Singapore’s residential sector will be a buyer’s market in 2020: CBRE

SINGAPORE (EDGEPROP) - Overall, CBRE expects Singapore’s property market to remain resilient despite macroeconomic headwinds. This is highlighted in CBRE’s report “Real Estate Market Outlook 2020 - Singapore”, which gives projections for the property sectors of residential, office, retail, logistics, and the capital markets.

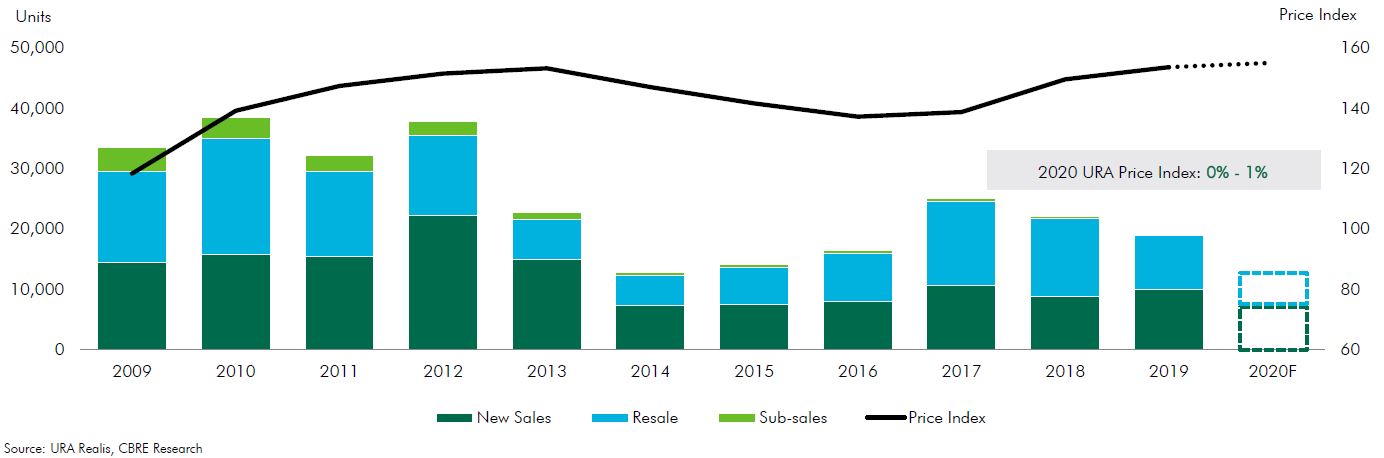

In 2019, there was a record number of 52 launches. New sales dominated the private residential market with 9,912 private residential units sold. It represented a 12.7% y-o-y increase, signalling improving buyer sentiment despite property cooling measures.

There are 40 projects scheduled for launch and an additional unsold inventory of 30,473 units in 2020. Thus, CBRE foresees that 2020 will be a buyer’s market and property buyers will be spoilt for choice. However, projects from the Core Central Region (CCR) will continue to have high demand, making up close to 40% of units available for launch in the year.

Chinese buyers are unlikely to feature in the short term due to the Covid-19 outbreak, but are expected to return in the middle to long term. In 2019, the Chinese accounted for 19.3% of new home purchases in the CCR, excluding those by Singaporeans.

In terms of property prices, there are no significant pressures to reduce prices or give discounts as the level of unsold inventory is still manageable. In addition, most of the projects with additional buyer’s stamp duty deadline in 2020 either have their units 100% sold or close to fully sold.

CBRE Research expects prices to stabilise and could achieve between 0% and 1% growth in 2020 due to high land costs.

Price per quantum per unit from 2017 to 2019 (Graph: CBRE Research)

For this year, CBRE projects that the price quantum of $2.0 million per unit will continue to be the sweet spot for investors. Residential property buyers are likely to be more price-sensitive, preferring smaller units. As it is, the median size for units transacted has declined from 828 sq ft in 2017 to 721 sq ft in 2019.

In spite of the virus outbreak, developers are moving ahead with new launches while taking precautionary measures at showflats.

Low interest rates are likely to fuel and sustain the underlying demand from both local and foreign investors.

Total private residential demand from 2009 to 2019. Graph: CBRE Research

However, sales volume is expected to be slower than in 2019. CBRE Research expects new home sales to fall within the range of 7,000 to 8,000 units and resale volume to fall within the range of 6,000 to 7,000 units.

Read also:

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search