Tight office supply keeps Singapore rents resilient despite slower leasing

The only major development scheduled for completion in 2026 is Shaw Tower (with temporary occupation permit targeted for June/July). It will comprise 450,000 sq ft of premium office space (Photo: Shaw Towers Realty)

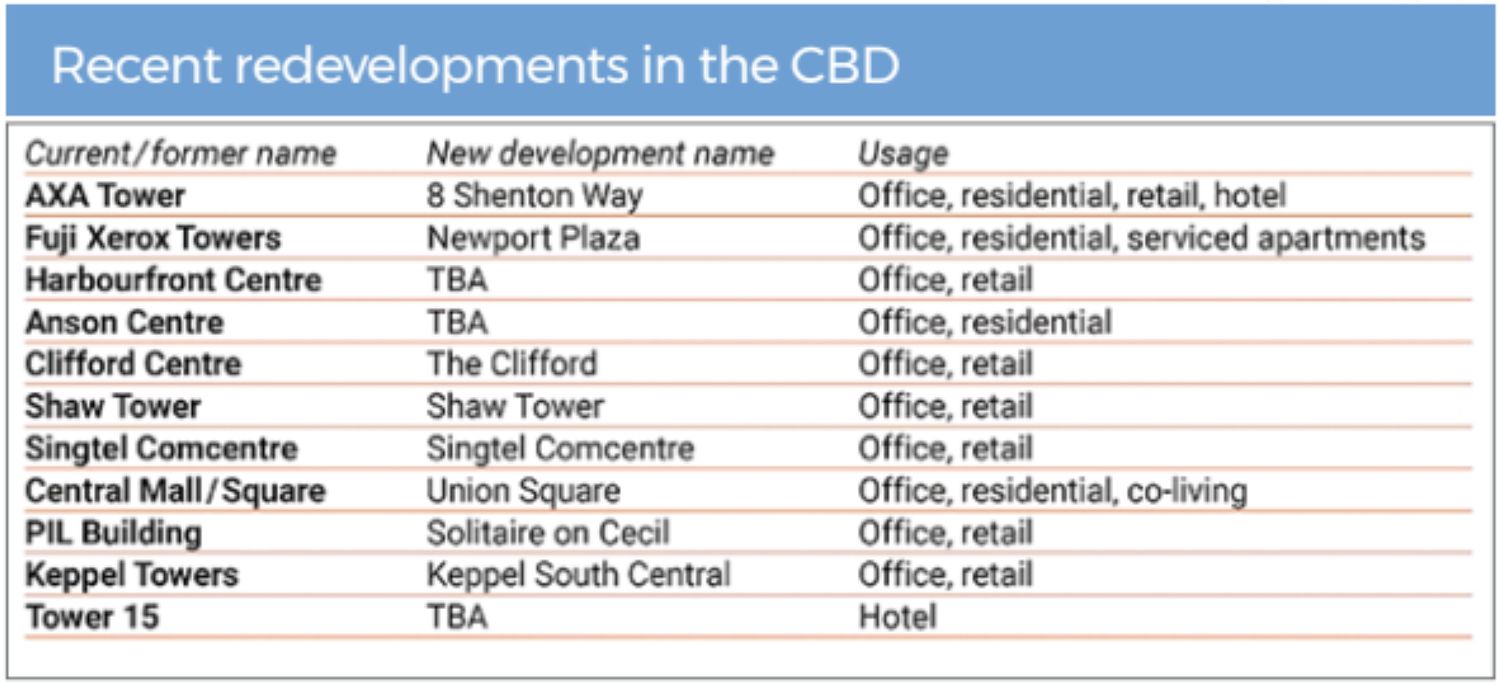

Following the lull over the Lunar New Year period, office leasing activity is expected to regain momentum, with more deals likely to conclude as tenants relocate from HarbourFront Centre and 79 Anson Road, both slated for redevelopment.

79 Anson Road is the latest beneficiary of the CBD Incentive Scheme and the Strategic Development Incentive, both launched by URA in 2019 to encourage the redevelopment of older buildings across the CBD and other strategic areas.

The aim is to reposition the CBD as a round-the-clock mixed-use district — not just a place to work, but one that also supports living and leisure.

Other notable redevelopments include the former Fuji Xerox Towers — now being redeveloped into Newport Plaza and Newport Residences — as well as the former AXA Tower, which will become The Skywaters and Skywaters Residences.

Table: Corporate Locations

Premium buildings continue to draw tenants as the “flight to quality” trend holds. This is reflected in the strong occupancy at IOI Central Boulevard Towers, which is nearly full, and at newly completed Keppel South Central, now a preferred choice for multiple tenants relocating from 79 Anson Road.

Keppel South Central, a 33-storey office tower in Tanjong Pagar, was developed by Keppel and completed last February (Photo: Samuel Isaac Chua/EdgeProp Singapore)

Fitted offices continue to gain ground and are increasingly the default for smaller requirements of up to 3,000 sq ft. In response, more landlords are also offering fitted solutions for existing bare units.

Rents are expected to remain firm, supported by limited supply and steady demand, including from new set-ups and tenants moving out of co-working centres. The Bugis–Beach Road–Suntec micro-market may see increased activity ahead of Shaw Tower’s completion.

Recent relocations

- Financial market: Lumen Capital Investors (CapitaGreen), Amundi Singapore (expanding in UOB Plaza 1)

- Services: New Shipping Agency (Paya Lebar Square), Redington Distribution (Mapletree Business City), Nortrans (OUE Downtown 1), China Telecom (SGX Centre 1), Capcom Singapore (One George Street), Intellipro (60 Anson Road)

- Fast-moving consumer goods: Goshoku Trading (Chinatown Point), Zalora (Centrepoint co-working space)

- Legal services: Lee Bon Leong & Co (UE Square)

- Commodities: Yazaki Global Purchasing (The Gateway East), Ecom Agroindustrial Asia (Anson House), Terrenus Energy (Suntec Tower 1).

Amazon is said to be exiting Asia Square Tower 1, where it has occupied about 100,000 sq ft since 2021. The tech giant’s lease, covering three mid-level floors in the 43-storey building, is said to expire in July.

Shell is expected to be the new tenant of that space if advanced ongoing negotiations culminate in a lease with the landlord of Asia Square Tower 1.

Energy sector — most active

Companies in the energy sector, particularly new entrants to Singapore, have been among the most active recently. It is too early to tell what impact tensions in the Middle East will have on Singapore’s office demand.

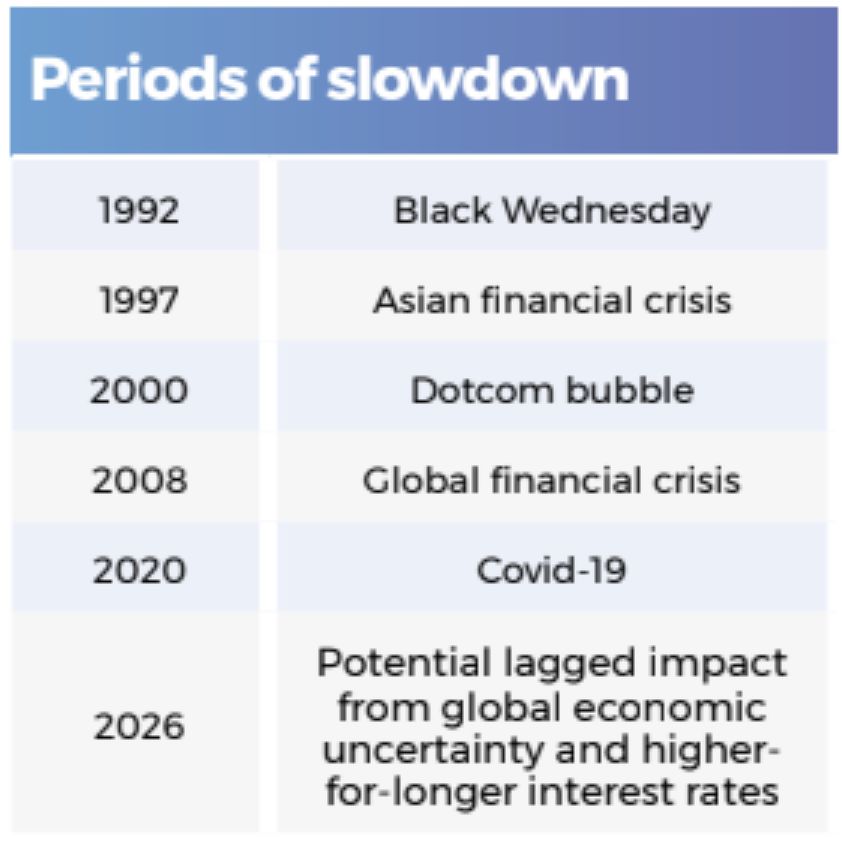

While it is difficult to predict market cycles with certainty, historical disruptions offer useful reference points. Previous periods of market slowdown include:

Table: Corporate Locations

We anticipate that Singapore’s office rental rates could rise by around 3% in 2026, albeit within a much quieter office leasing market.

Many reports quote average (“mean”) rental rates. However, these can be misleading, as an average monthly rate of $11.50 psf may reflect actual transactions ranging from $9 to $14 psf.

A more accurate assessment is to look at the “mode” rate, which represents the rental rate that appears most frequently in the market.

Currently, the mode rental rate for top Grade A buildings remains around $14 psf per month. Upper mid-range office space typically records mode rates of approximately $11.50 psf, while lower mid-range space is generally between $8 and $9 psf.

The resilience in rents reflects a structural supply constraint that continues to underpin Singapore’s office market. Some may argue that this could make Singapore less competitive. However, Singapore remains an important market in so many other respects that rising rental rates are unavoidable for most businesses.

New supply

The supply situation in Singapore is the opposite to that in other major European and US financial centres, and even other APAC financial hubs such as Hong Kong and Sydney. These markets are currently experiencing a significant oversupply of office space, leading to a slump in rents.

In contrast, supply in Singapore is the tightest it has been for years, which is having a knock-on effect on rental rates.

The only major development scheduled for completion in 2026 is Shaw Tower (with a temporary occupation permit targeted for June or July). It will comprise 450,000 sq ft of premium office space.

To date, major pre-commitments announced at Shaw Tower include R&D-driven pharmaceutical firm Sanofi and e-payment financial tech firm Adyen. Business centre operator The Great Room by Industrious is understood to be leasing around 36,000 sq ft.

The latest premium Grade A office tower to be introduced in Raffles Place — The Clifford at Raffles Place (former Clifford Centre) — will deliver 405,000 sq ft of net lettable area comprising office space, retail and lifestyle amenities.

The latest premium Grade A office tower to be introduced in Raffles Place, The Clifford (former Clifford Centre) at Raffles Place will deliver 405,000 sq ft of net lettable area (Photo: Singapore Land Group)

The 220m tower will provide 360,000 sq ft of premium Grade A office space across 21 floors, complemented by 45,000 sq ft of retail and F&B offerings.

Against this backdrop of limited new supply, investor interest in well-located office assets has also begun to re-emerge, particularly as expectations of lower interest rates improve the outlook for commercial property transactions.

On the market

Altallo Asset Management has entered into a put-and-call option agreement to acquire an office building at 158 Cecil Street for $175 million.

The price works out to $1,541 psf for the 14-storey property’s net lettable area of about 113,540 sq ft. The building is on a site with a 99-year leasehold tenure from January 1982, which leaves a balance of about 55 years.

The owners of One Raffles Place — which sits above and is directly linked to Raffles Place MRT Station — have reportedly appointed CBRE and JLL as joint marketing agents to find a buyer.

One Raffles Place has a 220m, 62-storey office tower, an adjacent 38-storey office block and a six-storey retail podium with a total of 860,000 sq ft of net lettable area. The building has been put up for sale by the owners, UOB Group and OUE Reit, at an indicative price of $2.4 billion.

Emerging market trends

Several trends have emerged in the market and are likely to continue.

1. Lack of office space for large-space users

Large-space users will find it increasingly difficult to source suitable space and may have to rely on stop-gap solutions, such as using “swing space” or temporary space, until a new wave of supply comes on stream in 2028.

The redevelopment of Comcentre on Exeter Road in the Orchard Road area is targeted for completion in 2028. It will have twin 20-storey office blocks with about 1.2 million sq ft of space (Photo: Lendlease)

2. Landlord fitted-out space

There has been some resistance to rising rents and, as a result, demand has softened. Consequently, more landlords are becoming proactive in responding to increased demand for fitted-out space.

Many landlords are now offering fully fitted units on a “plug-and-play” or “plug-in-and-go” basis. These options typically involve a base gross rental, plus approximately $2 psf to amortise the cost of the fit-out works.

3. Repositioning of business centre and serviced office space

The repositioning of business centre and serviced office operators continues. Some operators are scaling down. They include Ucommune at Bugis Junction and Prudential Tower. WeWork is giving up space in Manulife Tower and UE Square, O2 at Collyer Quay Centre, and CityHub at 20 Collyer Quay.

Other operators, however, continue to expand. Flexible office space provider Arcc Spaces, is leasing three floors in the Bank of Singapore Centre, JustCo is leasing several floors at 108 Robinson Road, The Executive Centre is expanding in Ocean Financial Centre, and The Work Project in Asia Square Tower 2. The Great Room announced that it will open its 10th location in Singapore — at Keppel South Central in June — in addition to its two upcoming locations at Shaw Tower and Stamford Place (former Stamford Court).

The Drawing Room at the upcoming Great Room in Keppel South Central, marks the brand’s 10th presence in Singapore, in addition to upcoming locations at the new Shaw Tower and Stamford Place (former Stamford Court) (Photo: Siren Design Studio)

Taken together, tight supply, selective tenant expansion and the continued flight to quality are likely to keep Singapore’s office market resilient. While leasing activity may remain measured amid global economic uncertainty, the lack of new supply in the near term should continue to underpin rents — reinforcing Singapore’s position as one of the most stable office markets in the region.

Douglas Dunkerley is the managing director of office leasing specialists Corporate Locations

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search