The most valuable part of the warehouse is the floor

In a goods-to-person industry, the product walks itself — on a robot — to the picker (Photo: Shutterstock)

Ask Buddy

The forklift has been replaced. The driver did not notice.

In April, Unitree humanoids performed kung fu on Orchard Road, then moved indoors to the Singapore Science Centre, where they ushered visitors and shared a bill with a comedy show titled, My Colleague is a Robot Dog.

In 2026, the humanoid performs. The robot that does the actual work has wheels, and the wheels run on concrete.

That robot — and its larger sibling, the automated forklift — was the main exhibit at Modex 2026 in Atlanta in April, the largest supply-chain trade show in the US. Fifty thousand attendees. One thousand exhibitors. The supply chain was declared a strategic weapon, not a cost centre, in the opening keynote.

The interesting question is not whether the robot works. The interesting question is what happens to the building once it does. Industrial property has traditionally been valued by location, tenure and specification. Robotics is introducing a fourth variable.

Dr Goh’s instruction

Since Dr Goh Keng Swee, Singapore’s “economic architect”, drained the swamps of Jurong in the 1960s, industrial users have answered the productivity call with more humans, then with humans and a crane, then with humans and more cranes and static automation.

The instruction has not changed. The technology answering it has.

Singapore industrial land is among the most expensive in the world, on leasehold terms shorter than the building it sits beneath.

Capex, automation, productivity per-square-metre — these make JTC officials happier. The operator who arrives with 40 workers and a 1990s forklift fleet does not excite the officer. The operator who arrives with technicians, supervisors and a robot fleet does.

Dr Goh did not need autonomous mobile robots. He merely designed a country in which they would eventually become obvious — and in which the concrete that the next tenant laid would matter more than the rent the previous tenant paid.

Robotics is creating a new hierarchy in industrial property. Some buildings can host the fleet. Some can be retrofitted for it. Some cannot. The market still prices many of them as if they belong to the same category.

Death of the (property) comparable

The industrial property market still speaks in comparables because comparables are comforting. A warehouse in one estate is compared with a warehouse in another; lease tenure, floor area, loading and access are adjusted until the spreadsheet stops complaining.

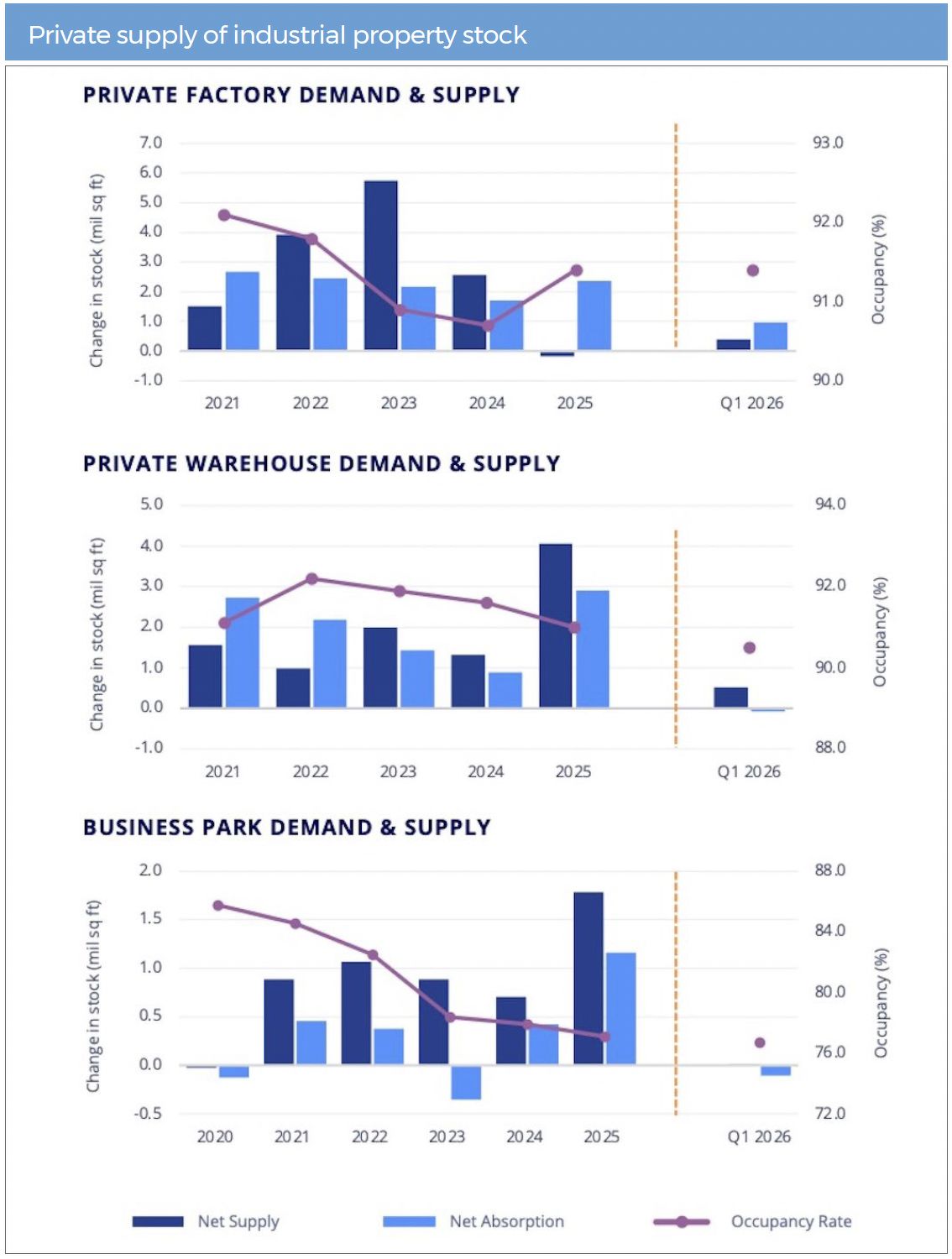

Chart: Colliers, JTC

Robotics makes the comparison less innocent. Two buildings with the same land area, tenure and zoning may no longer have the same productive ceiling — or, more precisely, the same productive floor.

One can host autonomous mobile robots (AMRs), autonomous forklifts, charging bays and orchestration software. The other can host a tenant querying why EDB’s productivity grants are not quite applicable this year.

The market calls both these spaces warehouses. The robot is less polite. Industrial property comparables are becoming less reliable because only one building may be capable of supporting the next generation of logistics operations.

Industrial rents have risen for 22 straight quarters into 1Q2026, even as tenants become more selective. Also, newer, higher-specification assets are holding demand better than older stock. The robot-first warehouse is the next step in that selection process. Location is priced first. Specification is priced next. Whether the floor can host the worker of the next lease is priced last, and not yet fully.

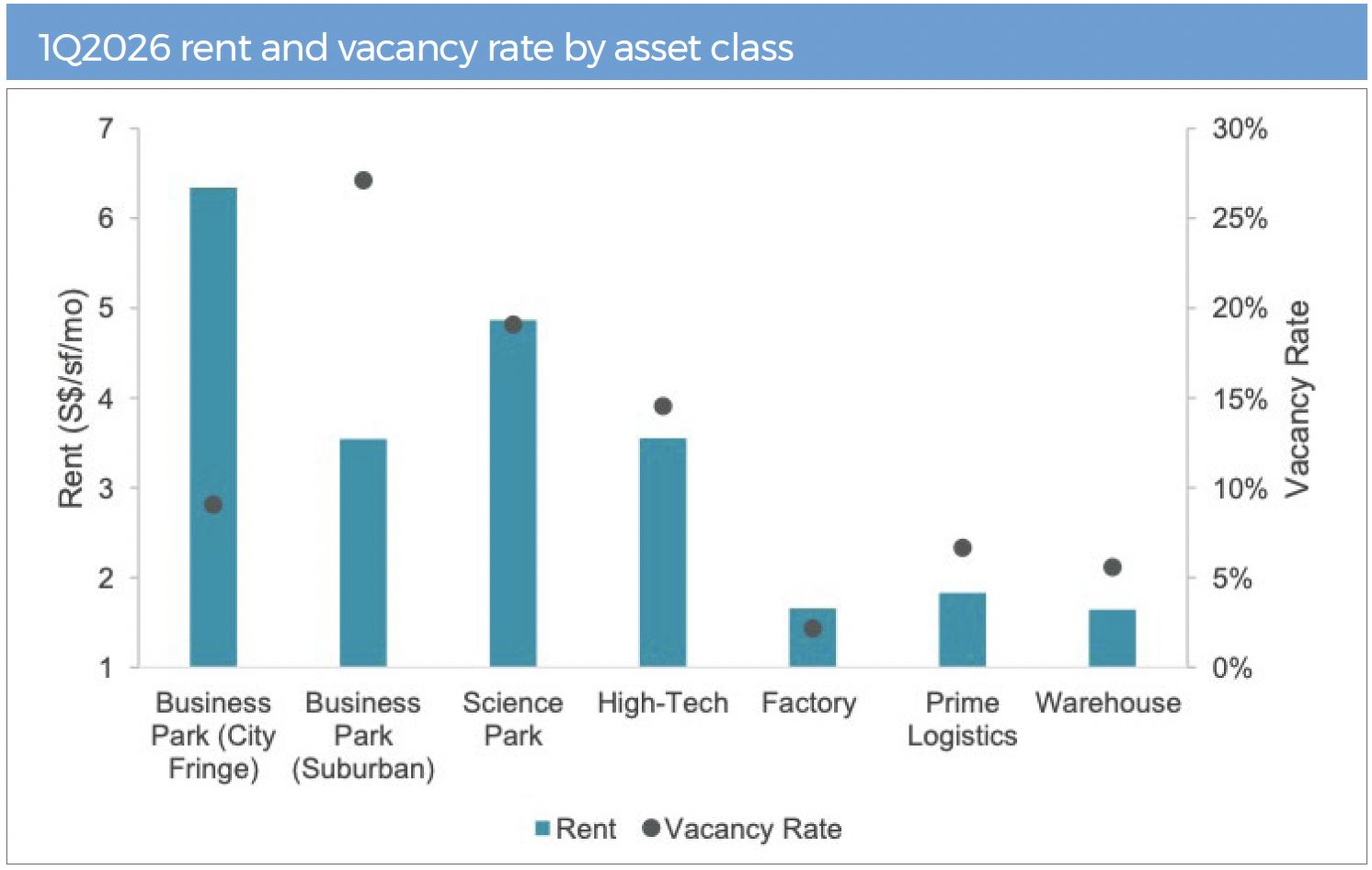

Chart: Cushman & Wakefield

Three conditions for productivity

Three conditions are required for the robot-first warehouse to make economic sense. Singapore has, with characteristic preparation, assembled all three.

The first is industrial land priced above the productivity of legacy labour. The JTC framework prices the floor space at a level only a productive enterprise can carry, and where the labour market is structurally tight — work-permit ratios capped, foreign-worker levies deliberate, and demographic reserve no longer expanding. The arithmetic favours the robot before the lease is even signed, and certainly before the Ministry of Manpower finishes counting the foreign-worker quota.

The second is a landlord that is rewarded for capex. The robot is the line item that converts the (now-acceptable) lease into a defensible cash flow. The floor, re-laid to AMR tolerance, is the line item that converts the building into one that a robot will accept.

The third is a deployment ecosystem dense enough to support fleet operations at scale. Singapore is not the headquarters of the AMR industry. It does not need to be.

It is the place where robotics vendors converge to support deployments — spare parts, software updates, integration engineers and fleet financing. The fleet does not need to be invented here. It needs to be serviced, financed and trusted here.

All three, on the same island, under the same regulator.

Singapore did not subsidise the robot into relevance. It made the alternative progressively harder to defend.

Amazon proves the point

In 2012, Amazon acquired warehouse automation company Kiva Systems for US$775 million. By mid-2025, the rebranded Amazon Robotics operated more than 1,000,000 mobile robots across its fulfilment network.

Before Kiva, Amazon’s human pickers, who walked 19km per shift, processed roughly 100 items per hour. After Kiva, the rate climbed to 300–400.

Amazon did not reduce its workforce as the robots arrived; it upskilled 700,000 workers across 300 facilities. Amazon calls them cobots — collaborative robots. The framing is deliberate.

Tesla will almost certainly make the humanoid Optimus commercially real one day. The warehouse, being less sentimental than the demo stage, has already chosen wheels.

Amazon proves the worker can be reorganised around the robot. Singapore’s question is different: it’s whether the building can be reorganised before the rent makes the old model indefensible.

Robots now doing the work

The AMR is the workhorse. A knee-high to waist-high wheeled platform, it navigates the warehouse floor without rails or fixed routes, lifts an entire shelf from underneath, and brings it to a human pick station at the perimeter. Goods-to-person, in industry shorthand. The product walks itself — on a robot — to the picker. Fleet sizes deployed at single sites now run into the thousands.

The AMR reads the floor before it reads anything else. The wheel knows where the building wants the robot to go before the controller does. A floor laid to appropriate flatness — tolerances measured in millimetres, not mood — is what makes the wheel a worker rather than a complaint. A floor laid to 1990s standards is what makes the same wheel slow, jittery and more expensive to run.

Beside the AMR sits the automated forklift — a self-driving counterbalance truck or reach truck. AMRs move boxes and totes; automated forklifts move pallets, at heights of 14m, or beyond. The automated forklift’s wheel base is wider, its turning radius tighter and its battery heavier. Both robots demand the same floor.

Above the floor sit mobile manipulators — AMRs with a collaborative robot arm bolted on top — which analysts at Modex tipped as more likely than the humanoid to steal the limelight once the hype subsides. Underneath the floor sits the orchestration software layer: warehouse control systems conducting an orchestra in which the players are AMRs, forklifts and conveyors.

None of this looks like a humanoid. None of it dances. All it cares about is concrete.

The sensor layer is what makes the robot the worker. Light detection and ranging smarts, machine vision and safety scanners allow the fleet to navigate around racks, pallets and human ankles in real time. Accident rates at automated facilities are a fraction of those in legacy operations.

The human’s job has shifted — from lifting and walking to coordinating and orchestrating. The job did not vanish. The walking did.

The old answer

When productivity per-square-metre first became the variable that Singapore industry optimised against, the answer was the automated storage and retrieval system (ASRS). Fixed cranes, dedicated rack geometry and a control system ran the building like one machine.

The ASRS did not care about the floor. It ran on rails. The crane ran on a track engineered for the box that the operator was shipping that year. The floor underneath the crane could be uneven, cracked or load-rated for the previous tenant’s pallet weight. None of it mattered. The rail mattered.

This is why the ASRS aged the way it did. It was a marriage of convenience. An ASRS facility is configured for a single product geometry at the time of commissioning.

The crane runs the aisle it was built to run. The rack accommodates the box it was built to accommodate. When the operator’s product mix changes — and in Singapore’s logistics, it always does — the ASRS is the trapped capital which the operator services for the rest of the lease.

By contrast, the AMR and autonomous forklift do not commit. They do not require a dedicated aisle. They do not assume a particular box. When the warehouse profile changes, the navigation stack and fleet management software reroute. When the lease expires, the fleet goes to the next building.

A floor laid to AMR tolerance is a permanent improvement to the building — readable by the next enterprise’s fleet, priced into productivity figures. The ASRS leaves behind a steel cage. The AMR fleet leaves behind concrete.

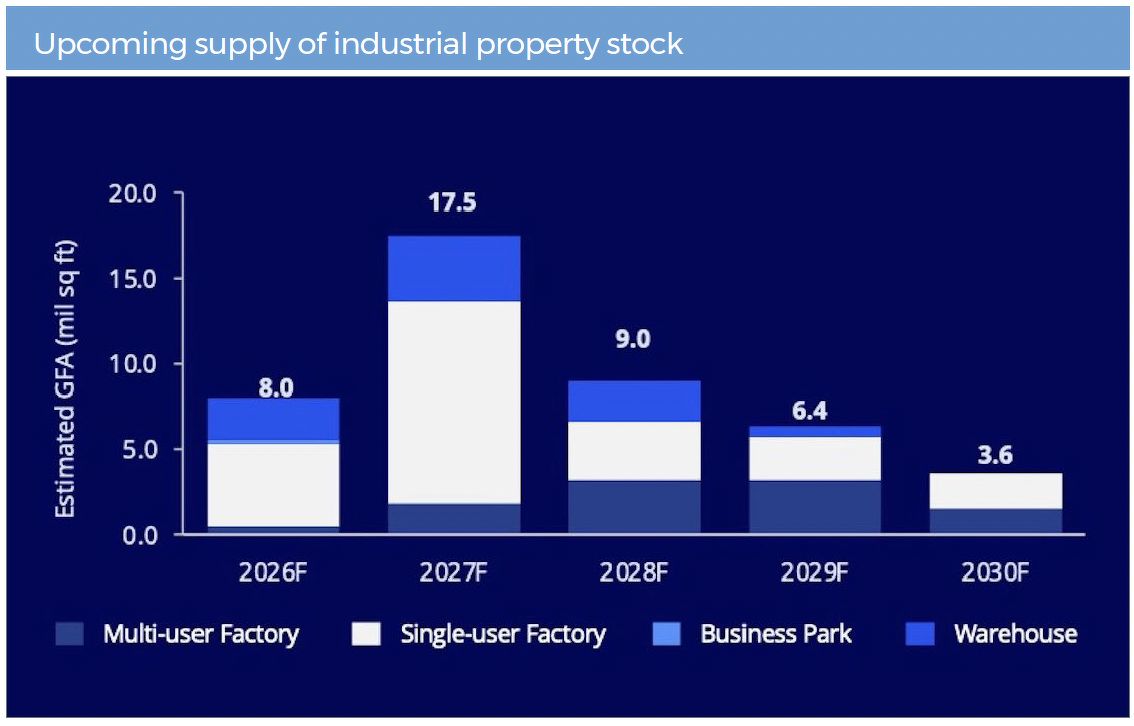

Chart: Colliers, JTC

New warehouse specification

The robot-first warehouse is not a warehouse with robots installed. It is a building specified, at construction, for the worker that the rent now requires. The ceiling is higher than it used to be. There is no URA planning rule capping the floor-to-ceiling height of a single-floor warehouse in Singapore. Until the robot, anything above 6m was architecture. After the robot, it is inventory.

But the more important specification is below the ceiling, not above. In the old warehouse, the floor held the goods. In the new one, it holds the business model. The new building also dedicates an area to charging infrastructure, which the old building did not need. Loading bays used to be the warehouse’s mouth. Charging zones are now its bloodstream.

Singapore’s industrial stock is unusually vertical. Multistorey and ramp-up factories were rational responses to land scarcity, but robotics will expose the difference between vertical density and operational density.

A building can stack floors and still be awkward for a fleet — narrow-turning radii, sloped circulation, fragmented charging zones, and fire compartmentation that breaks up orchestration paths. Singapore solved land scarcity by stacking industry. The robot will now grade the stack, one floor at a time.

Once robotics becomes part of the building specification rather than the tenant fit-out, industrial property stops being one asset class — it becomes three.

Three types of warehouses — which one is mispriced?

The first is the legacy shell. Low height, weak floor loading, awkward design and concrete that was never laid to the tolerances a fleet requires. The market still prices it as cheap industrial space. The robot cannot operate inside it at any meaningful productivity. This is terminal obsolescence.

The second is the retrofit-capable asset. Sufficient height, sufficient power, sufficient remaining lease and floors that can be re-laid to modern tolerance. The market discounts it as old stock. The robot sees a usable chassis and a floor that can be made readable.

Some short-leased JTC industrial warehouses — discounted for age rather than genuine physical incapacity — sit in the second asset group. Cheaper to buy than to build, often below replacement cost. The market sees an ageing warehouse. The robot sees a usable platform.

The third is the new, purpose-built robot warehouse, specified at construction for the fleet, the floor, the ceiling, the charging architecture and the orchestration software.

The legacy shell is correctly priced as obsolete. The new build is correctly priced at a premium.

The mispricing sits in the second — the retrofit-capable asset — which is priced as if it were the first and operates as if it were the third.

The market has historically rewarded location, tenure and specification. Robotics may force it to reward productive capacity instead.

Obsolescence in industrial property has historically been gradual. The lease shortens. Local banks decline to lend.

Robotics introduces a more binary form. Either the floor can hold the fleet, or it cannot. Either the tolerance works, or the robot slows down. Either the power and charging layout support operations, or the fleet becomes an expensive queue.

In a robot-first warehouse, the forklift’s beep — and driver — will be gone (Photo: Shutterstock)

New robotic workforce

Walk a robot-first warehouse end-to-end. It is quieter than the one it replaced. The forklift’s beep is gone. The picker’s footfall is also gone. What remains is the steady hum of charging cycles and the occasional voice of a supervisor reviewing fleet performance on a screen.

The building accommodates both. The floor accommodates both.

Industrial obsolescence has historically been measured in decades. Robotics may compress it into a single leasing cycle. The next valuation report may not ask how old the warehouse is. It may ask whether the floor can host the workforce that modern logistics now prefers.

The forklift has been replaced. The driver did not notice. He is now coordinating the fleet.

The old warehouse waits for its next valuation report, where it will discover that the floor was never just the floor.

Chunkky Lim is the pen name of a Harvard MBA and former hedge fund professional who now helms his family office, managing a diversified real estate portfolio across industrial, commercial and residential sectors

Ask Buddy

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search