OPINION: Can the market absorb the supply from this year’s GLS sites?

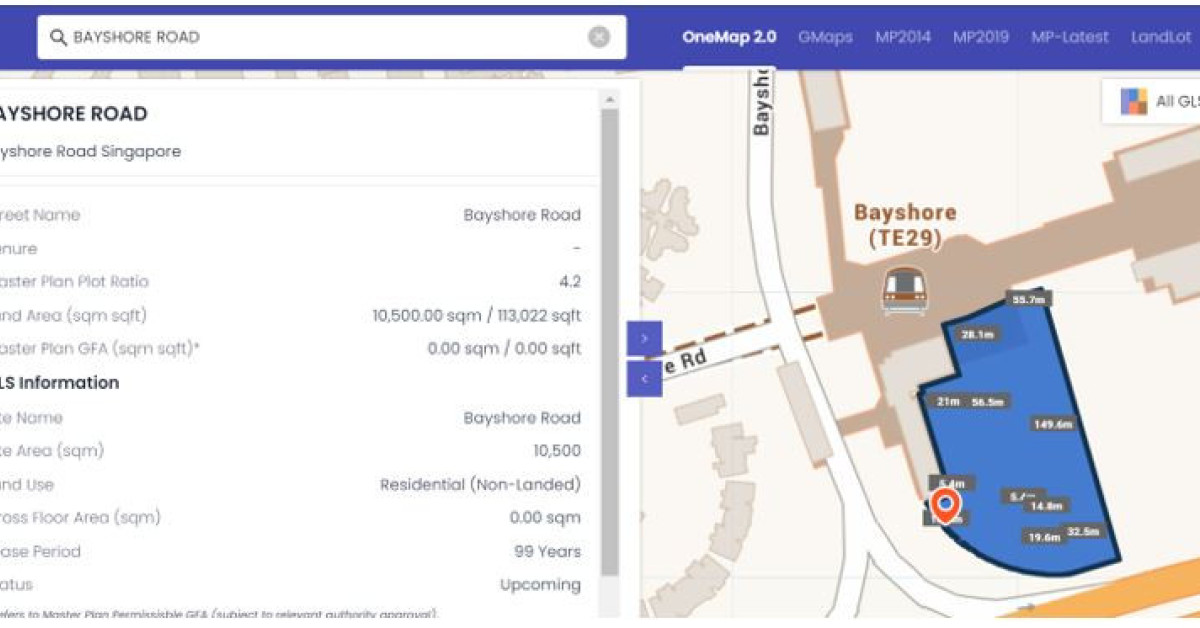

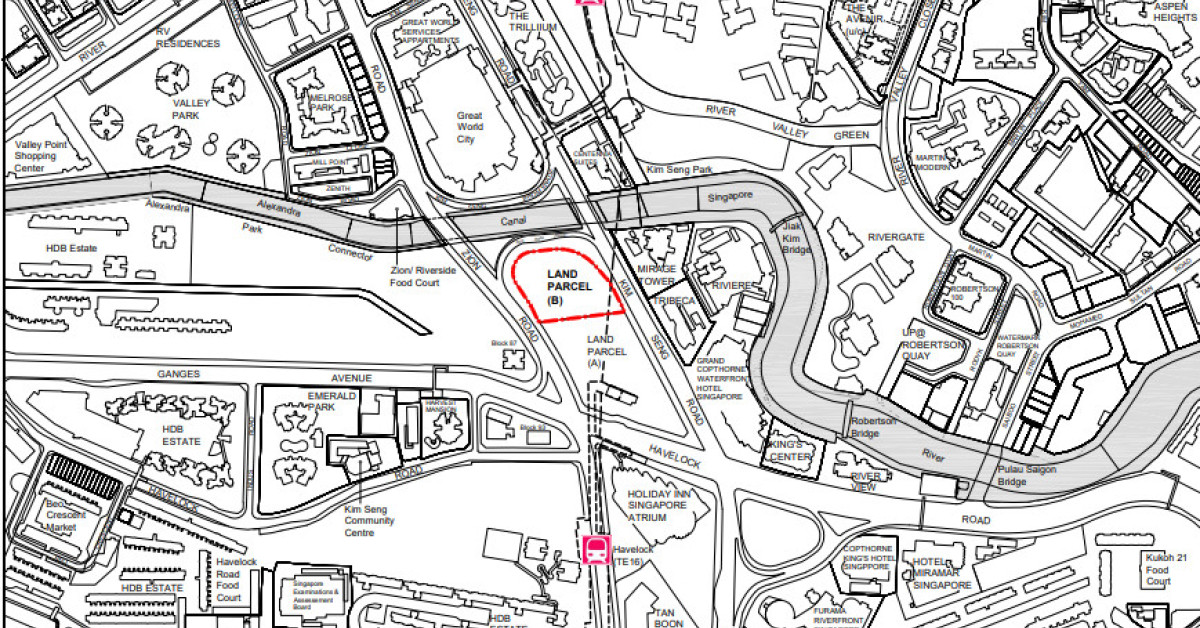

The GLS lists for this year feature a number of sites along Zion Road and River Valley Green. (Photo: Samuel Isaac Chua/EdgeProp Singapore)

Ask Buddy

SINGAPORE (EDGEPROP) – The confirmed and reserve lists for the 2H2024 Government Land Sales (GLS) programme were announced last month. The sites on the latest confirmed and reserve lists will yield an estimated 5,050 and 3,090 residential units, respectively. The sites on both lists for the 2H2024 GLS programme will yield a total of 8,140 units if executive condos (EC) are included, down from a total of 8,910 units from the 1H2024 GLS programme.

The decline in future condo units from the most recent GLS lists could be the government’s response to developers’ lacklustre responses to recent GLS tender closings. In February, URA rejected the lone bid for the Marina Gardens Crescent GLS site because the bid price was considered too low. Additionally, no bids were submitted for the Upper Thomson Road (Parcel A) GLS site when its tender closed last month.

Number of unsold condo units building up

Developers' recent lukewarm response to GLS tenders could be because some of them still have unsold inventory. The total number of unsold condo units increased from 14,330 units in 2021 to 16,145 units in 2022, before rising further to 17,256 units last year. As of the first quarter of this year, there were 20,195 unsold condo units (see Chart 1).

Of greater concern is the growing number of completed and unsold condo units, which rose from 176 units in 2021 to 259 units in 1Q2024. URA data for 2Q2024 will be available only at the end of July.

Buyers’ preference shifting to resale?

Since 2021, resale transactions have made up the majority of condo sales. In 2021, resale transactions comprised 56% of the total sales volume, increasing to 69% in the first half of this year (see Chart 2). Conversely, new sales accounted for 44% of the total volume in 2021 but dropped to 24% this year. This shift in buyer preference toward resale units may have contributed to the rise in unsold new condos. However, it is too early to determine if this trend will continue.

Source: EdgeProp Market Trends (as at 8 July 2024)

The price difference between new and resale condos could have contributed to more buyers purchasing resale units. The difference between the average prices for new sale and resale condos was only $459 psf in 2020 but rose to $639 psf in 2021 and $705 psf this year (see Chart 3).

Furthermore, the average resale price is still below $2,000 psf, but the average new sale price broke through this benchmark in 2021. This is despite a 5.1% y-o-y drop in the average price to $2,402 psf for new condos, while the average price for resale condos increased by 4.5% y-o-y to $1,697 psf.

Source: EdgeProp Market Trends (as at 8 July 2024)

Construction delays might also be prompting buyers to opt for resale units instead of new, unfinished ones. During the pandemic, the annual number of completed condo units dropped to fewer than 10,000. However, this figure rebounded to 19,968 units last year (see Chart 4). The decline in completions and the construction delays during the pandemic were caused by shortages of materials and manpower.

Construction costs on the rise

Besides construction delays, the materials and manpower shortages also resulted in higher construction costs. According to the International Construction Market Survey 2024 by Turner & Townsend, rising construction cost is a key challenge for developers in Asia. Consequently, developers may attempt to manage rising development costs with more conservative bids for GLS sites.

Moreover, Turner & Townsend has identified Singapore as the eighth most expensive Asian city to do construction (see Chart 5). Construction cost in Singapore increased by 8% last year but the rate of increase is expected to ease to 5% for this year.

Developers have to pay ABSD if unable to meet deadline

Developers in Singapore also face punitive consequences if they are unable to build and sell all units in their development within five years of being awarded the site. Developers have to pay additional buyer’s stamp duty (ABSD) amounting to 40% of the land price when they purchase a site. However, part of the total ABSD, amounting to 35%, is remittable if the developer is able to meet the five-year deadline. The possibility of having to pay an additional 35% for the land parcel increases development risk for developers.

However, developers received some reprieve when the government announced a tiered clawback in February. For developers who purchased their land on or after February 16, the ABSD rate of 34% is applicable if they manage to sell 90% of the units in their development. The applicable rate drops to 25% if 99% of the units are sold.

However, developers are expected to try to sell out their development before the deadline because the decline in ABSD clawback is not a significant amount. If the developer buys a land parcel for $100 million with plans to build 500 condo units, then the developer would still have to pay ABSD of $25 million (25% of $100 million) if he has only five unsold units (1% of 500 units) after the five-year deadline. Furthermore, the reprieve is unlikely to have a significant impact on the developers’ development risk assessment when purchasing land, and hence their cautious stance is unlikely to change significantly in the short run.

Impact of ABSD on foreign buyers

The government implemented an increase in the ABSD rate last year. The biggest change was for foreign buyers, who saw their applicable rate jump from 30% to 60%.

As a result of the increase in ABSD rate for foreign buyers, they purchased fewer condo units. The number of units purchased by foreign buyers dropped from 923 units in 2022 to 619 units last year and only 116 units in the first half of this year. Since the increase in the ABSD rate last year, foreign buyers have purchased only 360 condo units (see Chart 6).

The decline in the number of units purchased by foreign buyers could have contributed to the subdued number of bids and bid prices in recent GLS tenders, especially for sites in the core central region (CCR). Since 2022, more than 50% of the condo units purchased by foreign buyers have been in the CCR (see Chart 7). Even with the significant increase in the ABSD rate for foreign buyers, condos in the CCR still represent 52.3% of total condo sales to foreign buyers.

Demand still expected for upcoming units

The sites on the two confirmed lists for this year will yield an estimated total of 10,500 housing units, an increase over the 9,250 housing units from last year’s confirmed lists. However, if executive condos (ECs) are excluded, the sites from this year’s lists will yield approximately 9,230 condo units compared to 7,990 condo units from last year’s lists.

The sales volume for new condos was 12,548 units in 2021 but fell to below 7,000 units in 2022 and 2023. For the first half of this year, only 1,850 new condo units have been sold (see Chart 8). The rolling three-year average for new sales volume followed a similar trend, albeit falling less sharply, from 10,249 units in 2021 to 9,577 units in 2022 and 8,535 units last year.

The two confirmed lists for this year’s GLS programme are expected to yield an estimated 9,230 condo units, which is on par with the rolling average of 8,535 new condo units sold last year. However, there is still a significant number of unsold condo units, reaching a three-year rolling average of 15,910 units last year.

On the bright side, the rolling average for unsold units has eased from 23,007 units in 2021 to 18,268 units in 2022. This is a good indication that developers are gradually clearing their unsold inventory.

Comparing the rolling average for the supply and sales volume of new condo units indicates that the difference between both averages is declining, falling from 12,758 units in 2021 to 8,691 units and 7,375 units in 2022 and 2023, respectively (see Chart 9). This indicates the unsold inventory is gradually shrinking on the back of resilient demand.

We did some projections for new sale volume and the number of unsold units to forecast whether the market would be able to absorb the upcoming supply. Bearing in mind that 1,850 new condo units were sold in 1H2024, we assumed that new sale transactions will hit 4,000 units this year. We estimated that total unsold new condo units for this year might reach approximately 25,800 based on the 17,256 unsold units at the end of last year, plus the estimated 12,600 new units that will be launched this year and less our projected number of new units that will be sold this year.

The rolling three-year average for unsold units will increase to approximately 19,700 units this year, but the rolling average for sales of new condo units will drop to approximately 5,600 units, resulting in a difference of approximately 14,000 units. This is a significant increase over the differences of 7,375 units last year and 8,691 units in 2022 but is on par with the difference of 12,758 units in 2021. However, higher differences of 21,378 units and 20,039 units were noted for 2020 and 2019, respectively.

As such, the market should be able to absorb the upcoming units, albeit at a slower pace. Recent new launches indicate that take-up rates of 20% to 30% can be expected during the launch weekend. About 23% of the units in Sora were sold during its launch last weekend and The Hill @ One-North achieved a take-up rate of 30% when it was first launched in April. Developers are expected to continue being selective and conservative in their bids to avoid paying ABSD for unsold units beyond the five-year deadline.

Ask Buddy

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search