How smart homeowners are rethinking their mortgage strategy as rates fall

The most successful homeowners are not those who simply hunt for the lowest rate but those who understand how to structure their finances around the market cycle

After a prolonged period of elevated borrowing costs, global central banks led by the US Federal Reserve have begun cutting rates to support a cooling economy.

In Singapore, this easing trend has filtered through the local market: fixed home-loan packages that hovered around 2.80% in mid-2024 have steadily fallen to about 1.55% today. Meanwhile, the benchmark three-month compounded Singapore overnight rate average (3M Sora), which stood at 3.03% earlier this year, has dropped to roughly 1.33%.

For property owners, this isn’t just cause for celebration — it’s a signal. A reminder that interest-rate cycles move in waves, and that true financial resilience lies not in reacting to the tide, but in learning to ride it. Because beyond chasing a lower rate, savvy homeowners are now optimising their mortgages through liquidity planning, Central Provident Fund (CPF) strategy and even strategic equity deployment.

Where interest rates are headed

To understand why this moment matters, it helps to see where we’ve come from.

Throughout 2023 and early 2024, mortgage rates climbed sharply as central banks fought stubborn inflation. Many homeowners locked in fixed packages with rates ranging from 2.8% to 3.20%, while floating rates pegged to Sora moved above 3%.

As inflation eased and global growth softened, the Fed pivoted and started cutting rates in mid-2024 and again in September.

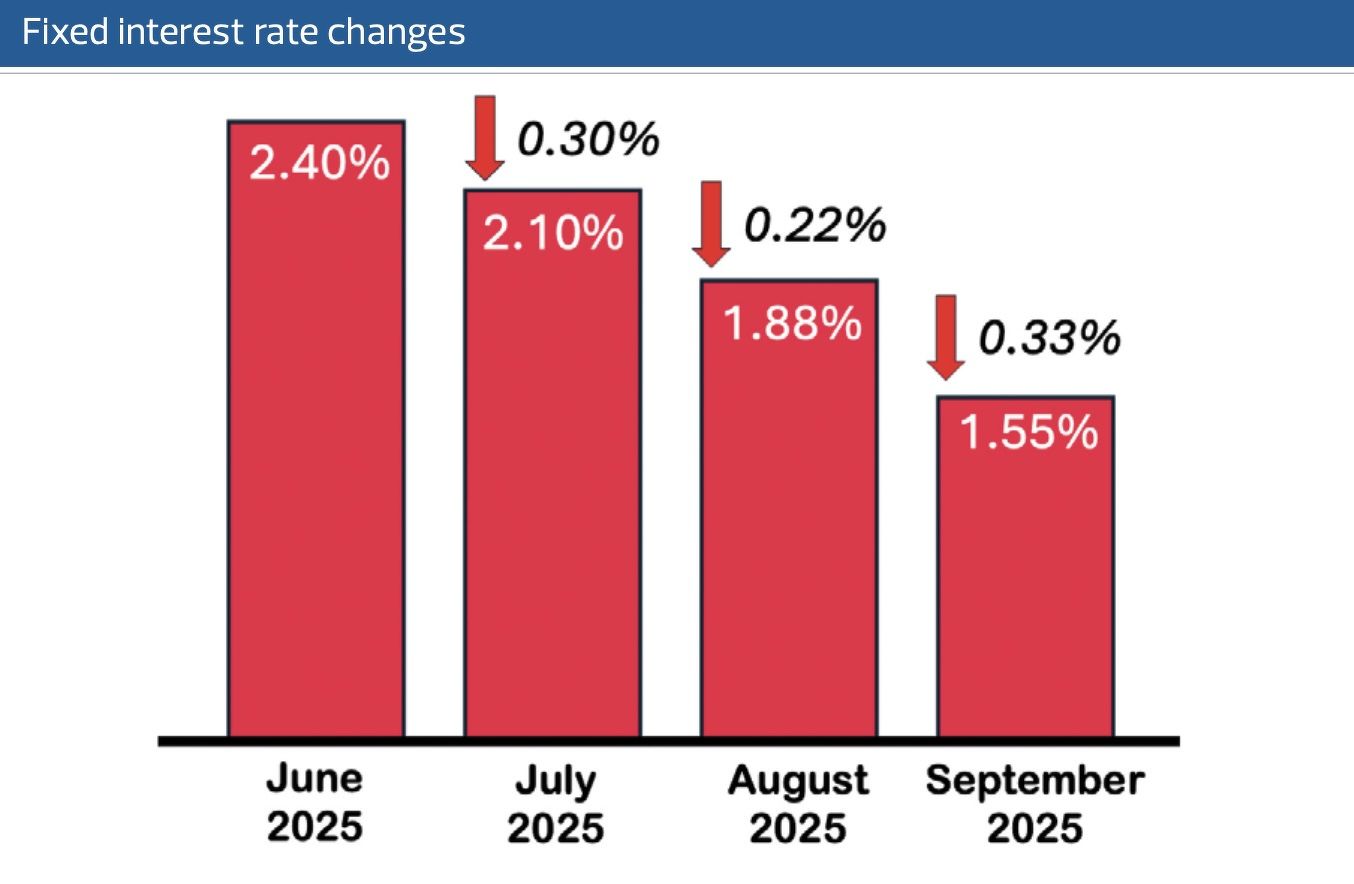

Since then, fixed mortgage packages have fallen in sequence:

June 2024: 2.40% → July: 2.10% → August: 1.88% → September: 1.55%.

In the same period, the three-month Sora eased from 3.03% in January 2025 to 1.36% by September, reflecting a broader moderation in monetary conditions.

What this means for homeowners is straightforward: the cost of borrowing is falling. But what’s less obvious is that opportunities in a declining-rate environment aren’t confined to cheaper loans. They extend into how you structure liquidity, manage CPF, and even reallocate equity, all of which can improve long-term financial flexibility.

In a market that’s shifting quietly but steadily, the smartest homeowners aren’t just celebrating lower rates; they’re re-engineering how their money works for them.

Source: Redbrick Mortgage Advisory

Liquidity is the new leverage

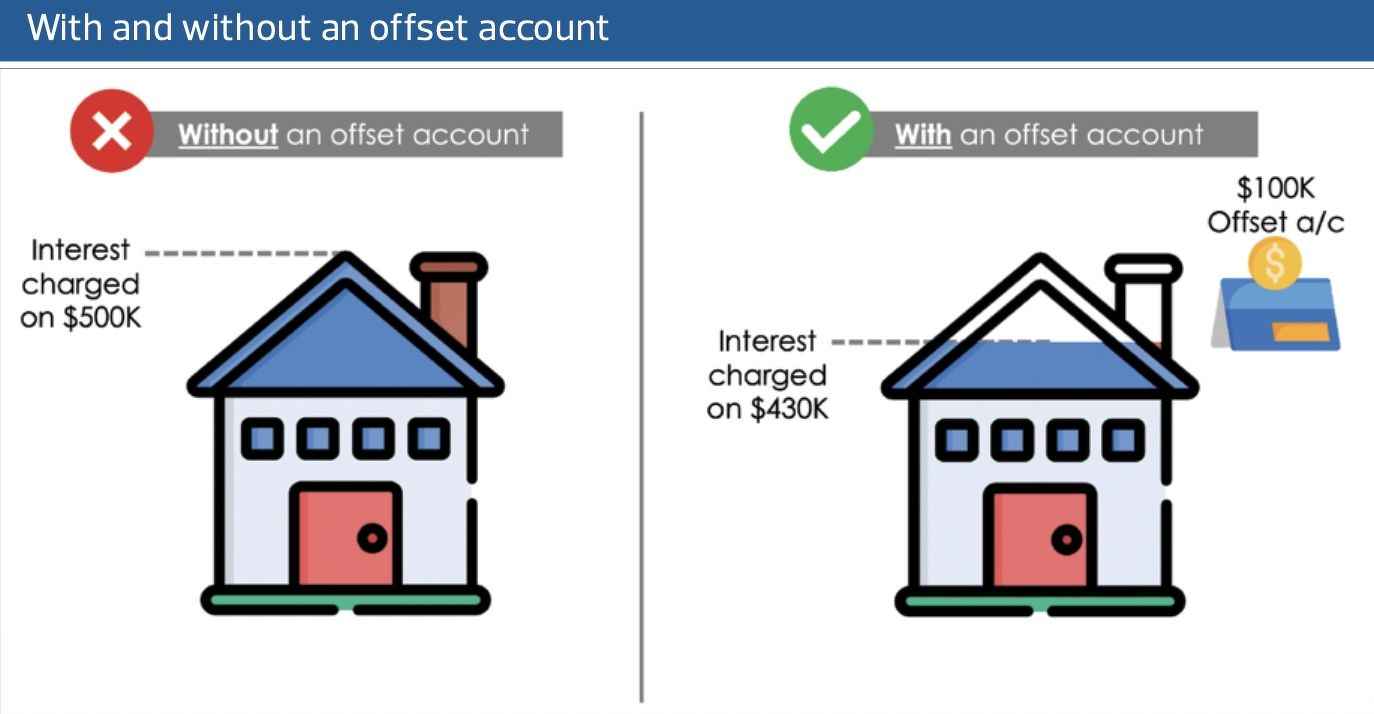

One of the most overlooked tools in the mortgage landscape is the interest-offset account, offered by a few offshore banks in Singapore.

Here’s how it works:

When you park cash in the linked offset account, that balance effectively reduces the portion of your loan on which interest is charged. For example, if you have a $500,000 mortgage and $100,000 parked in your offset account, you’re effectively paying interest only on $430,000.

Seventy per cent of your $100,000 “offsets” the interest, like earning a risk-free return equal to your mortgage rate. Meanwhile, it keeps your money fully liquid. So, you get access to your money while leveraging on that same cash to reduce your effective mortgage interest rate.

Instead of locking funds in fixed deposits or volatile investments, homeowners can keep liquidity ready for emergencies or opportunities without sacrificing returns.

It’s an elegant way to hedge uncertainty while still optimising your cost of debt. But liquidity isn’t the only lever homeowners can pull. In fact, for many, their biggest opportunity may be sitting right in their CPF Ordinary Account.

The CPF refund advantage

For decades, CPF Ordinary Account (OA) funds have been the default source for mortgage repayments. It’s convenient, automatic, and on the surface, logical. But few realise that this convenience comes with an invisible cost. Every dollar you use from CPF OA to pay for your property accrues 2.5% “accrued interest”, money you must eventually refund to CPF OA when you sell. Think of it as a silent liability you owe yourself.

Here’s where the math gets interesting: If you’ve used $200,000 from CPF OA, that sum accrues $5,000 of interest each year at 2.5%. With mortgage rates now hovering around 1.55%, homeowners who have spare cash might consider refunding their CPF.

Why? By refunding, you’re restoring your OA balance, which earns 2.5% virtually guaranteed, while simultaneously reducing a loan that costs less. In effect, you’re capturing an arbitrage of almost 1% per year, risk-free.

This strategy isn’t for everyone, of course. It requires liquidity and discipline. But for those with cash sitting idle in savings accounts yielding below 1%, it’s one of the few “sure-win” moves available today.

For homeowners who don’t have spare cash but do have property equity, fret not, for there’s another way to reposition capital.

Source: Redbrick Mortgage Advisory

Releasing equity

If you own a private property whose value has appreciated, you may be able to extract part of that equity through an equity term loan, a facility pegged to attractive home-loan rates. Used wisely, this can be a powerful financial tool.

Some homeowners draw an equity term loan at around 1.6% to refund CPF (as described above). Others use it to diversify into assets that yield more, such as dividend-paying instruments or insurance endowments.

For instance, a homeowner who releases $300,000 of equity at 1.6% might redeploy part of it into investments yielding 3% to 4%, while retaining liquidity. The key is not to over-leverage, but to reallocate capital intelligently, turning dormant equity into working capital that compounds.

At a time when interest rates are low but uncertainty lingers, such flexibility can spell the difference between being trapped by a mortgage and mastering it.

Breaking the fixed-rate inertia

Lastly, many homeowners who refinanced one to two years ago are now “locked in” at higher fixed rates, often between 2.8% and 3%, and feel helpless as newer packages plunge below 1.6%. However, being locked in doesn’t mean being stuck.

The math can still work in your favour, even if it means breaking the lock-in period and incurring a 1.5% penalty for refinancing.

Let’s illustrate: On a $1 million loan locked at a three-year fixed rate at 2.80% in 2024, a homeowner pays approximately $28,000 per year in interest. There are two more years to go before the homeowner comes out of the lock-in period.

Refinancing to a fixed interest rate of 1.55% offered today would reduce the interest payments to approximately $15,500, thereby saving $12,500 per year. Over two years, that’s $25,000 saved. After deducting the $15,000 penalty (1.5% of $1 million), the homeowner still gains $10,000 net over two years, while regaining flexibility and access to future rate cycles.

Of course, this requires careful calculation, taking into account remaining lock-in periods, legal fees, and potential claw-back periods. But the point stands: the cost of inaction can quietly exceed the cost of change.

The bigger picture

Ultimately, the most successful homeowners are not those who hunt for the lowest rate but those who understand how to structure their finances around the market cycle.

When rates were rising, the goal was stability. Today, as rates fall, the advantage shifts to flexibility. Homeowners who refinance strategically can free up cash flow, while those who use interest-offset or equity-release facilities can build a liquidity buffer for the next phase of the cycle.

And as CPF, savings, and property equity intertwine, the real question isn’t “Which bank gives me 0.1% less?” but “How do I align my cash, CPF, and equity to work in sync?” That is where your portfolio evolves from transactional to transformational.

The environment we’re in today is a rare window. Whether you’re refinancing to capture lower rates, refunding CPF to earn more, or using equity to unlock new possibilities, the ultimate goal remains the same: to build a structure that supports your life, not just your loan.

Clive Chng is the associate director of Redbrick Mortgage Advisory

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search