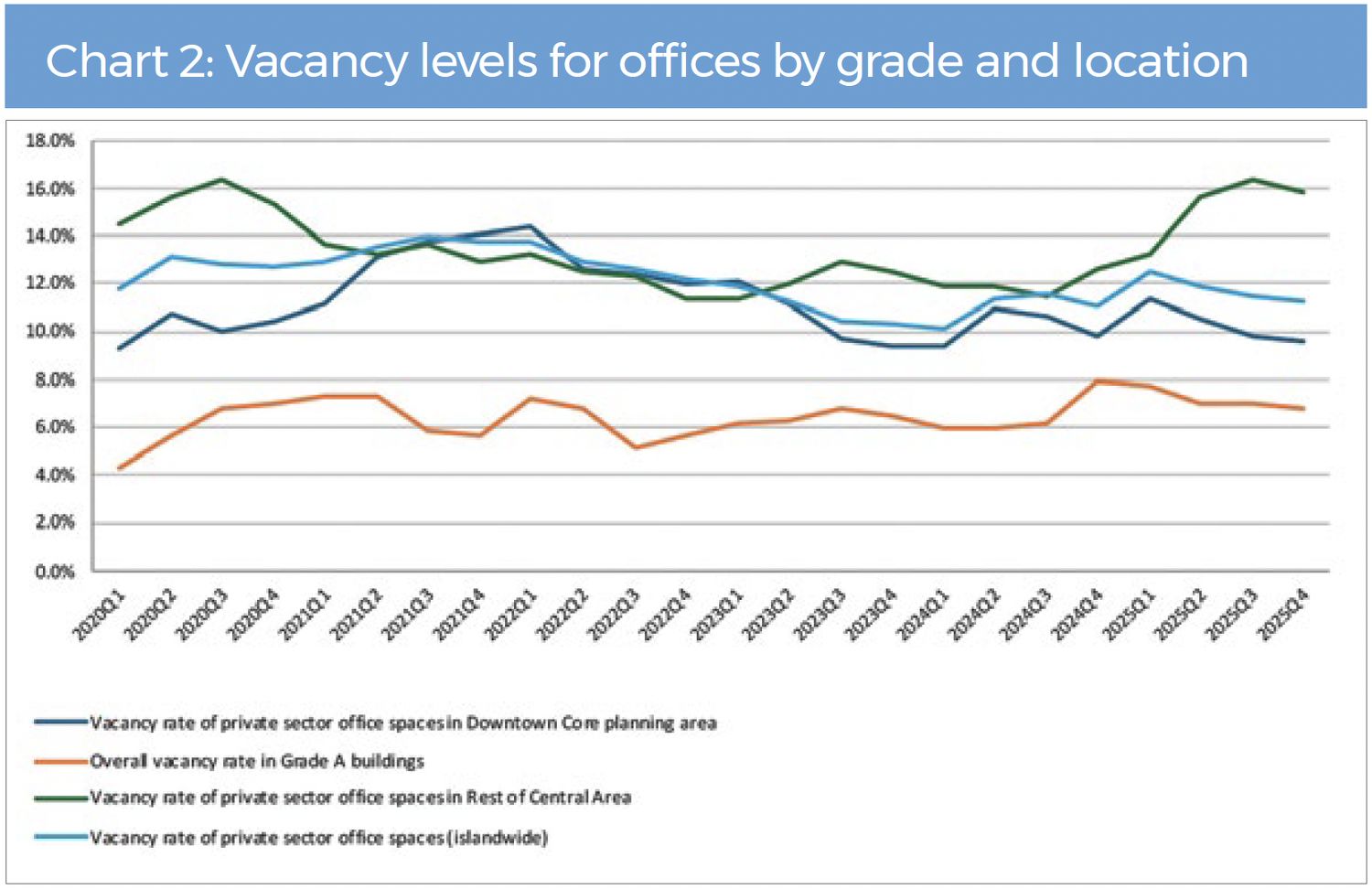

As rents in Grade A buildings rise, upward pressure is likely to extend to lower-grade buildings. However, this may occur alongside growing vacancy in the non-Grade A segment, as tenant preferences continue to shift towards higher-quality assets.

While overall rents may continue to trend upwards, vacancy rates are likely to diverge across building grades, with lower-quality buildings facing a greater risk of elevated vacancies.

Source: Realis, Savills Research & Consultancy

Increasing fragmentation in office market

Despite the ongoing conflict in the Middle East, Grade A CBD office rents in Singapore are still expected to rise through 2026 and 2027.

However, the broader office market is likely to see increasing fragmentation, with the tenant base splitting into more distinct and disconnected sub-segments.

Grade A buildings will continue to attract large, financially resilient corporations and family offices, while non-Grade A buildings may face a more challenging trajectory — either moving towards redevelopment or experiencing rising vacancy levels. This is largely because their tenants tend to be smaller firms operating in industries with tighter margins and weaker bargaining power, often serving companies located in Grade A assets.

Previously, our projections for Grade A office rents in the CBD were a y-o-y growth of around 2%. Given the tightening supply in this submarket — particularly within the AAA segment — we have revised our 2026 rental outlook upwards to growth of 3% to 5%.

Nonetheless, unlike in past years when the environment was comparatively stable, the conflict in the Middle East and geopolitical tensions introduce a meaningful downside risk. Should the situation extend into 2H2026, it could disrupt these projections.

Alan Cheong is the executive director, research & consultancy, at Savills Singapore

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Related Articles

Top Articles

Search