Singapore industrial rents rise 0.5% in 3Q2025, capping five years of steady gains

An example of new activity in Changi Business Park is RD American School, which opened in August (Photo: Samuel Isaac Chua/EdgeProp Singapore)

Ask Buddy

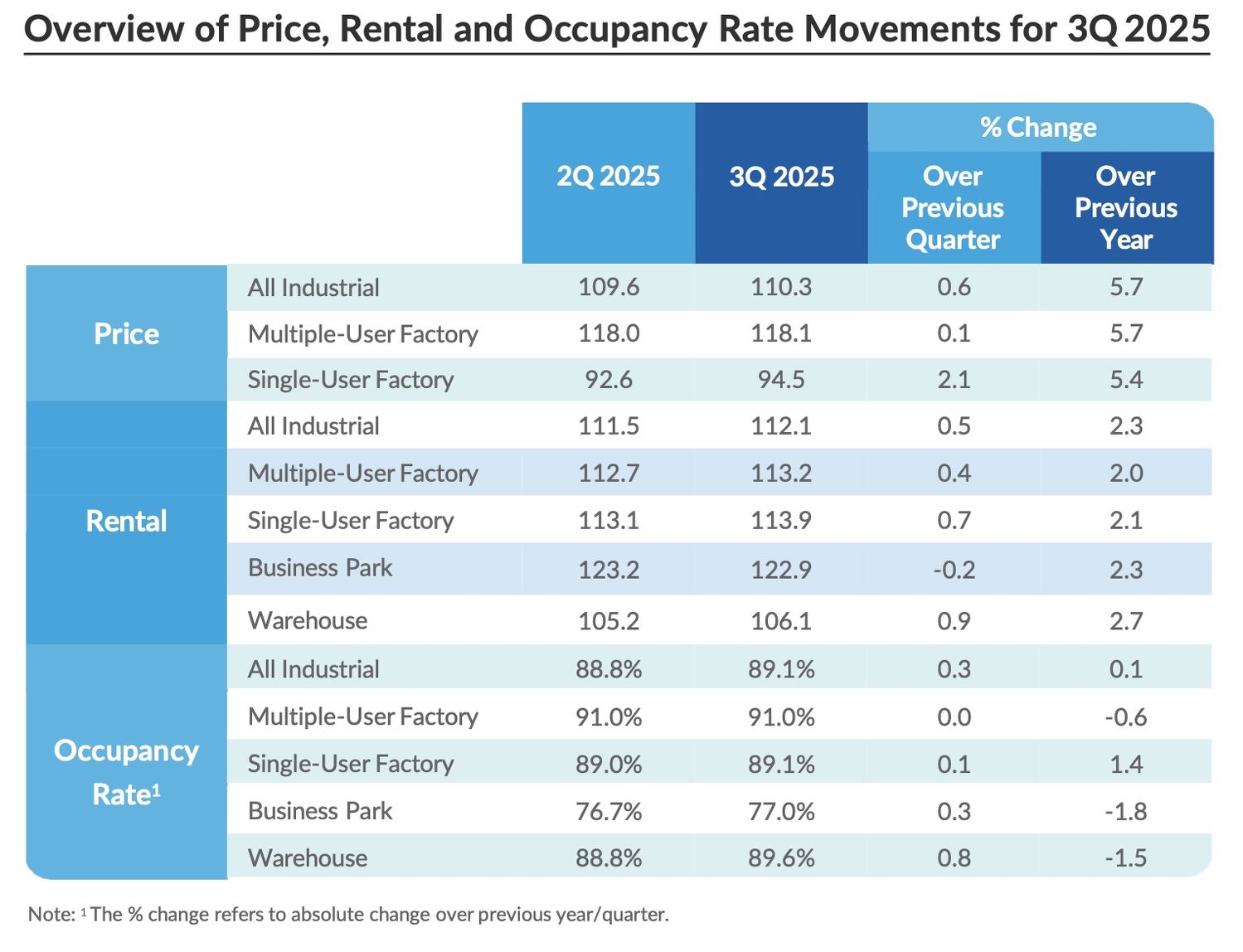

The overall rents for all industrial spaces in Singapore rose by 0.5% q-o-q in 3Q2025 and 2.3% y-o-y, according to JTC statistics released on Oct 23. This marks the 20th consecutive quarter of rental growth since the trough in 3Q2020, at the height of the pandemic. Since then, rents have climbed 25.3%.

Growth during the quarter was led by the warehouse segment, which saw a 0.9% q-o-q rise, accelerating from 0.4% in 2Q2025. The segment was buoyed by sustained demand for newer, well-located facilities and a continued flight to quality.

“With net absorption at its strongest since 2Q2023, and warehouse completions moderating compared to last quarter, occupancy rose by 0.8 percentage points to 89.6% in 3Q2025,” says Tricia Song, Head of Research, Singapore and Southeast Asia, CBRE

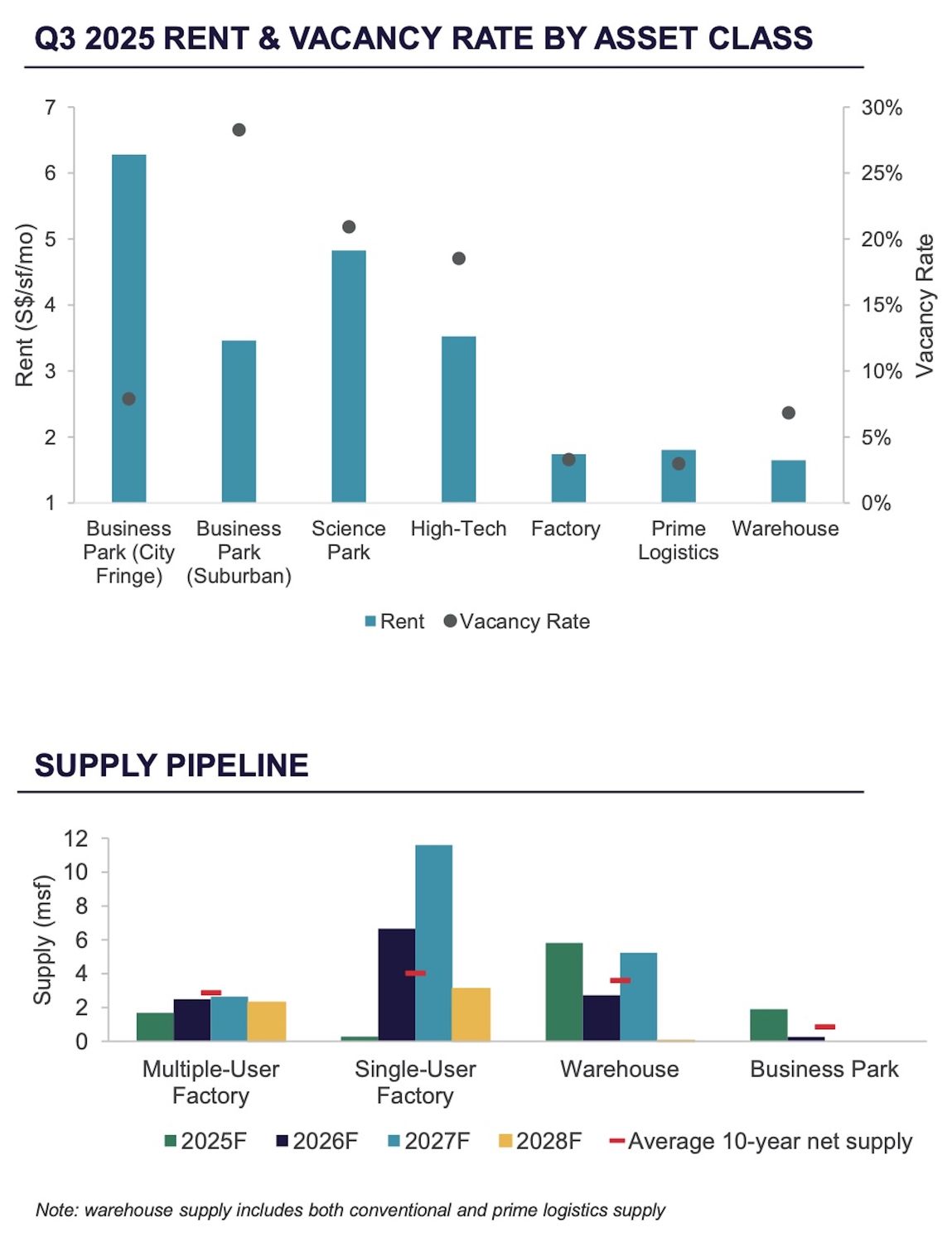

CBRE Research also observed robust take-up of prime logistics space, led by major third-party logistics (3PL) operators. As a result, occupancy for CBRE’s basket of prime logistics properties increased from 92.1% in 2Q2025 to 93.6% in 3Q2025.

Notable completions during the quarter included CapitaLand Ascendas REIT’s 5 Toh Guan East (0.55 million sq ft) and Toll Logistics’ facility at 60 Pioneer Road (0.13 million sq ft) — both strategically located near the upcoming Jurong Lake District.

“While overall leasing enquiries remain subdued, a few occupiers, particularly 3PL players, are exploring consolidation of their warehouse footprints within prime logistics developments to enhance operational efficiency,” says Brenda Ong, executive director and head of logistics & industrial services, Cushman & Wakefield (C&W) Singapore

Source: JTC Industrial statistics 3Q2025

Factory segments: steady but uneven growth

Rents for single-user factories rose by 0.7% q-o-q, accelerating from 0.4% in 2Q2025. Occupancy edged up by 0.1 ppt to 89.1%. The only notable completion was Novartis’ addition and alteration (A&A) works at its existing pharmaceutical manufacturing facility at 8 Tuas Bay Lane (0.09 million sq ft), notes CBRE.

Meanwhile, multi-user factory rents increased by 0.4% q-o-q, a moderation from 0.9% in 2Q2025. The quarter’s sole completion was CT FoodNEX at 2A Mandai Estate (0.20 million sq ft) — a 10-storey, freehold food factory comprising 109 production units and one canteen. Occupancy for this segment remained unchanged at 89.1%.

“Hi-tech spaces continue to be driven by flight to quality,” says CBRE’s Song. “Relocation activity remains healthy as landlords selectively offer incentives. Smaller occupiers, in particular, are drawn to fitted units that reduce start-up costs.”

Source: Cushman & Wakefield

Business parks: resilience amid a pause

Business park rents recorded a 0.2% q-o-q dip in 3Q2025, ending three consecutive quarters of growth. Nonetheless, rents were still up 2.3% y-o-y, reflecting underlying resilience, notes CBRE.

The slight decline followed a 1.2% q-o-q rise in 2Q2025. According to C&W’s Ong, the softening stemmed from landlords easing asking rents to sustain occupancy, particularly among older properties in mature business parks.

Older stock in the East and West regions has generally seen stagnant occupancy levels compared to newer properties in the Central region, adds Leonard Tay, head of research, Knight Frank Singapore. “Some of these assets are due for a refresh and repositioning to attract occupiers in the post-pandemic period.”

An example of new activity in Changi Business Park is RD American School, which opened in August. The campus introduces a new type of tenant to the area, notes Tay. “Its flexible layout with open, reconfigurable spaces fosters activity, curiosity, and social interaction — a shift from traditional classrooms.”

Knight Frank data shows lower occupancy rates in the East (73.0%) and West (63.1%) than in the Central region (85.4%), underscoring the case for rejuvenation and adaptive reuse.

Prices stabilise, demand remains resilient

Prices for industrial properties rose by 0.6% q-o-q and 5.7% y-o-y in 3Q2025, marking six consecutive quarters of prices outpacing rents. While this was the lowest quarterly increase in a year, it highlights steady investor confidence, says CBRE’s Song.

Single-user factory prices climbed 2.1% q-o-q, while multi-user factory prices inched up by 0.1%, moderating from 1.7% in 2Q2025.

Knight Frank’s Tay attributes the continued uptick to lower interest rates, a broader range of investible assets, and SMEs acquiring premises to ensure business continuity amid global uncertainty.

“With Singapore’s short- to medium-term interest rates easing faster than US benchmarks, investors are increasingly looking to deploy capital into defensive asset classes,” says CBRE’s Song. “Industrial real estate — particularly those with leasehold tenures — remains attractive for its stable returns and widening yield spreads.”

Supply outlook: tightening pipeline

As at end-September 2025, around 2.26 million sq ft of new industrial space — equivalent to 0.4% of total stock — is scheduled for completion in 4Q2025, according to CBRE.

The single-user and multi-user factory segments will contribute 61% and 35.6% of the upcoming supply, respectively, while the warehouse segment accounts for the remaining 3.4%.

No new business park projects are slated for completion in 4Q2025. Over the next three years, the only major pipeline project is 27 IBP (0.21 million sq ft), targeted for completion in 2026. “As more landlords undertake asset enhancement initiatives to improve the specifications of ageing facilities, supply is expected to tighten further,” adds Song.

Ask Buddy

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search