Singapore investment deals hit $33.68 bil in 2025 as big-ticket transactions return

Despite a volatile global landscape in 2025, Singapore remained an attractive investment destination, says Michael Tay, advisory deputy managing director and head of capital markets at CBRE Singapore. He attributes this resilience to “Singapore’s reputation as a stable and secure investment destination, coupled with solid fundamentals”.

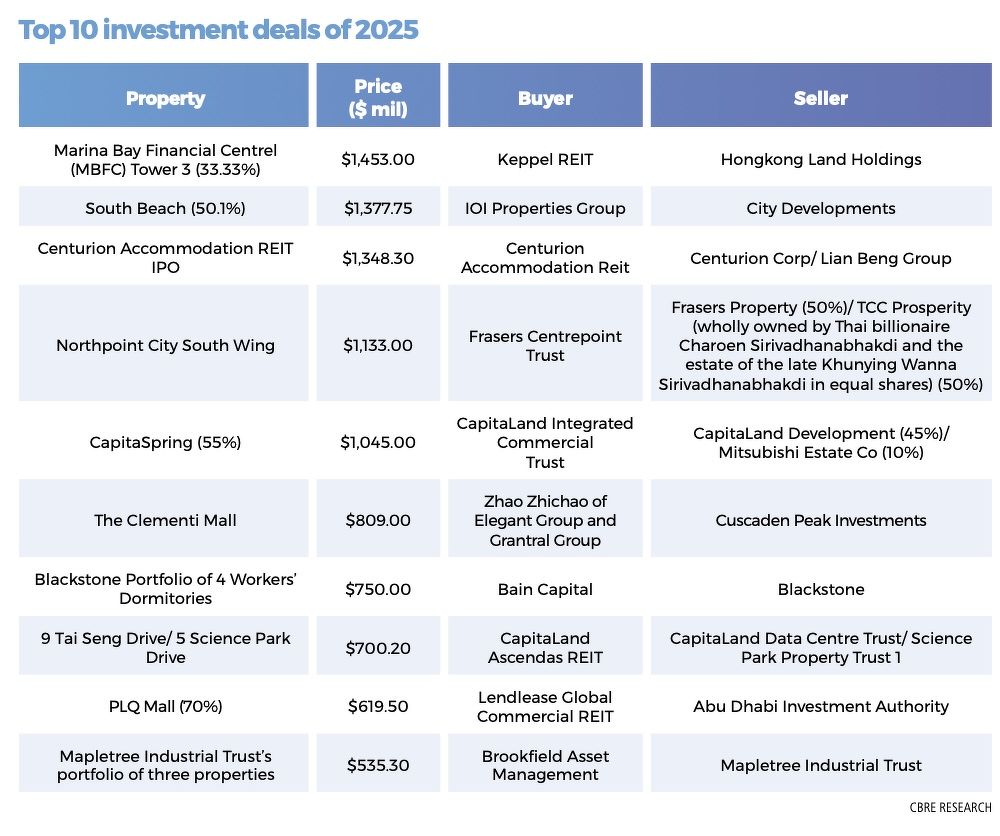

Big-ticket transactions, buoyed by a late-year surge in deal activity, lifted total investment sales to $33.68 billion for the year, estimates CBRE. Among the standout transactions was the year’s largest deal — Keppel REIT’s purchase of Hongkong Land’s one-third stake in Marina Bay Financial Centre (MBFC) Tower 3 for $1.453 billion in December.

Other late-year transactions included Brookfield Asset Management’s acquisition of a portfolio of eight industrial and logistics assets from ESR REIT for $338.1 million; developer Victor Soh of Pinnacle Assets’ $148 million purchase of a Good Class Bungalow (GCB) at Peirce Road; and the sale of another GCB at Dalvey Estate for $41.6 million.

Overall, investment volumes were 16.8% higher than the $28.84 billion recorded in 2024, says Tricia Song, head of research for Singapore and Southeast Asia at CBRE. Beyond big-ticket transactions and public land sales, activity also picked up across shopping malls, industrial portfolios and the living sector — including existing serviced apartments as well as sites acquired for redevelopment into co-living or long-stay serviced apartments, she adds.

Mega deals anchor 2025 activity

Including the September 2025 listing of Centurion Accommodation REIT with an initial portfolio value of about $1.35 billion, five of the top 10 deals in 2025 were mega transactions exceeding $1 billion.

While the largest deal was Keppel REIT’s acquisition of the one-third stake in MBFC Tower 3, another standout was City Developments’ sale of a 50.1% stake in the mixed-use South Beach development to Malaysian conglomerate IOI Properties Group for $1.38 billion in June.

Two other mega deals involved related-party REIT transactions: the sale of Northpoint City South Wing to Frasers Centrepoint Trust for $1.13 billion in March, and the sale of a 55% stake in CapitaSpring to CapitaLand Integrated Commercial Trust for about $1.05 billion in August.

The sale of Northpoint City South Wing to Frasers Centrepoint Trust for $1.13 billion was one of the largest deals of the year (Photo: Samuel Isaac Chua/EdgeProp Singapore)

Shopping malls featured prominently among the significant transactions, including Northpoint City South Wing ($1.13 billion), Clementi Mall ($809 million) and PLQ Mall ($619.5 million).

“Excluding related-party transactions, 2025 still ended strongly,” says Jeremy Lake, managing director of investment sales and capital markets at Savills Singapore. “Clementi Mall was the largest private investment sale to close in 4Q2025 and stood out for both record pricing and the high number of bids received (12).”

Clementi Mall was the largest single property sale to close in 4Q2025 and stood out for both record pricing and the high number of bids received (12) [Photo: Samuel Isaac Chua/EdgeProp Singapore]

Residential and GLS dominate investment volumes

The residential sector — driven largely by government land sales (GLS) — accounted for about 47% of total investment deals in 2025, estimates CBRE. Developers’ sentiment strengthened amid robust new home sales and easing borrowing costs. “Developers are now hungry to replenish their depleted land banks,” observes CBRE’s Song.

One surprise entrant was HH Investment, linked to Taiwan’s Huang Hsiang Construction Corp, which paid $1,820 psf per plot ratio (psf ppr) for the Bukit Timah Road GLS site in November. This marked the highest Core Central Region (CCR) land rate since April 2018, when SC Global Developments and its partners acquired a Cuscaden Road site for $2,377 psf ppr.

Competition was also intense for suburban sites. The Bedok Rise GLS site drew 10 bids, with the top offer of $464.8 million ($1,330 psf ppr) submitted by Allgreen Properties, making it the most keenly contested land tender of the year, notes Song.

Other notable GLS transactions included the Bayshore Road site, which attracted eight bids and set a new benchmark of $1,388 psf ppr, and the Dunearn Road site at Bukit Timah Turf City, which drew nine bidders and secured a top bid of $1,410 psf ppr. The latter is expected to serve as a pricing anchor for future developments in the new housing area, says Chua Yang Liang, head of research and consultancy for Southeast Asia at JLL.

Despite strong participation, pricing discipline remained evident, says Karamjit Singh, CEO of Delasa. “Pricing did not overheat; it stratified,” he notes. While CCR parcels set new benchmarks, Singh adds that strong Outside Central Region (OCR) and Rest of Central Region (RCR) sites consistently cleared within a relatively tight $1,300–$1,410 psf ppr range.

Stalled developments at the 60%–70% consensus level could revisit the process, resulting in more collective sale attempts (Photo: Samuel Isaac Chua/EdgeProp Singapore)

Collective sale revival?

The government is reportedly reviewing whether to lower the collective sale consent threshold to 70% from 80%. Such a move could prompt stalled developments at the 60%–70% consensus level to revisit the process, resulting in more collective sale attempts, says Nicholas Ng, senior director of capital markets at JLL.

However, Singh cautions that mega en bloc deals — particularly those yielding more than 2,000 new units — still carry significant sell-through risk within the 5.5-year timeline.

Beyond the consent threshold, another major hurdle remains the “significant buyer-seller price gap”, particularly for freehold sites, “where owners are setting reserve prices that developers find difficult to justify in the current market”, says CBRE’s Tay. This is compounded by the attractive pipeline of GLS sites in the 2H2025 and 1H2026 programmes.

For CCR sites, the 60% additional buyer’s stamp duty (ABSD) imposed on foreign owners has been another constraint. “It’s a double whammy — developers struggle to secure consent from foreign owners while also worrying about weaker buying interest from foreign purchasers due to the hefty ABSD,” Tay adds.

Data centres, in particular, continue to see robust demand from hyperscalers, enterprises and AI-driven businesse (Photo: EdgeProp Singapore)

‘Another strong year for industrial’

2025 was another “very strong year” for the industrial sector, says Jeremy Lake of Savills Singapore.

Food manufacturers and logistics operators are increasingly seeking high-specification spaces to support supply-chain diversification, according to Chua Yang Liang of JLL. “Freehold tenure enhances capital appreciation and liquidity, while the shift towards integrated, high-specification districts is reinforcing developer interest,” he says.

Data centres, in particular, continue to see robust demand from hyperscalers, enterprises and AI-driven businesses, notes Andrew Mackin, director of data centre and industrial & logistics services at CBRE.

Supply, however, remains constrained by Singapore’s tightly controlled approval regime, keeping vacancy rates below 5%. While Johor and Batam have absorbed some spillover demand, Singapore remains the preferred hub for mission-critical workloads, Mackin adds.

The government’s Data Centre Call-for-Application is expected to release about 200MW of new capacity, largely on Jurong Island, with awards anticipated between mid- and end-2026. Nonetheless, many operators, citing higher perceived operational and location risks associated with Jurong Island, are actively exploring sites on the Singapore mainland, says Mackin.

In the investment market, data-centre assets remain tightly held, with few arm’s-length transactions. Mackin points to CapitaLand Ascendas REIT’s acquisition of a carrier-neutral data centre at 9 Tai Seng Drive from another CapitaLand entity for $455.2 million in May. Separately, NTT divested its Singapore SG1 data centre through the listing of NTT DC REIT, generating proceeds of US$259 million ($331.7 million) for the 8.6MW facility.

One of the significant office deals this year was the sale of JEM office block to Keppel Sustainable Urban Renewal Fund (Photo: Samuel Isaac Chua/EdgeProp Singapore)

‘Resurgence in office sector’

The office sector saw a resurgence of interest in 2025, says CBRE’s Tay. Domestic interest rates have fallen by close to 180 basis points since the start of the year, restoring positive carry for office investments.

Renewed appetite was reflected in large transactions such as CapitaSpring ($1.05 billion) and the Jem office block ($462 million), notes Pamela Ambler, JLL’s head of investor intelligence for Asia Pacific.

Sentiment was further buoyed by improving occupancy levels. New developments — including IOI Central Boulevard Towers and Paya Lebar Green — are substantially (over 95%) and fully leased, respectively. “With several big-ticket office assets expected to enter the market, there is a strong case for the office sector to outperform in 2026,” Tay says.

The IPO of Centurion Accommodation REIT marked a milestone in the institutionalisation of purpose-built worker accommodation (Photo: Centurion Accommodation REIT)

Living, hospitality gain traction

The living sector emerged as a key growth area in 2025, with the IPO of Centurion Accommodation REIT marking a milestone in the institutionalisation of purpose-built worker accommodation. Regulatory reforms under the Foreign Employee Dormitories Act have accelerated professionalisation in the sector, says Chua of JLL.

“Singapore’s co-living sector has matured rapidly over the past two years — transforming from a niche alternative into a recognised and increasingly institutionalised asset class,” adds Chua.

Capital markets activity is expected to further boost the segment. Recent and upcoming listings in the living sector — including Centurion Accommodation REIT, Coliwoo Holdings and the proposed IPO of The Assembly Place — are likely to support deal momentum, notes JLL.

One of the top hotel deals of the year was the sale of Hotel Miramar for $160 million to Aravest (a unit of Sumitomo Mitsui Finance & Leasing) and Wee Hur Holdings, to be rebranded DoubleTree by Hilton (Image: Aravest and Wee Hur Holdings)

Hospitality also stood out as a strong performer. The hotel sector recorded the fastest growth in 2025, with investment volumes rising 137% year-on-year, says Pamela Ambler of JLL. Notable transactions included the sale of Hotel Miramar for $160 million to Aravest (a unit of Sumitomo Mitsui Finance & Leasing) and Wee Hur Holdings, to be rebranded DoubleTree by Hilton; Citadines Raffles Place for $280 million to a consortium including BlackRock and YTL Corp; and Momentus Serviced Residences Novena for $100 million to a BlackRock-led group.

Boutique hotels also featured prominently. Duxton Reserve was sold to a family office for $80 million. “Boutique hotels have emerged as attractive investments, now comprising around 51% of Singapore’s total hotel supply,” says Ambler. “Investor interest is driven by demand for authentic and personalised guest experiences, as well as supportive government policies on heritage conservation and adaptive reuse.”

Reflecting the convergence of living and hospitality strategies, another notable deal involved the $75 million sale of a bungalow on Claymore Road to Asok Kumar Hiranandani of Royal Group of Companies. The property is expected to be repositioned as a long-stay, luxury serviced-apartment project under URA's SA2 (minimum three-month stay). “Claymore Road is a very strong location supporting a luxury serviced apartment development targeting high-end corporate and embassy tenants,” says Singh of Delasa.

A bungalow on Claymore Road was sold for $75 million to Asok Kumar Hiranandani of Royal Group of Companies, to be repositioned as luxury long-stay serviced apartments (Photo: Samuel Isaac Chua/EdgeProp Singapore)

Cautious optimism for 2026

With a limited supply of institutional-grade assets, capital is expected to remain selective, notes CBRE’s Song. Even so, market activity is likely to stay resilient, supported by a more favourable interest-rate environment, she adds. “We foresee investors remaining keen on industrial properties, driven by continued rental growth and the widening of already-positive carry.”

Similarly, Lake of Savills expects private investment volumes to rise further, underpinned by narrowing bid-ask spreads and renewed investor confidence. He believes the suburban retail segment will continue to perform well in 2026, with the office market also gaining traction.

However, the outlook remains tinged with uncertainty, “due in part to the continued unpredictability of US trade policies and the potential escalation of geopolitical tensions”, notes Tay of CBRE.

“While further easing of domestic interest rates would be supportive of growth and investment appetite, potential inflationary pressures arising from tariffs could tighten global financing conditions and, in turn, dampen investor sentiment,” Tay adds.

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search