Australia housing affordability set to worsen for new homebuyers in 2026: Moody's

Sydney is the least affordable housing market in Australia, according to Moody's housing affordability measure (Picture: Jesper van der Pol/Unsplash)

Housing affordability in Australia may decline throughout 2026, amid rising interest rates and high housing prices, according to an April research report by Moody’s Ratings.

The credit ratings and research agency measures housing affordability as the share of average monthly household disposable income homebuyers need to meet monthly home loan repayments on a typical new mortgage.

As of March, housing affordability in Australia stood at 29.6%, higher than the 28.6% recorded in December 2025 and the 29.1% recorded a year earlier, in March 2025.

Sydney was by far the least affordable city for housing, with monthly home loan repayments taking up 40.4% of household disposable income. Brisbane (37.1%) was second, followed by Adelaide (28%), Perth (25.4%), Melbourne (23.9%), Hobart (23.3%) and Darwin (20.9%).

The deterioration of housing affordability projected for 2026 marks a reversal from improvements charted in 2025, says Moody’s. This comes as the Reserve Bank of Australia (RBA), the country’s central bank, tightens interest rates.

Housing affordability measure, by city

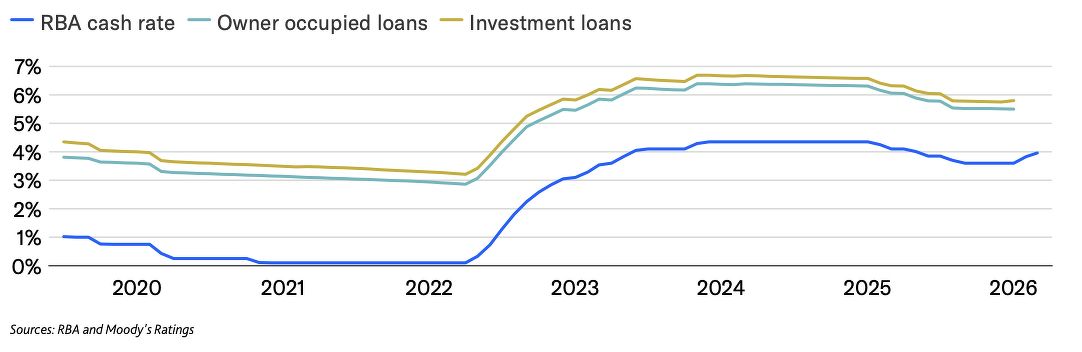

After lowering interest rates throughout 2025, the RBA increased its cash rate by 0.25 percentage points in both February and March to counter inflation. The benchmark interest rate currently stands at 4.1%, with the next central bank meeting scheduled for early May.

Moody’s expects the RBA to continue tightening rates. “Further rate increases are likely this year, with the RBA signalling that it may need to continue raising the cash rate to return inflation to the central bank’s target range amid a global energy crisis that is increasing the cost of living,” its report states.

The more conservative monetary policy has trickled into mortgage rates, with Moody’s observing higher lending rates since the start of the year.

Monthly average RBA cash rate and lending rates for new loans funded

Demand-supply factors to keep house prices high

While the increase in financing costs, coupled with higher costs of living, is expected to dampen the housing market to an extent, Moody’s predicts housing prices in Australia will remain elevated in 2026, underpinned by both demand and supply factors.

Demand for Australian housing remains supported by steady population growth, backed by inbound migration. The country’s population, which stood at 27.6 million as of June 30, 2025, is forecasted to grow by roughly 300,000 per year, according to the Australian government’s 2025 Population Statement.

At the same time, government initiatives to promote home ownership have propelled housing purchases. In October 2025, the government launched the 5% Deposit Scheme, which expands on a previous scheme, launched in 2020, that allows eligible buyers to purchase their first home with a deposit of as low as 5%.

Under the newer 5% Deposit Scheme, the eligibility criteria were expanded, with the removal of previous income caps and higher price limits for homes being purchased. Buyers will also be able to buy their home without having to purchase lenders mortgage insurance, thus reducing upfront costs.

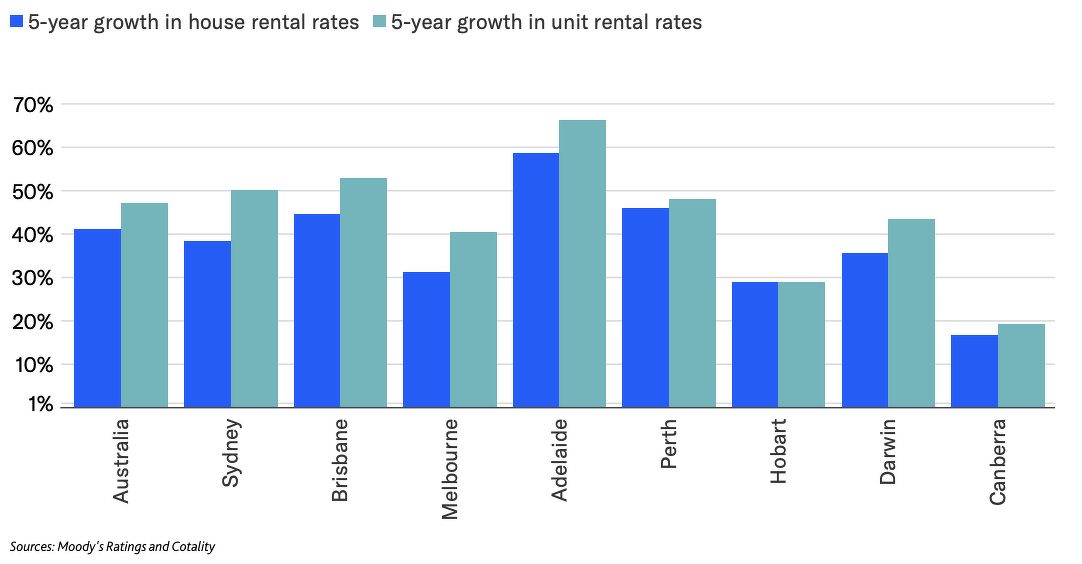

House rental rates and unit rental rates by capital cities

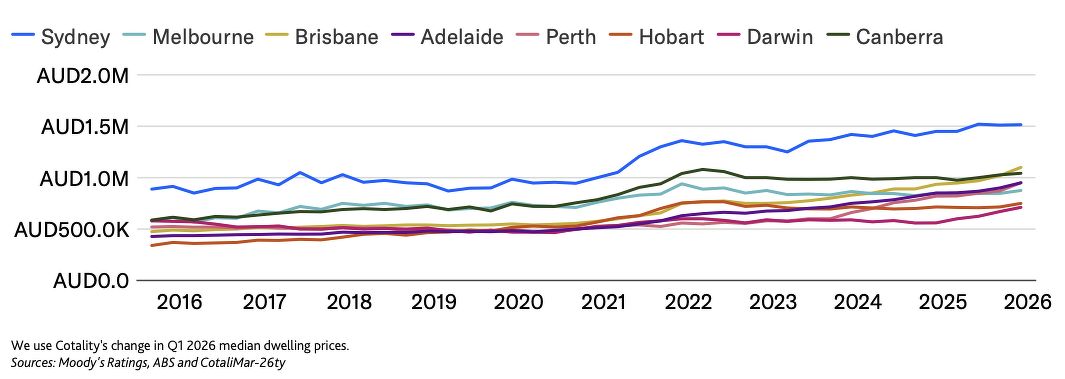

Beyond first homebuyers, the housing market is also garnering demand from investors drawn to its strong rental growth over the last five years. Since 2021, Australian housing rental rates have surged by around 40% amid a lack of supply, with vacancy rates falling to less than 2% at the end of 2025.

Moody’s notes that new housing supply remains low compared to current population growth levels, as high construction costs inhibit new housing builds. Combined with resilient demand, the tight supply is expected to keep housing prices elevated.

Median dwelling prices, by city

Different scenarios

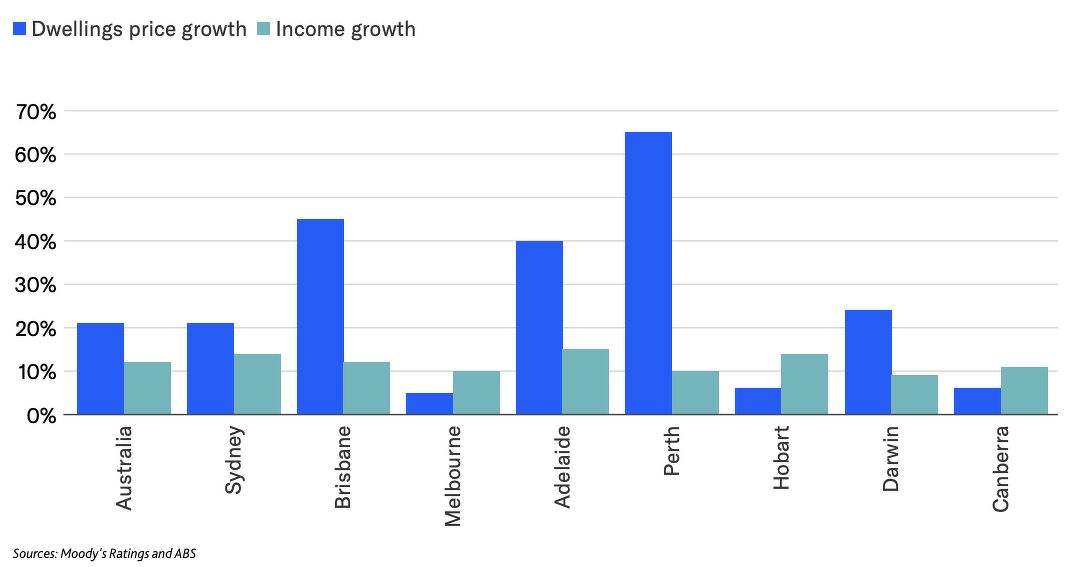

While household income has risen in Australia over the past year, Moody’s does not expect this to improve housing affordability, as inflation has eroded wage gains in real terms. “Housing price growth exceeded income growth on average in Australia and in most major cities in the two and a half years to December 2025,” the report adds.

Housing price and income growth from March 2023 to December 2025

As a result, any changes in housing affordability this year will largely depend on the RBA’s interest rate decisions, along with movements in house prices.

For market observers, a further increase in interest rates is on the cards in the near term. Most economists polled by The Australian Financial Review expect the cash rate to be lifted to 4.35% in May, the newspaper reported on April 7, with some anticipating further hikes that could see the rate hit 4.6% by the year-end.

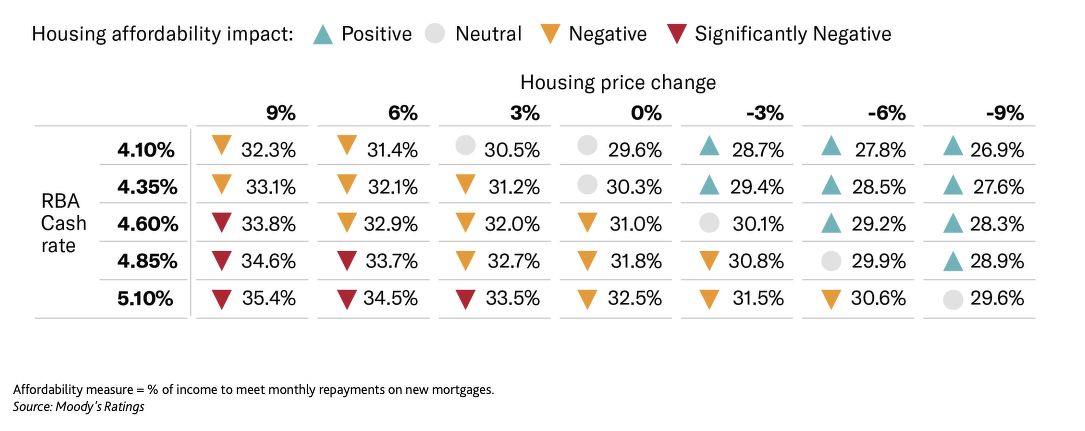

Moody’s model indicates that if the RBA raises the cash rate to 4.35%, assuming housing prices do not change, housing affordability will decline, with monthly mortgage payments making up 30.3% of income. If the rate rises to 4.6%, the housing affordability measure increases to 31%, indicating worsening affordability.

Housing affordability measure under RBA cas rate and housing price scenarios

In addition, any increase in house prices will exacerbate the decline in housing affordability. Moody’s model shows that at a cash rate of 4.35%, the housing affordability measure rises to 31.2% if housing prices go up by 3%, or 32.1% if they increase by 6%.

At a cash rate of 4.6%, a housing price gain of 3% will see the housing affordability measure hit 32%, or 32.9% if housing prices rise 6%.

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search