The time has come for opportunistic buyers to scavenge for bargains

One of the most memorable quotes in investing is “Be fearful when others are greedy and greedy when others are fearful”. The person who said this is none other than Warren Buffett, arguably the most prominent investor of our time, who amassed most of his fortune purely from stock-picking and buying undervalued companies.

Can the same principle be applied to the Singapore property market today? It is yesterday’s news that buyers are adopting a wait-and see attitude out of fear or caution that prices might slip further. Their concerns are not unfounded, given the multiple property curbs, rising interest rates, softening rental market and news of a potential supply glut afflicting the market. It would be irrational to dismiss this as “herd mentality”, but too much repetition can cloud investors’ judgement. As the market continues to chart a downward trajectory, we believe the hunting season has begun for opportunistic buyers scavenging for bargains in the housing segment.

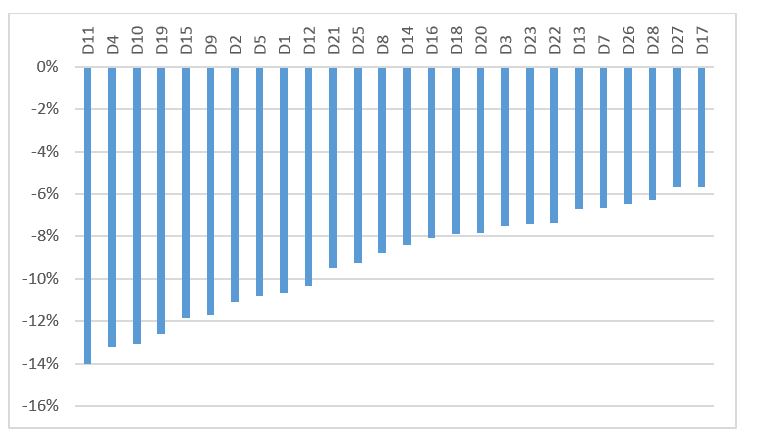

The high-end and city-fringe housing segment, for example, could be investors’ next bet. A survey of listings on The Edge Property showed that District 11 (Novena and Thomson area) topped the charts for potential discounts offered (see Figure 1).Around 19% of listings in District 11 were found to be below the median transacted price over the past six months. Of these so-called undervalued listings, the discount was 14% below the median transacted price.

Figure 1: Average discount* among undervalued listings ranked by district

* Median asking price versus median transacted price in the district adjusted for size

Source: URA, The Edge Property

With the exception of District 19, which stretches from Serangoon to Punggol, the top 10 districts in terms of discounts offered were in prime and city-fringe locations. This came as no surprise, given that prices of non-landed homes in the Core Central Region (CCR) and Rest of Central Region (RCR) have fallen since their last peaks by around 7%. On the other hand, prices in the Outside Central Region (OCR) have only declined by 4% since their last peak.

The discounts should not be taken at face value, but rather as a litmus test across locations. The study categorised the asking and past transacted prices of non-landed homes into various size bands before computing the discount rate in order to minimise distortions where only larger units would be found to be undervalued.

If a hefty price tag is a deterrent, city-fringe homes would be a more palatable choice. According to caveats lodged with the Urban Redevelopment Authority (URA) between January and April this year, the median price for non-landed homes in the RCR was $1.2 million, compared with $2.2 million in the CCR. Separately, the mass-market segment offers bite-sized opportunities. No surprise here, the discount magnitude among its undervalued listings was smaller than its pricier cousins.

A study on asking prices might raise contention, but the message is simple and clear: It is time for undecided buyers to start doing their homework and they might uncover trophy deals.

Those still unconvinced and hoping for prices to nosedive might be in for a disappointment. There are many such people apparently, which explains the gridlock between buyers and sellers and hence, the low sales volume. The following is why a nosedive in prices may remain a pipe dream for investors. Preliminary data from the Manpower Ministry showed that the unemployment rate continued to trend down to 1.8% as at March 2015, lower than the 2.1% seen in the boom year of 2007. The Singapore GDP, meanwhile, is forecast to expand between 2% and 4% this year. Historically, market crashes were only associated with economic recessions, in which peak-to-trough prices lost altitude at a compounded rate of more than 5% a quarter. The current compounded rate of decline at 0.9% a quarter seems to pale in comparison.

Tender prices for private housing sites sold under the Government Land Sales (GLS) programme have also held firm, with the exception of a few select locations where there was perceived oversupply. Even these were part of prudent strategies to hedge against a hike in construction costs and allow developers flexibility in pricing their projects. Separately, top bids for private housing sites sold this year have generally exceeded market expectation. The sites were highly contested, drawing nine to 16 bids each. Having addressed the undersupply situation post-global financial crisis, the government continued to moderate housing supply offered under the GLS programme and the number of homes offered under the Confirmed List has dwindled from 4,600 units in 1H2014 to 3,020 units in 1H2015.

More than anything, the current downtrend in prices is artificially induced by the total debt servicing ratio framework (TDSR) and additional buyer’s stamp duty. Hence, a potential opportunity in the current market is to shortlist properties with discounts that may offset the ABSD.

We attempted to pick some resale projects with undervalued listings that offer at least a 5% discount to their median transacted price for the past six months. This does not mean that prices in these projects have fallen dramatically but just that there might be value deals that await those who search diligently. The size was set at 1,200 sq ft and below. Three projects emerged from the search — Dover Parkview, D’Leedon and Melville Park. For bigger units of more than 1,200 sq ft, more projects surfaced — The Interlace, Costa Del Sol, D’Leedon, Goodwood Residence, Changi Rise Condominium, Urban Resort Condominium and Kovan Melody. The list would be longer if not for the search criterion, which requires at least five transactions over the past six months within the size category. Many projects, as a result, were removed from the radar.

The current scenario of low transaction volume versus stubbornly high prices defies the basic logic of supply and demand. To put it simply, buyers are expecting ridiculously low prices, while sellers are not willing to budge. In other words, the market is in a state of disequilibrium. Until sellers’ holding power is shaken by unforeseen external shocks, the odds are against buyers winning the tug of war.

Meanwhile, the rental market would act as a cushion for owners against rising interest rates and foreclosures. This brings us to another point — the loss in rental yield for investors who continue waiting on the sidelines. Based on URA data, gross rental yields averaged 3.2% in 1Q2015 and were relatively uniform across districts, with a standard deviation of 0.4 percentage point. A more conservative estimate based on the 25th percentile rents puts the rental yield at 2.8%, with a standard deviation across districts of 0.3 percentage point.

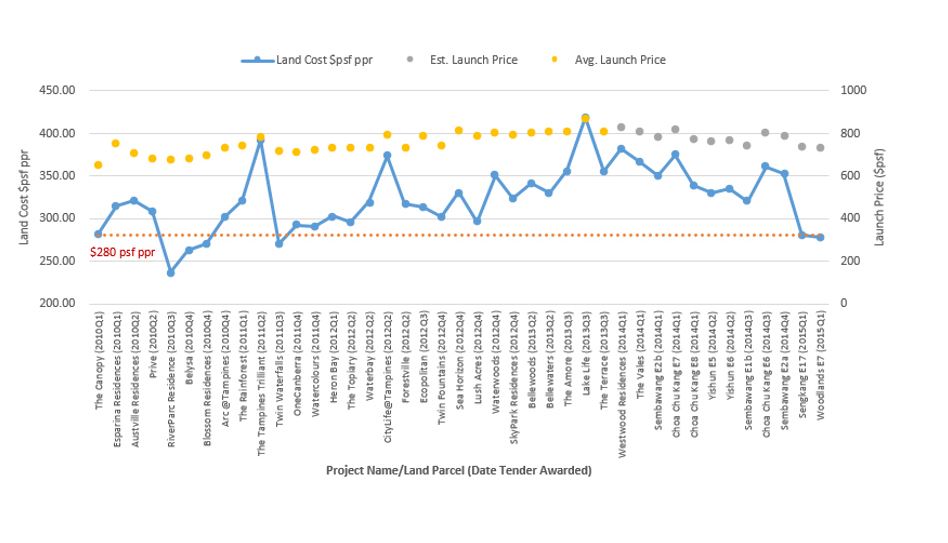

While tender prices for private housing sites have held firm, executive condominium sites saw prices buckling. Prospective buyers might wish to watch out for this segment. In February, two EC sites in Sengkang and Woodlands were sold for about $280 psf per plot ratio, a price unheard of since 3Q2011. Based on the tender price, EC prices in Sengkang and Woodlands may witness a price correction of 5% to 8% next year, from around $790 psf to between$730 and 750 psf (see Figure 2). In addition, eight EC projects are expected to be launched this year. Developers of these projects that have submitted their tender prices, based on previous market conditions, could adjust their profit margins to price their projects competitively.

Figure 2: Land cost of executive condominium sites and their average launch price

Source: URA, The Edge Property

While prices may continue to head south, undecided buyers should reflect on whether the prospect is worth the wait. At the rate non-landed prices are falling at a compounded average of 0.9% a quarter, the opportunity costs of waiting include a loss in interest savings amid a rising Sibor (Singapore interbank offered rate) and rental income foregone. Revisiting those listings, there are value deals waiting to be uncovered, where discounts offered surpass the magnitude market prices have fallen.

With prices having come off for more than a year now, the question of whether it is the right time to buy has become less relevant. Buyers should instead evaluate the property’s location attributes, their investment needs and affordability threshold should the market take a turn for the worse. Ultimately, the most important question should be whether we can sleep with those numbers.

This article appeared in The Edge Property Pullout of Issue 677 (May 18) of The Edge Singapore.

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search