Looking Ahead

Property investors seeking opportunities in the bearish residential property market need to look beyond capital appreciation as poor market sentiments continue to prevail. Though seemingly attractive deals may be available in today’s languid market, a prudent purchase is likely to be a wiser investment. Quick gains will be tough to come by as demand for residential properties falls due to tighter lending rules. Prices are also expected to face downward pressures due to a strong pipeline of newly completed projects entering the secondary market.

Market Performance

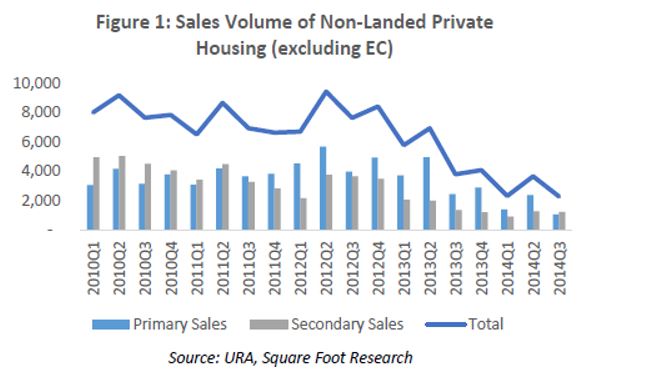

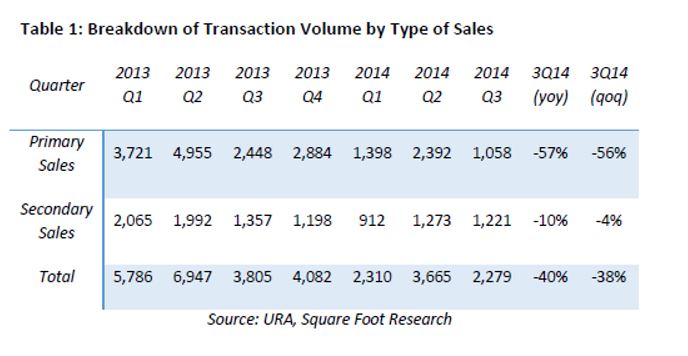

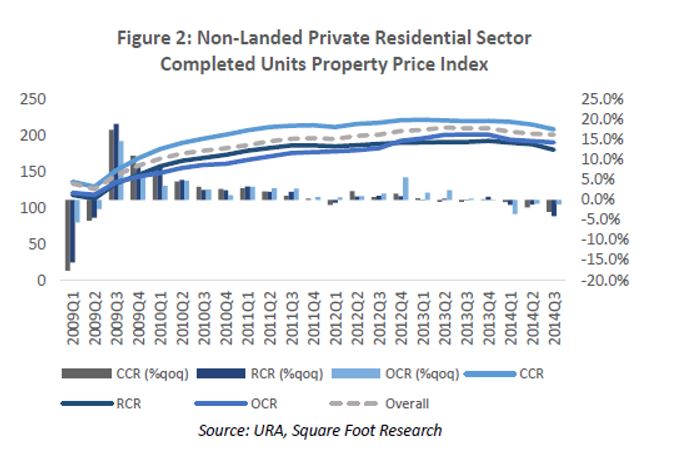

Transaction volume in the non-landed housing segment fell by 53.6% q-o-q in 3Q14 as a result of a lackluster primary market (Table 1). Price correction in 3Q14 is more pronounced for completed units where overall prices dropped by 4.3% y-o-y as compared to 2.6% y-o-y in the primary market.

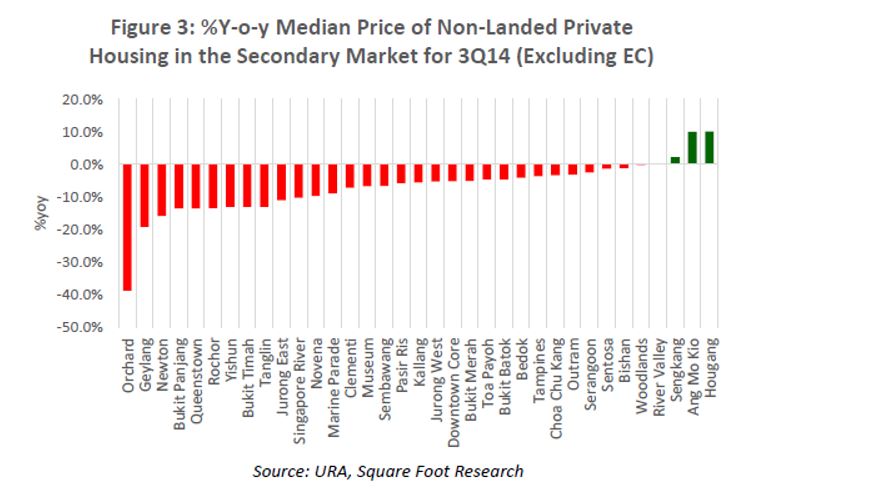

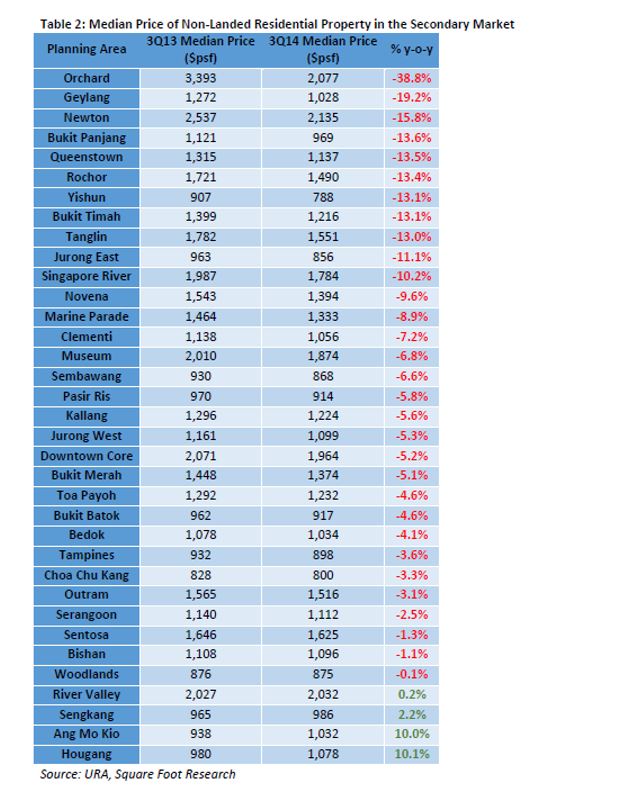

Prices saw the greatest dip in the Orchard area where overall median price in the secondary market fell by 38.8% in 3Q14.

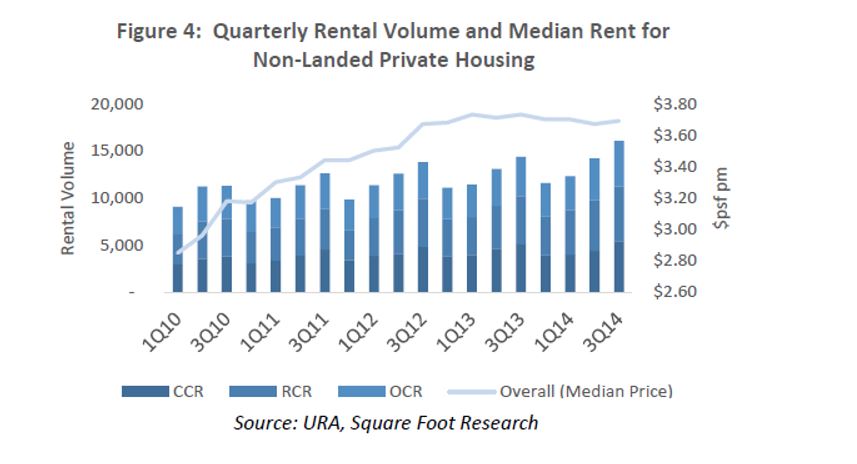

Rental Market

Rental volume surged by 13.1% q-o-q and 11.8% y-o-y to 16,050 rental contracts signed in 3Q14, the highest since 2000. Median rent, however, remained relatively stagnant at around $3.7 psf pm, a level since 3Q12. Overall rental price index fell by 1.1% q-o-q and 2.2% y-o-y with the largest correction in CCR followed by OCR and RCR (Table 2). Notably, rental contracts in CCR increased by 25% q-o-q in 3Q14 to a 5-year record high of 5,425 records even though the region had the highest price correction.

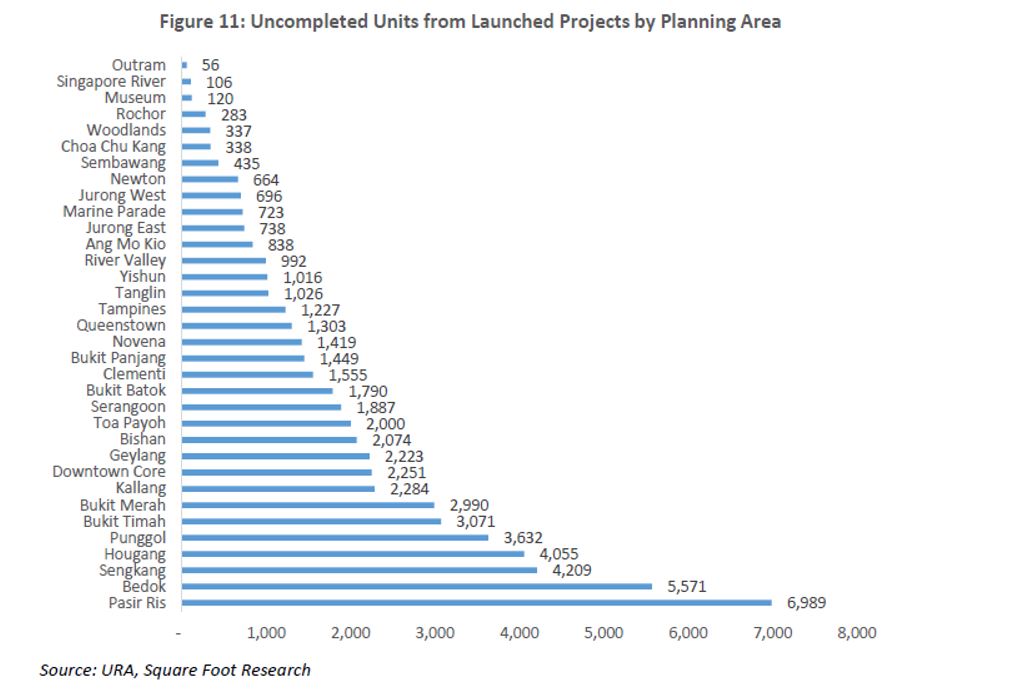

The rental market is likely to remain competitive in the short run due to an avalanche of supply from completing projects launched since 2010 coupled with stricter hiring policies for foreign talents. With a reduction of expatriate hiring and housing allowance by companies, rental compression is likely to persist.

Top 5 Rental Yield Projects

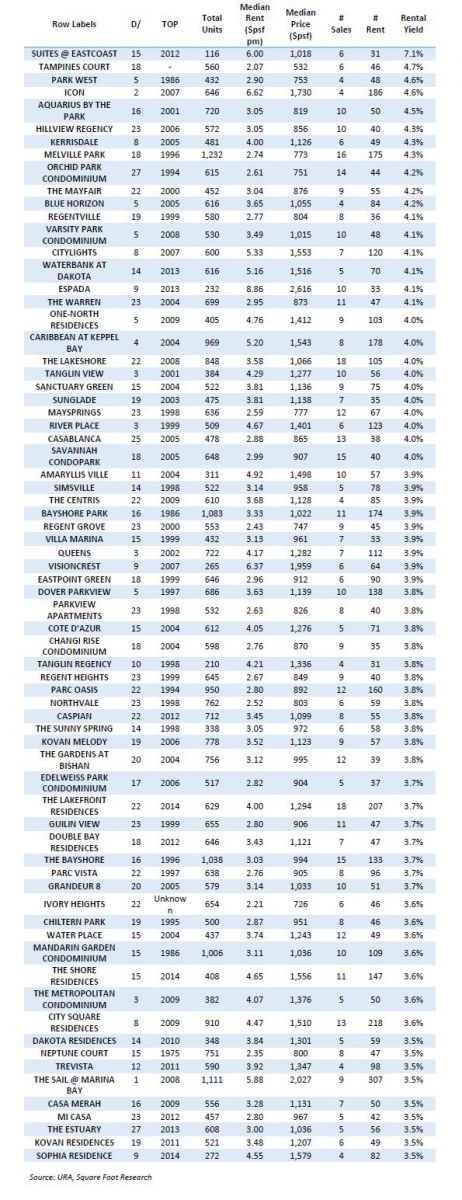

Ranked by rental yield, these are the top 5 developments with at least 30 rental contracts and 4 sales transactions recorded in the past 2 quarters (2Q14 and 3Q14).

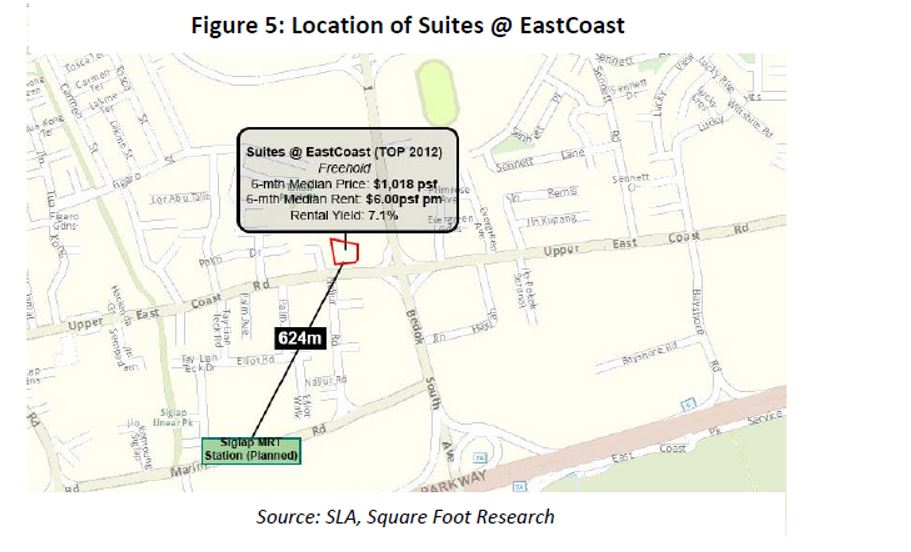

1. SUITES @ EASTCOAST

Topping the chart with a median rental yield of 7.1% is this fairly new freehold development located near East Coast Park in district 15. Completed in 2012, Suites @ Eastcoast consists of 116 units of which 57% are shoebox units (unit area below 500 sqft). A total of 6 sales and 31 rental contracts were transacted in the last 2 quarters with a median rent and price of $6.00 psf pm and $1,018 psf. With the construction of the Thomson-East Coast Line, Suites @ East Coast will stand to benefit from the upcoming Siglap MRT Station, slated to be completed in 2023.

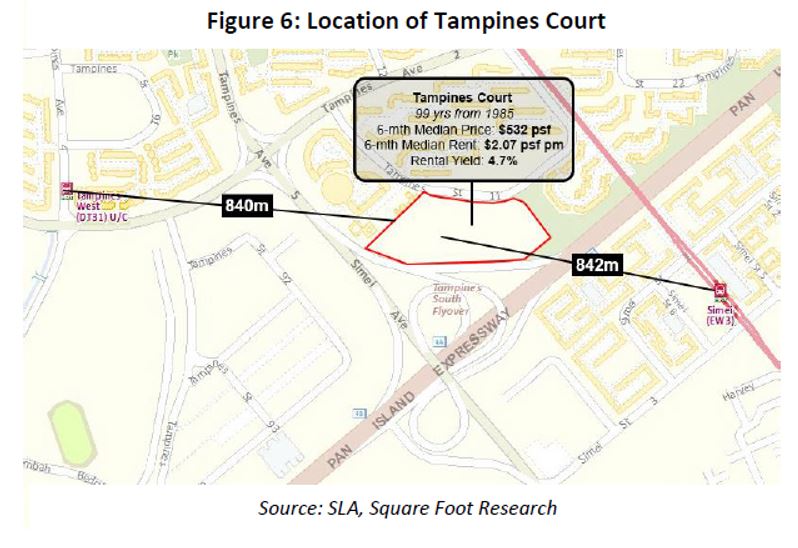

2. TAMPINES COURT

Privatised in 2002, the exact completion date of this development is unknown although we do know its 101-year tenure begin in 1985. Comprising 560 spacious units ranging from 1,300 sqft onwards, this old development has braved through a total of 2 failed en-bloc attempts, one in 2006 and the other in 2011. Tampines Court is located in the outskirt at district 18. Located near industrial buildings which may be the source of demand for rental units in the vicinity, Tampines Court has recorded 46 rental contracts and 6 sales transactions with a median price of $2.07 psf pm and $532psf in the past 2 quarters. Coming in second is Tampines Court at a median rental yield of 4.7%.

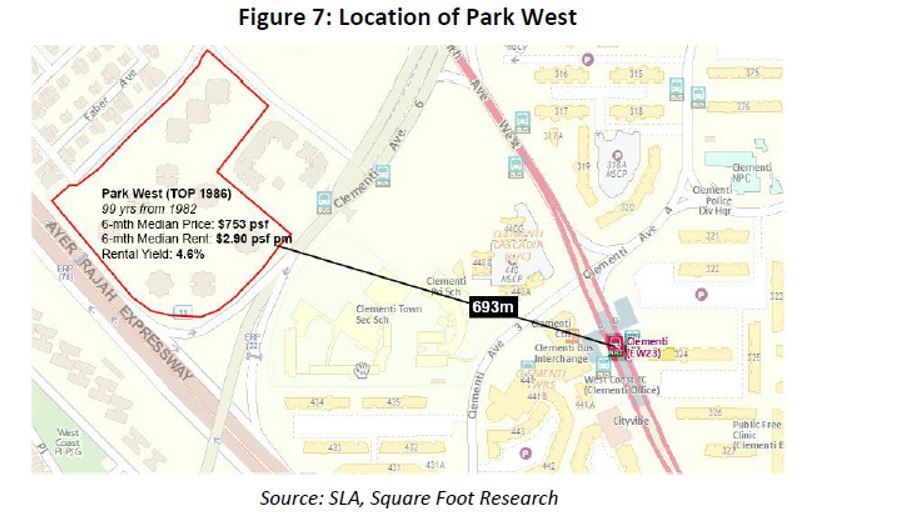

3. PARK WEST

Also situated nearby industrial development, Park West rented out a 48 of its 432 units in the past 2 quarters at a median rent of $2.90 psf pm. A total of 4 sales transactions were recorded during the same period at a median price of $753 psf. This 99-year tenure development was completed in 1986 and is currently one of the oldest and most inexpensive development available in the vicinity. Park West ranks third with a median rental yield of 4.62%.

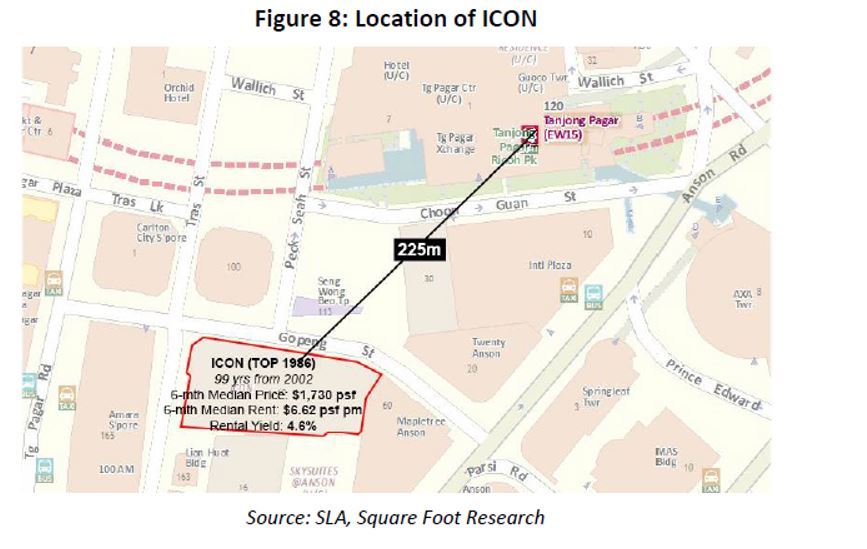

4. ICON

Coming in fourth is Icon, a development located in CCR, Downtown Core, and is just 225m away from Tanjong Pagar MRT station. Developed by Far East Organization, this development comprises a total of 616 units and was completed in 2007. A total of 380 rental contracts, representing 58% of its total units, were recorded in a 12-month period from 4Q13 to 3Q14. The median rent and median price from 186 rental contracts and 4 sales transactions recorded in the past 2 quarters is $6.62 psf pm and $1,730 psf. Icon comes in fourth with a rental yield of 4.6%.

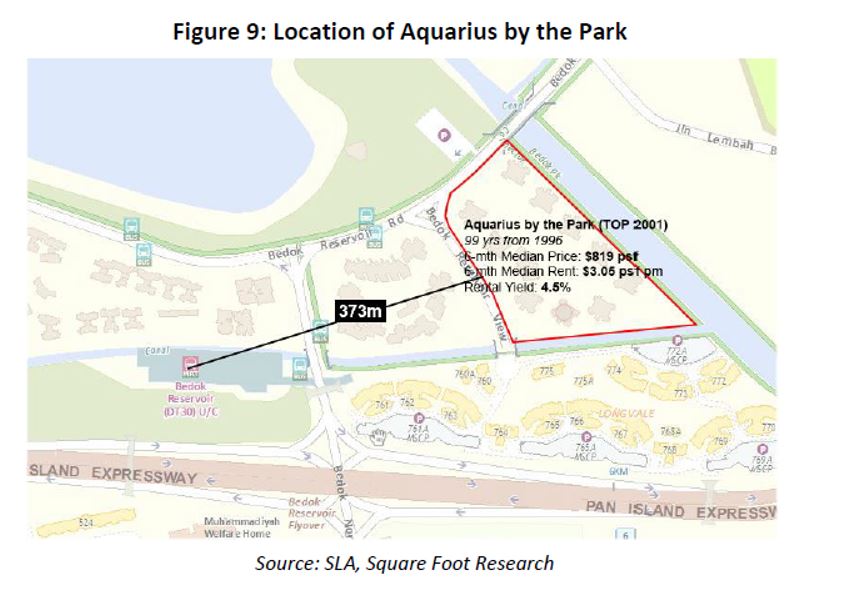

5. AQUARIUS BY THE PARK

Situated in district 16 just beside Bedok Reservoir, Aquarius by the Park will soon benefit from the Bedok Reservoir Station (DTL), which is slated to be completed in 2017. Comprising 720 units, this development was completed in 2001 and saw a total of 50 rental contracts and 10 sales transactions in the past 2 quarters with median rent and median price of $3.05 psf pm and $819 psf. Aquarius by the Park ranks fifth with a rental yield of 4.5%.

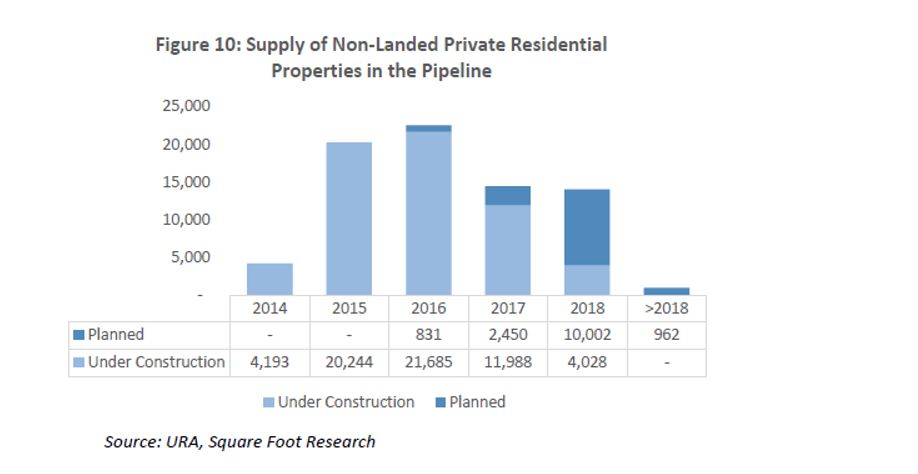

CONDO & APARTMENT - SUPPLY IN THE PIPELINE

CONDO & APARTMENT – 3Q14 MEDIAN TRANSACTION PRICE

3Q14 MEDIAN RENTAL YIELD BY PLANNING AREA

RENTAL YIELD OF 3.5% AND ABOVE

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search