'Significant reordering' in Asia Pacific data centre market; power and execution risks to intensify

Power constraints remain a key challenge, driving data centre expansion into emerging markets with lower development costs and stronger power availability. (Image: Shutterstock)

The Asia Pacific (Apac) data centre market is undergoing a “significant reordering” — shifting from concentrated growth in traditional hubs to rapid expansion in “power-advantaged” locations, such as Malaysia, Australia and India, that can support large-scale cloud and AI deployments, according to a CBRE report.

It comes amid rising AI adoption and growing power constraints, with power availability increasingly determining where new capacity can be delivered.

A separate report by Moody’s Ratings similarly notes that constraints in mature hubs are pushing incremental investment towards emerging markets, while data localisation rules and government incentives continue to underpin demand.

“Growth will increasingly disperse to emerging markets such as India, Malaysia, Indonesia, Thailand and Vietnam,” notes Moody’s.

The firm also highlights the South and Southeast Asia region as one of the fastest-growing data centre markets globally, with capacity expected to double by 2030. However, the pace and distribution of growth will increasingly depend on power availability, grid stability and execution capability.

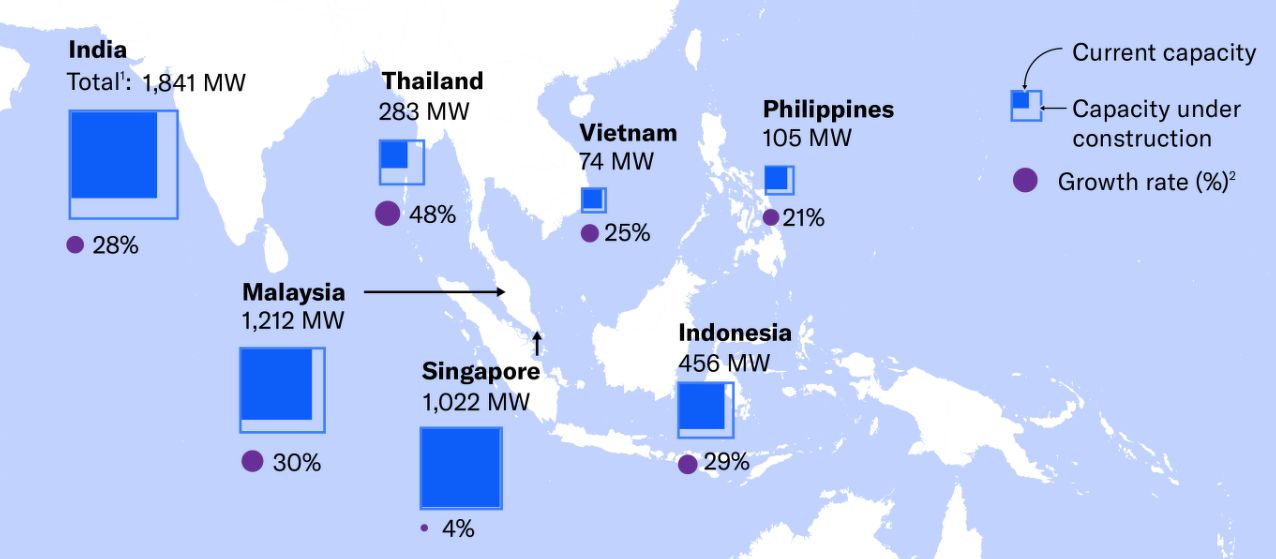

India and Singapore are the region’s largest data centre markets, with incremental capacity growth shifting to emerging markets:

Note: 'Total' represents current and under-construction capacity. Growth rate reflects CAGR for 2025-30. Sources: Cushman & Wakefield, Moody's Ratings estimates.

Hyperscalers — the large-scale cloud computing infrastructure typically used for frontier AI models — are increasingly pursuing build-to-suit campuses and joint ventures with data centre developers, particularly in India, Indonesia and Malaysia. Their aim is to secure power and land, scale more quickly and improve cost certainty amid rising power and construction costs.

In South and Southeast Asia, growth is further supported by China’s hyperscalers expanding outside their home market to diversify operations and ecosystems, Moody’s adds.

Chinese data centre operators have set up subsidiary operations in emerging data centre markets in Southeast Asia, particularly Malaysia, Indonesia and Thailand, to support their multinational clients.

Power availability redirects capacity expansion

Backed by sustained demand for stabilised assets, development sites and conversion opportunities, direct investments in the Apac data centre market have grown steadily over the past seven years before reaching a record US$11.6 billion ($14.85 billion) in 2025, the CBRE report states.

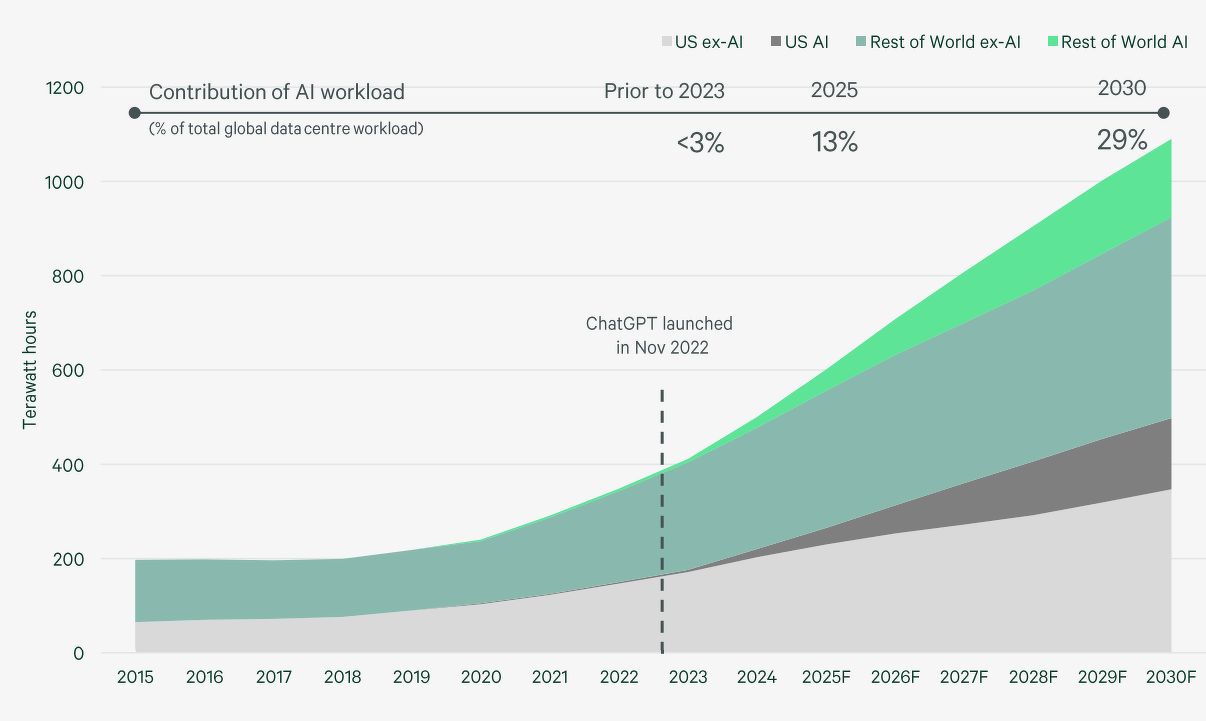

While the pipeline remains strong, power is still a major challenge. Electricity consumption by Apac data centres almost doubled from 2020 to 2024, and is likely to triple over the next few years.

New builds are also increasing in capacity, with average sizes now exceeding 100MW. Intensive AI workloads are placing further strain on power infrastructure.

Global data centre electricity consumption: 2015–2030 (forecast):

Source: Goldman Sachs, CBRE Research (February)

As a result, so-called "power-advantaged" markets that can support rapid scaling are emerging as focal points. In 2025, Johor led the region with a sharp 53% y-o-y surge in live capacity, followed by Melbourne with a 37% increase.

That is in contrast to the more modest 6–8% growth recorded in mature markets such as Singapore and Hong Kong, although CBRE attributes this to development constraints as opposed to a lack of demand.

Malaysia, Australia and India are securing a larger share of incremental demand as hyperscalers prioritise scalability and delivery certainty in the race for power.

"Upcoming pipeline projects are frequently measured in the hundreds of megawatts, and in some cases approach gigawatt-scale campus formats," CBRE writes.

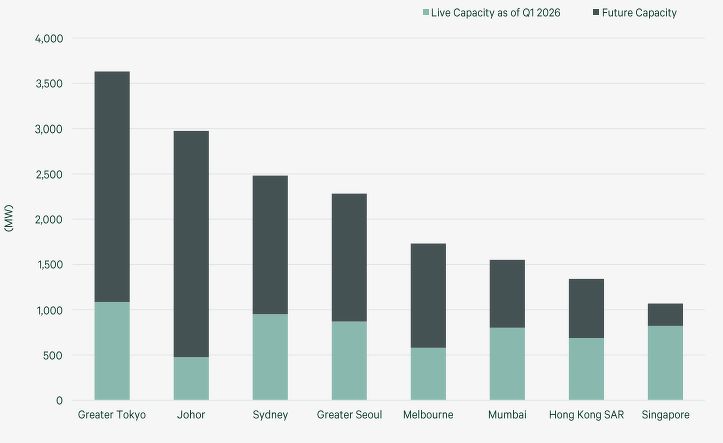

Pipeline of data centres in Asia Pacific (in megawatts, MW):

Source: CBRE Data Centre Solutions, CBRE Research, April 2026.

Ada Choi, head of research for Apac at the real estate consultancy, says that as AI adoption accelerates, Apac is expected to remain “one of the most important global growth regions, with attractive opportunities in power-secure, AI-ready markets”.

Meanwhile, Moody’s flags that power and execution risks will intensify in South and Southeast Asia as the operational capacity of data centres in the region is set to increase at a compound annual growth rate (CAGR) of 24% over the next four to five years.

Power availability sets the ceiling for capacity expansion, determining market scalability and risk, while grid reliability and permitting processes determine the speed to market.

In Johor, growth has benefitted from available land and power, and Malaysia has a solid power reserve margin. However, further scaling will depend on the timely delivery of new generation capacity and grid expansion, Moody’s says.

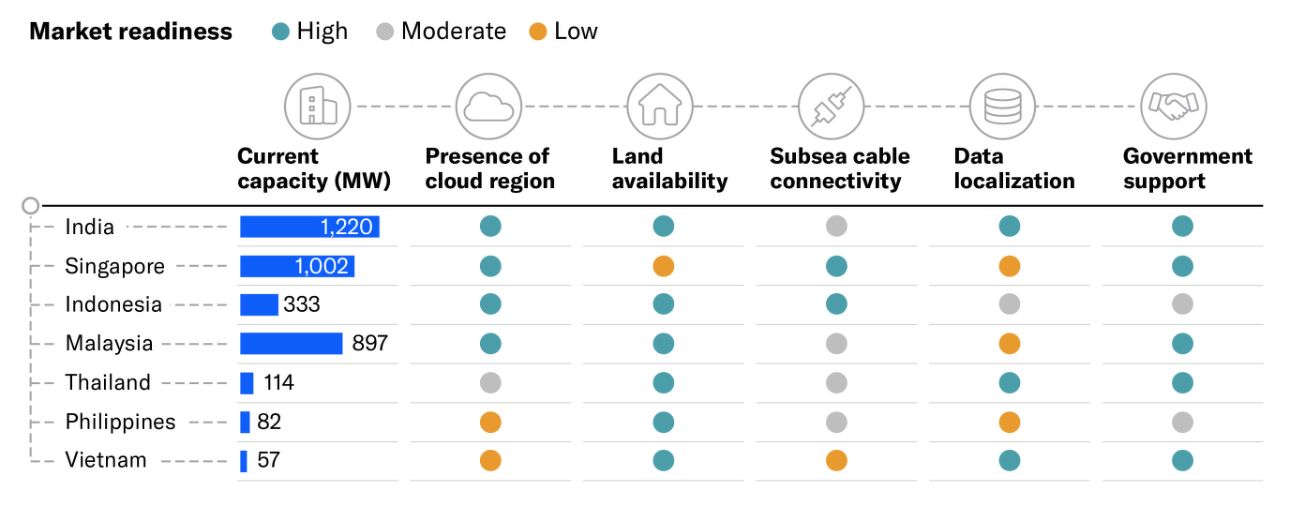

Market readiness for data centre capacity additions differs across South and Southeast Asia:

Source: National authorities, Moody's Ratings.

As for India, it is better positioned to absorb incremental data centre-related demand as it has a track record of commissioning new generation and grid infrastructure.

Moody’s notes that India’s ability to cater to additional power demand reflects its much larger power market, within which data centres represent only 1% of installed capacity, according to the International Energy Agency.

Even if data centre capacity in India were to grow at the upper end of the range forecast by market participants, the amount of energy consumed will likely remain below 5% of the market at that point.

Neoclouds emerge as new demand driver

While traditional hyperscalers continue to drive the bulk of data centre activity, CBRE points to the growing presence of neoclouds — a new class of AI-focused cloud providers — in the region.

Neocloud operators are seeking rapid expansion to support high-intensity AI training and inference workloads. This is adding depth and diversity to the demand base for data centres.

Global neocloud operators such as Nebius are starting to expand into Apac, while regional players such as Australia’s Sharon AI and Firmus have also emerged.

This surge in near-term demand has worsened capacity shortages within the region’s existing data centre pipeline.

Opportunities vary by market, depending on power availability and infrastructure readiness. This is because neoclouds require specialised infrastructure that includes high power density, advanced cooling systems and ultra-low-latency network infrastructure.

For example, CBRE sees limited prospects in certain parts of Japan and South Korea, as a lack of power availability is constraining development in core Tokyo and Seoul. Hong Kong has both inadequate power and building specifications, while mainland China has sufficient power but a lack of access to graphics processing units (GPUs).

On the other hand, South and Southeast Asia — excluding Singapore — have high potential for neocloud development, in CBRE’s view. Attractive markets for growth include Malaysia, Indonesia and Thailand, thanks to cheaper power, better access to sufficient power, easier permitting conditions and proximity to Singapore.

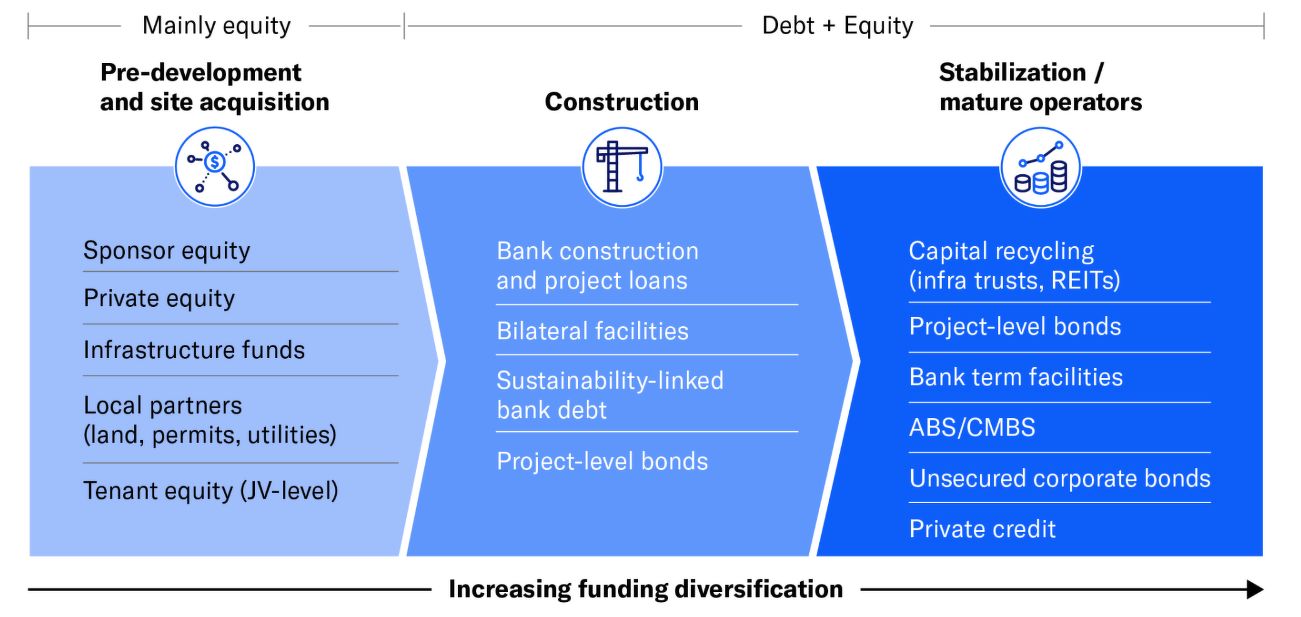

Financing structures, investment routes evolve

As assets transition from development to stabilisation, capital structures are evolving in tandem.

Moody’s points out that development capital for data centres in South and Southeast Asia has mainly been provided in the form of sponsor equity, private equity, infrastructure investment, and bank financing.

This reflects the early growth phase, which includes greenfield development risk, potential construction delays, limited operating track records and uncertainties around power access and tenant ramp-up.

Looking ahead, the firm reckons there will be more diversification in data centre financing, due to asset maturation, platform scaling and a growing emphasis on sustainability-linked funding structures.

Funding sources will diversify as sector matures:

Source: Moody's Ratings

“We expect private equity and infrastructure funds to remain significant capital providers, but with more selective underwriting that prioritises projects with secured power, pre-committed tenants and credible sustainability strategies,” Moody’s says.

As more hyperscale-anchored campuses reach stabilisation, operators will likely pursue capital recycling strategies and refinance construction debt with longer-tenor project-level bonds, the credit ratings agency adds.

Similarly, CBRE has observed a rise in fund management models, through which operators and developers recycle capital by spinning assets into fund or partnership structures.

This is among the different channels investors are using to access data centre assets, as investment activity is becoming bifurcated by asset size and risk appetite in a maturing market.

Direct investment continues to appeal to investors seeking smaller ticket sizes, asset-specific exposure and relatively better liquidity, especially among yield-focused Reits and domestic investors.

As for entity-level transactions, they have been relatively scarce but account for a significant share of capital deployment, CBRE notes. These strategies, primarily through platform and operating-company investments, provide investors with an efficient pathway to scale, particularly if they are targeting larger-scale assets or multi-market portfolios.

Live and future data centre capacity in Asia Pacific:

Note: The 5-year CAGR assumes all under construction and announced supply pipeline to be completed over the next five years. South Korea data cover only Greater Seoul. Thailand data cover only Greater Bangkok. Mainland China data cover only Tier 1 cities. Source: CBRE Data Centre Solutions, CBRE Research, April 2026.

CBRE believes Tier 1 cities in India as well as emerging Southeast Asian markets offer attractive growth opportunities.

It adds that markets with high growth potential, such as Osaka, Brisbane, Thailand and Indonesia, can provide cheaper options for investors considering development plays.

For more news and analysis, read our weekly e-paper. Prefer a print copy? Get it delivered to your home every Monday.

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search