More than enough space in all segments

Singapore may be a very small city state that is land-locked, but we have lots and lots of empty space. And it seems that the vacancies are rising in every property segment since the recovery from the Global Financial Crisis in 2010. Is the Singapore market oversupplied with real estate? Or has demand fallen far short of expectations such that vacancies accumulate as each additional building gets completed?

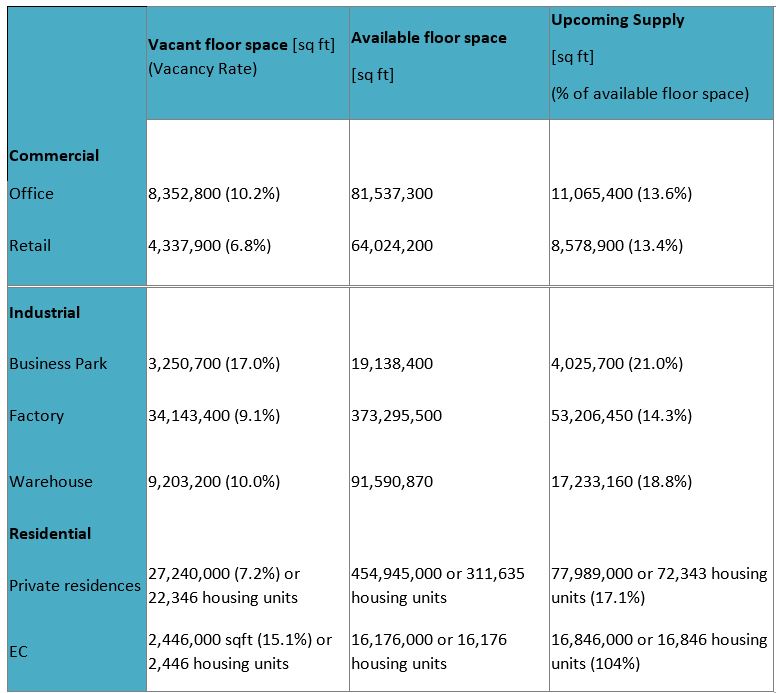

Real estate data for the first quarter of 2015 released in the last week of April revealed a total of 59,288,000 sqft of vacant nett lettable area in the Industrial and Commercial segments. Most of us cannot visualise the expanse of 59 million sqft of empty space. Given that the nett lettable area of Vivocity is about 1.04 million sqft and that most readers in Singapore would have visited Vivocity before, perhaps we might be able to relate to 59 vacant Vivocity’s. Or for those more familiar with the football pitch, perhaps we might try to imagine 770 empty football fields.

The residential segment is not much better. 22,346 vacant units of private residences and a record high 2,446 vacant Executive Condominium (EC) units. The 22,346 vacant private residences comprise 2,447 units of landed properties and 19,899 units of apartments and condominiums. If we assumed each landed property unit to have an average of 3,000 sqft of built in area and while non-landed and EC units have an average of 1,000 sqft of built in area, the vacant space in the private residential and EC segments will total 29,686,000 sqft.

That is equivalent to 29 vacant Vivocity’s. Or 386 empty football fields. Take your pick.

Table 1: 1Q2015 data on the Commercial, Industrial and Residential (including ECs) segments.

Source: Century 21, JTC, URA

It is yesterday’s news that the Industrial segment is facing a massive oversupply with 46 million sqft of vacant space, mostly concentrated in the “Factory” category. The islandwide vacancy of Factory space is about 34.1 million sqft, or 9.1% of total stock. 36% of all vacant factory stock comes from the sub-category of “Multi-User Factory Space” in the private sector, which is more commonly known to us as: strata-titled factory space. The vacancy rate of Multi-User Factory Space in the private sector stands at 13.4%, which represents a whopping 12.2 million sqft of empty factory units, most of which are small and not entirely suitable for manufacturing use. The proliferation of shoebox industrial units since 2010 is now taking its toll on landlords who are facing stiff competition for tenants. Most landlords are lowering their asking rentals despite increases in loan expenses due to rising interest rates.

Strangely, the data on the factory rental index and transacted price index are not reflecting the reality on the ground yet. According to data from Jurong Town Corporation (JTC), the Multi-User Factory rental index increased from 102.8 in 4Q2014 to 102.9 in 1Q2015 while the price index increased from 107.7 in 4Q2014 to 107.8 in 1Q2015. While an increase of 0.1% may not be statistically significant, it is a large deviation from what practising property agents are reporting: that landlords are lowering their selling prices and asking rentals by 5-15%.

It is a similar situation in the Office category, where weakening sentiments are not yet evident in the official data. The quarter-on-quarter vacancy rate stayed flat at 10.2% while the rental index increased by 0.6% on the back of a 0.1% drop in the price index. Several weak spots in the economy are beginning to affect Singapore negatively: slower growth in the Chinese economy, a prolonged downturn in oil prices, cancellations and delays in orders for oil rigs, a multi-year slowdown in the residential market, etc. While new office space may still see healthy take-up rates from MNCs, the space they vacated in older buildings may not fill up as fast.

The Retail category used to be my favourite category but it is now the source of my biggest concern about the Singapore real estate market. Already disadvantaged by a small home market and listless growth in tourism arrivals, retailers also face a shortage of labour, higher salaries, increased foreign worker levies and competition from online stores. Many retailers are experiencing financial losses and a few foreign brands such as Lowrys Farm and Francfranc have closed and withdrawn from the Singapore market in the past twelve months.

The overall vacancy rate increased from 5.8% in 4Q2014 to 6.8% in 1Q2015. In absolute terms, vacant retail space increased by 635,000 sqft to a total of 4.3 million sqft in 1Q2015. The price index remained flat at 130.7 points during these periods while the rental index dropped 0.4 points to 118.0 in 1Q2015.

There are many strata-titled retail shops in mixed developments that have remained empty for over 2-3 years from the time they were completed. More of such mixed developments (retail-office, retail-residential, retail-hotel, etc) will be completing in the next 2 years. The correction in rental rates will be welcomed by retailers. Against these negatives, landlords might consider divesting their retail units but they have to contend with a thin buyer’s market.

Looking forward, the scenery is not a pretty one. New residential supply will hit a record high this year with an additional 25,400 private residential and EC units expected and is expected to hit another record high in 2016 with 25,769 units completed. We also expect to see spikes in the supply of Office space (over 5 million sqft) and Factory space (over 20 million sqft) in 2016. Furthermore, there is some cannibalisation within these categories as certain types of tenants can choose to operate their businesses out of either categories. Note that we have not even touched on the record high supplies of HDB flats and the massive completions of residential, office and industrial space across the border up north.

With major global economies still mired in uncertain growth, and the oil and commodities industries facing strong headwinds, it is unlikely that the demand for Singapore’s real estate will surge to match the strong supply numbers. I would expect to see higher vacancy rates, weaker rentals and lower capital values across all segments right up till 2018.

This article appeared in The Edge Property Pullout of Issue 678 (May 25) of The Edge Singapore.

Ku Swee Yong is a licensed real estate agent and the CEO of Century 21 Singapore.

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search