Asia Pacific corporate real estate holds steady amid global volatility and shifting US trade policies

Sweeping policy changes during the first 100 days of US President Donald Trump's second term — particularly in trade, tariffs, and deregulation — have introduced significant volatility across global markets (Photo: Cushman & Wakefield report)

The Asia Pacific (APAC) property sector entered 2025 on solid footing, supported by healthy occupier demand and a recovery in investment transaction activity.

However, sweeping policy changes during the first 100 days of US President Donald Trump's second term — particularly in trade, tariffs, and deregulation — have introduced significant volatility across global markets.

Amid this flurry of changes, the dominant theme in the marketplace has been uncertainty. The turbulence is expected to dampen growth as businesses adopt a more cautious, wait-and-see approach to decision-making.

Brown: The odds of a US recession are rising, and short-term stagflation — slowing growth coupled with sticky inflation — has become the consensus outlook for 2025 (Photo: Cushman & Wakefield)

Still, according to Cushman & Wakefield's latest report, Trump 2.0: The First 100 Days—Implications for the APAC Economy & Property Markets, APAC's economy and property markets are showing resilience, underpinned by domestic demand and strong market fundamentals.

The odds of a US recession are rising, and short-term stagflation — slowing growth coupled with sticky inflation — has become the consensus outlook for 2025, says Dominic Brown, head of international research at Cushman & Wakefield (C&W).

While domestic consumption is expected to support regional growth, APAC will inevitably feel the effects of a global slowdown. "Expected stronger growth in the U.S. in 2026 could provide tailwinds for the Asia Pacific region," Brown adds.

Among sectors, manufacturing — especially exporters to the US — will bear the brunt of new tariffs.

Leasing and investment activity may temporarily slow

C&W anticipates a near-term slowdown in leasing and investment activity, primarily due to delayed decision-making amid uncertainty. However, historical trends suggest that APAC tends to rebound quickly once confidence returns and conditions stabilise.

The outlook for construction costs remains mixed, which could encourage a "risk-off" stance and curb new supply until clearer signals emerge. In this environment, existing assets are likely to benefit.

Most central banks began 2025 with a more accommodative monetary stance, a trend expected to continue. Despite the riskier environment, property values are generally expected to remain resilient and trend higher once market confidence improves. In the near term, however, wider credit spreads may emerge.

Impact on Corporate Real Estate (CRE)

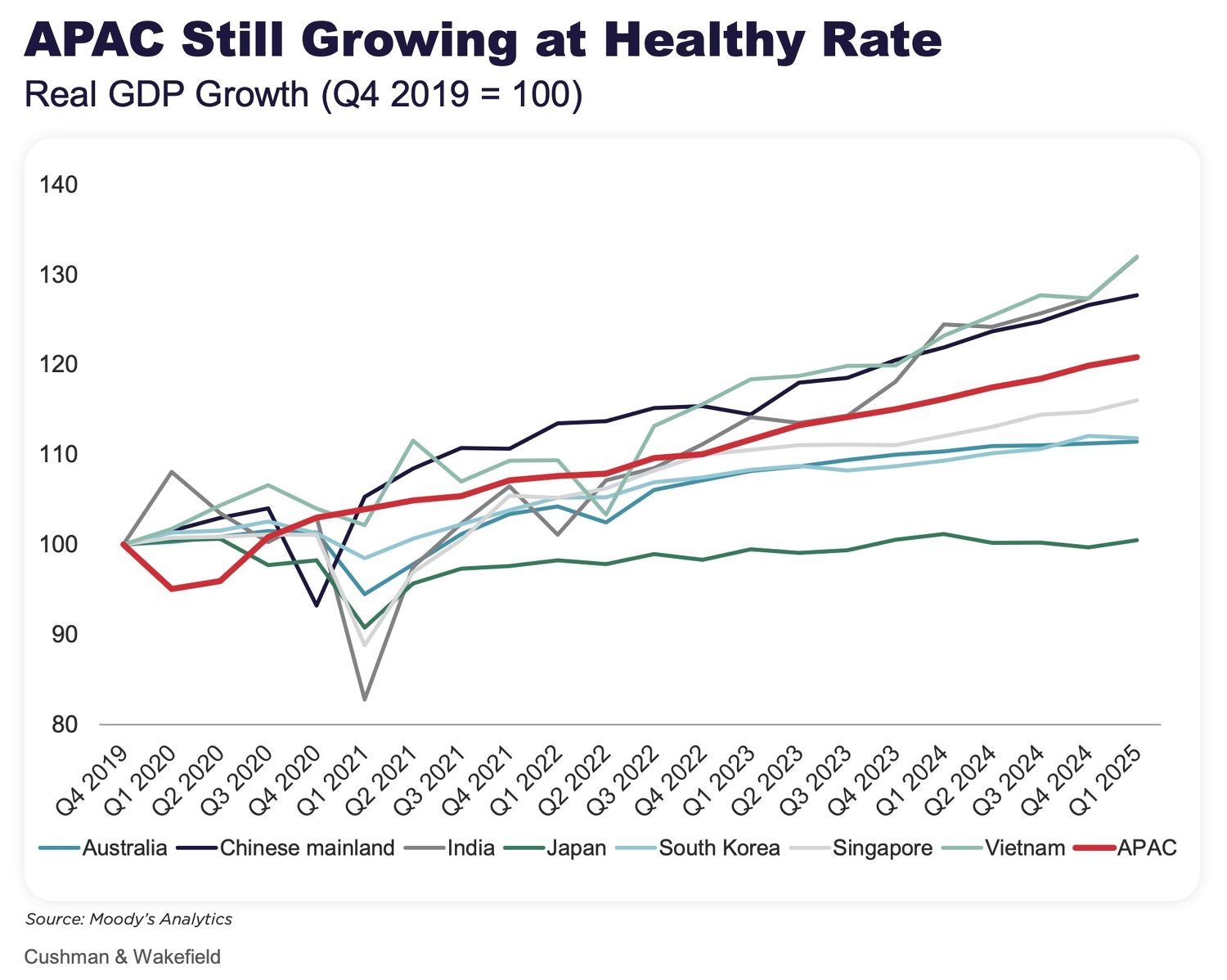

The APAC regional economy has been growing at a healthy rate of 4% over recent years, with India and Southeast Asia leading the charge.

Over the past five years, the region has added nearly 68 million jobs, of which over 16 million are office-based. This has supported sustained demand for office space, while a growing middle class continues to fuel the manufacturing and retail sectors through rising consumption.

Despite global volatility, GDP growth across APAC held firm in 1Q2025 at 3.9%, comparable to pre-Trump-era levels.

While stock market swings may not directly affect real estate fundamentals, the wealth effect plays a significant role. When equity markets rise, consumers feel wealthier and spend more, boosting corporate earnings and employment. The reverse, however, can dampen consumer confidence and, eventually, real estate demand.

Policy uncertainty sapping confidence

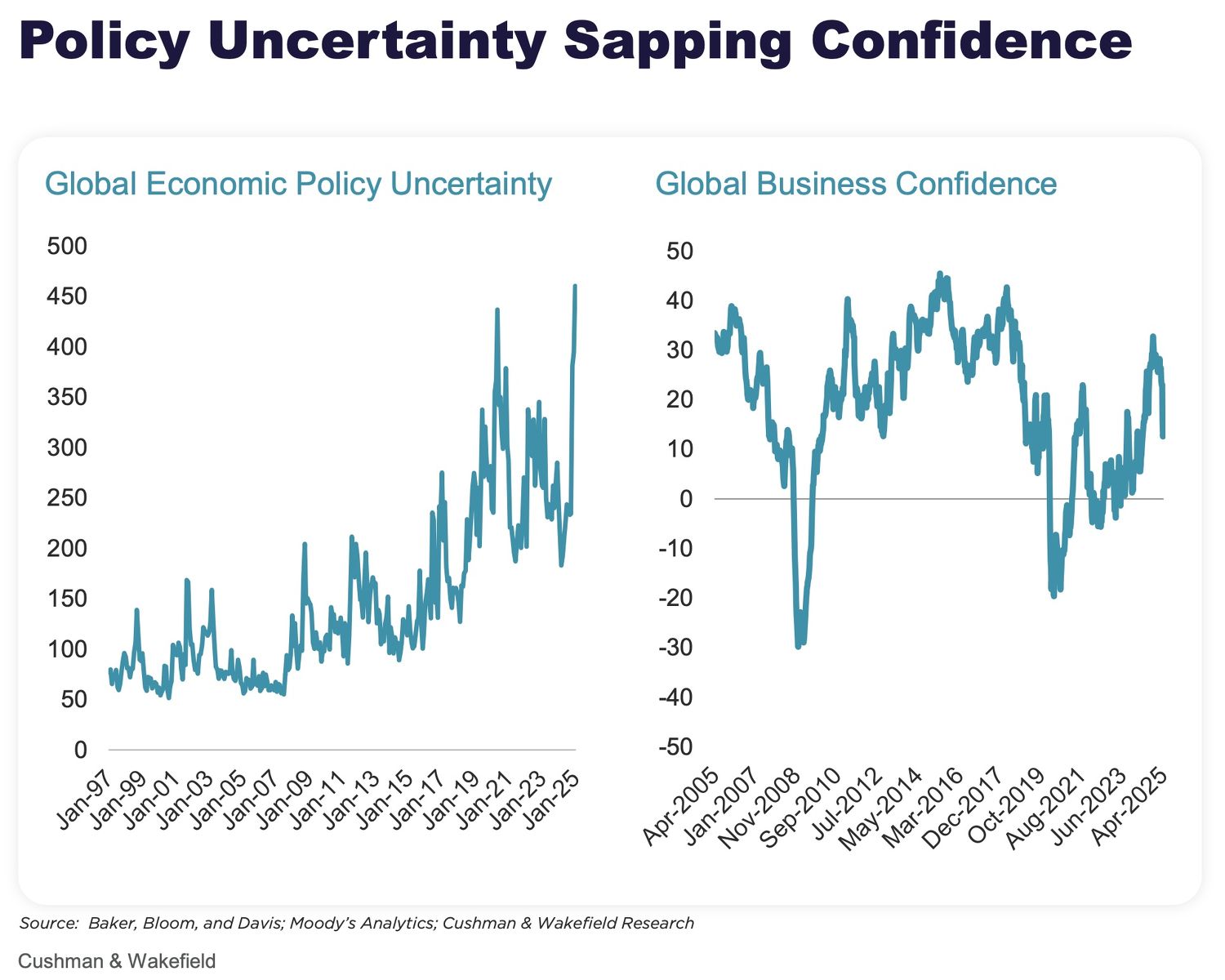

Trump's on-again, off-again tariff policies have led to one of the highest levels of policy uncertainty in recent memory.

Periods of elevated policy uncertainty typically correlate with falling business confidence, resulting in delayed hiring and capital investment. In such scenarios, businesses often pause until there's greater clarity on policy direction.

The longer this uncertainty persists, the more damage it inflicts on regional and global growth. Consumption and investment — key pillars of GDP — are especially vulnerable.

The same holds true for the CRE sector, where both occupiers and investors may defer decision-making until visibility improves.

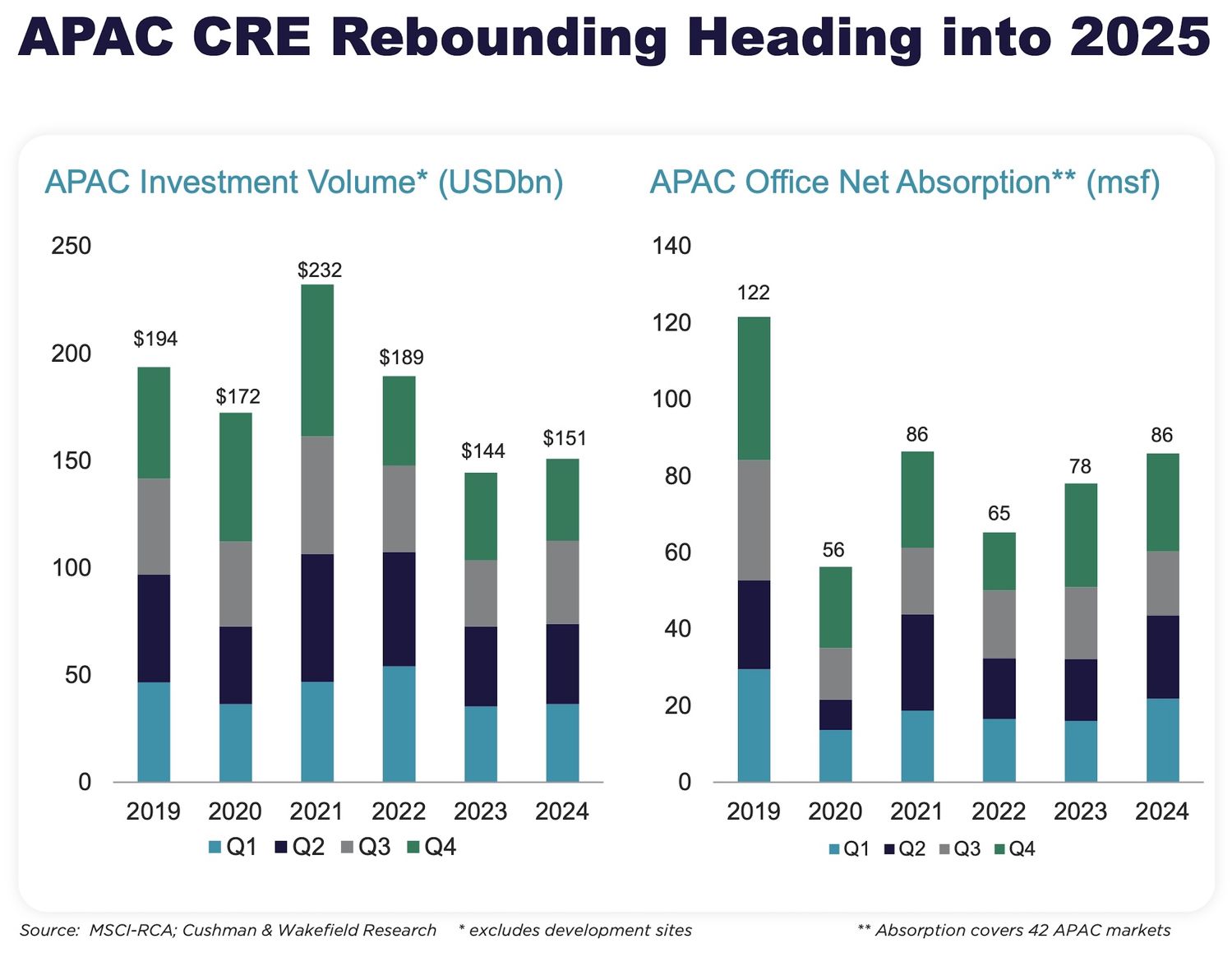

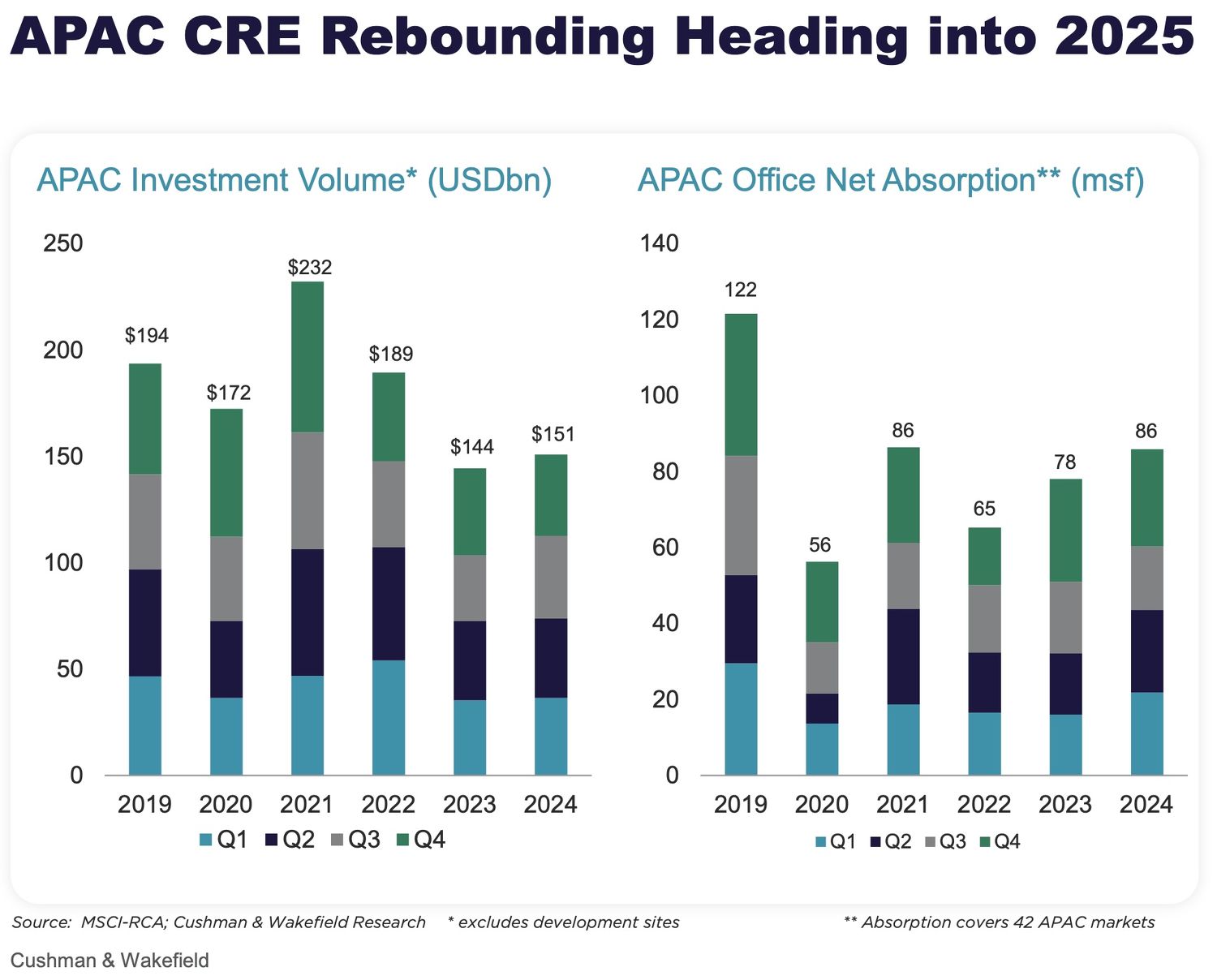

In 2024, as interest rate cuts started to occur, first in Europe and the US, and then in APAC, investor appetite increased. Investment volumes in APAC hit a trough around the middle of 2024 and gradually trended higher. In addition, pricing has stabilised across much of the region.

Occupier demand in the region has been stronger, headlined by India, with contributions from most of the region. Consequently, as of the end of 4Q2024, more than 370 million sq ft of office space is occupied in APAC.

Rising uncertainty is the largest downside risk in the near term, which may delay occupier and investor decision-making. However, the fundamentals remain resilient so far.

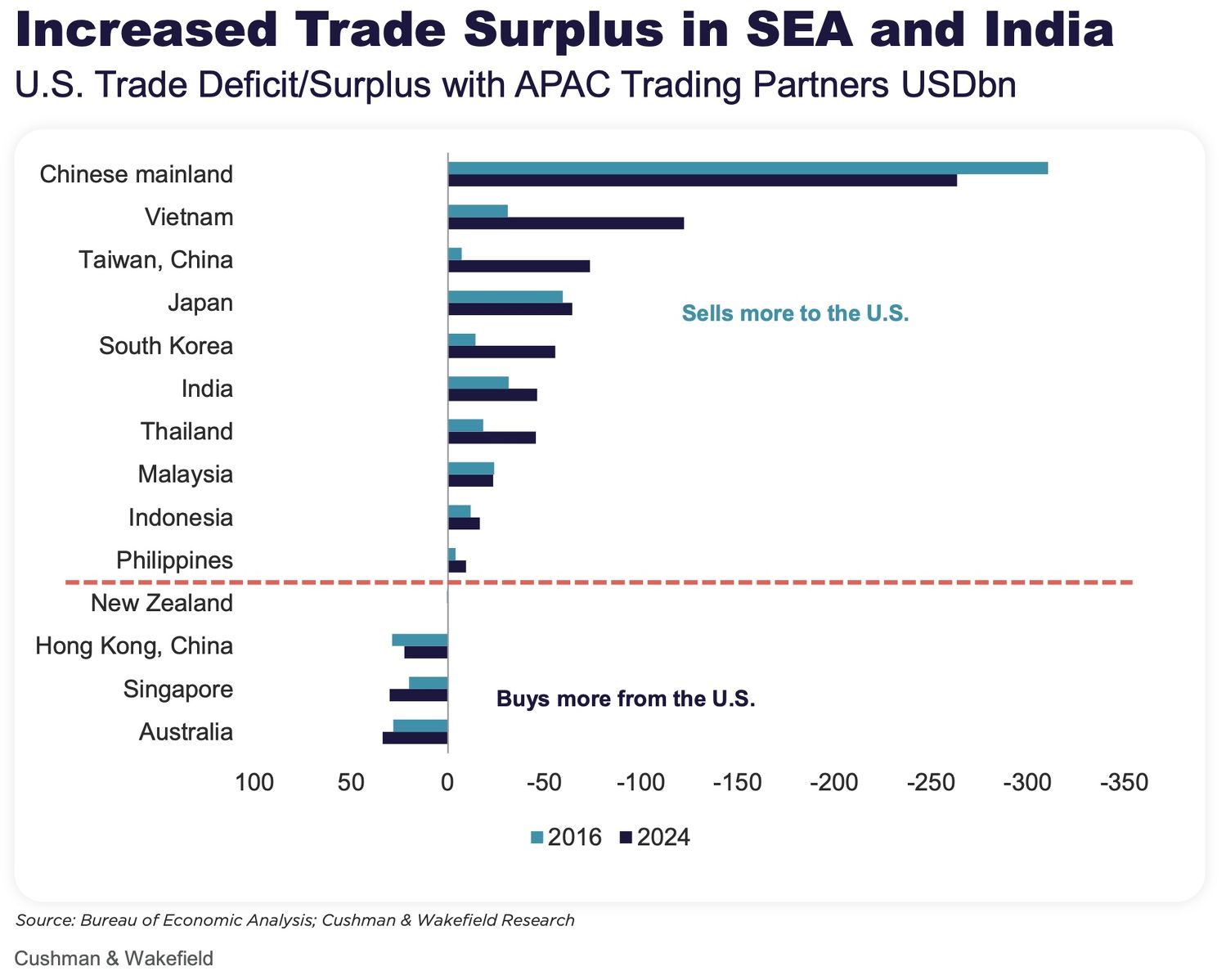

Increased trade surplus in Southeast Asia and India

Trade tariffs imposed on China during the first Trump administration gave rise to the "China Plus One" manufacturing strategy, accelerating industrial production across the APAC region.

The primary beneficiaries of this shift have been India and key Southeast Asian (SEA) markets. Over the past decade, these economies have seen a significant improvement in their terms of trade with the US, with most recording increased trade surpluses.

Meanwhile, strong global demand for semiconductors and automobiles has benefited Taiwan, South Korea, and Japan.

Logistics and industrial markets across the region have performed strongly over the past decade — and especially in the past five years. This growth has been characterised by the rapid development of new supply, tight vacancy rates, and robust rental growth.

As of 1Q2025, most industrial markets in APAC remain landlord-friendly.

US trade exposure varies across APAC

Trade with the US remains a critical growth driver for many APAC economies, though the degree of exposure varies significantly by market.

For example, Vietnam is highly dependent on US trade, making it more vulnerable to any slowdown.

In contrast, markets such as mainland China and India — despite high absolute trade volumes with the US — are less reliant on it for GDP growth. China benefits from broader global trade networks, while India's growth is increasingly driven by domestic consumption.

These variations in trade and consumption patterns will shape the outlook for industrial space demand. A key takeaway: a slowdown in US trade doesn't necessarily translate to weaker industrial real estate demand in all markets.

The current tariff environment remains highly fluid. While a general 10% blanket tariff exists globally, additional tariffs have been levied on specific goods and countries. Simultaneously, some exemptions are still in place.

Therefore, understanding a market's exposure to US trade and the nature of traded goods is essential to gauge the potential impact on the broader economy and industrial real estate. These two factors must be assessed together, not in isolation, and developments in tariff policy should be closely monitored.

US direct investment into APAC

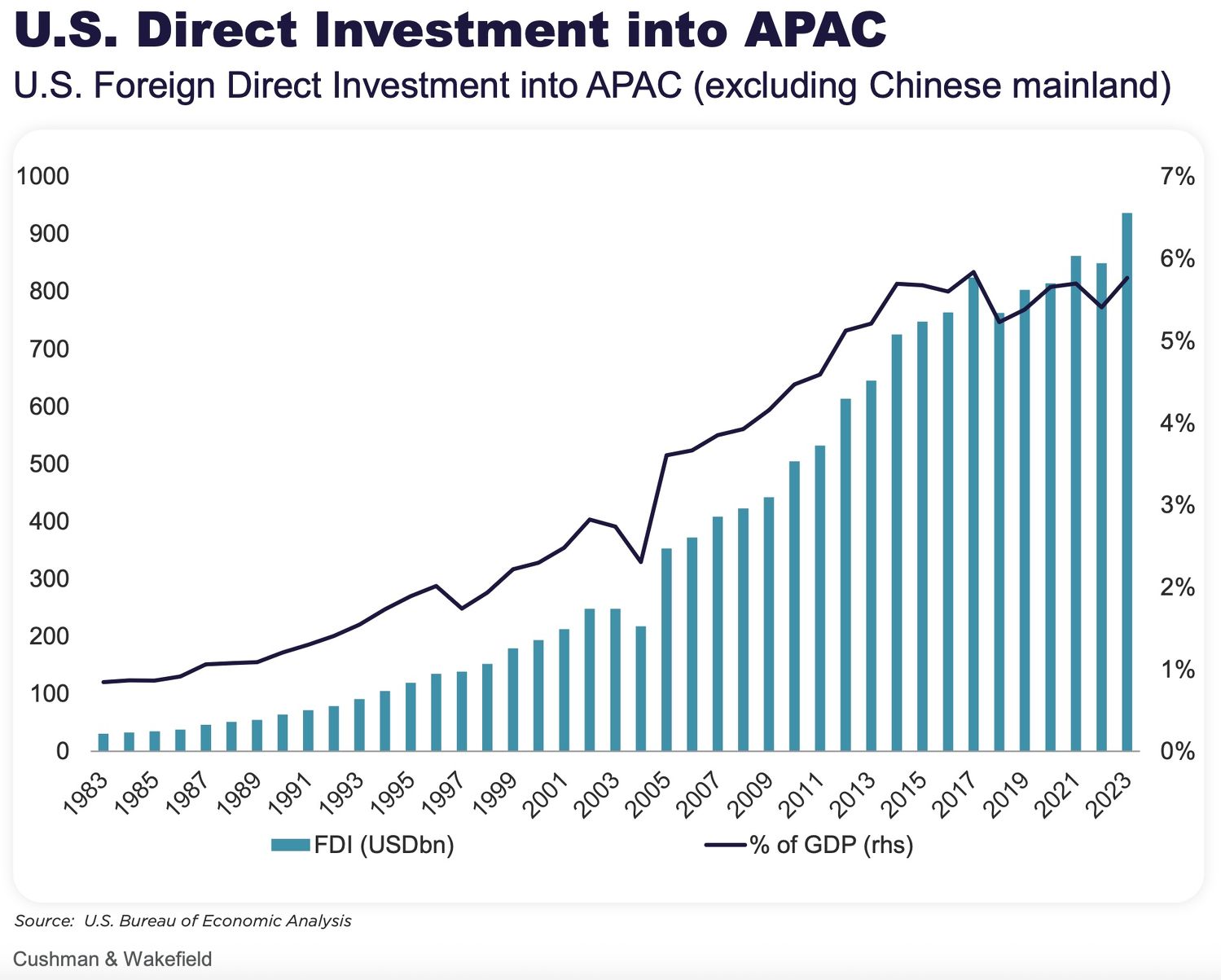

Beyond trade, US direct investment is another critical economic link to the APAC region.

Over the decades, many US-headquartered firms have expanded their presence in Asia. US direct investment in the region has risen from just 1% in the early 1980s to 6% in 2024 — from US$27 billion to over US$935 billion in absolute terms.

These US businesses support extensive employment across APAC and utilise various types of real estate space across the region. Thus, the health of the US economy and corporate balance sheets will remain key factors to watch.

Scope for further rate cuts

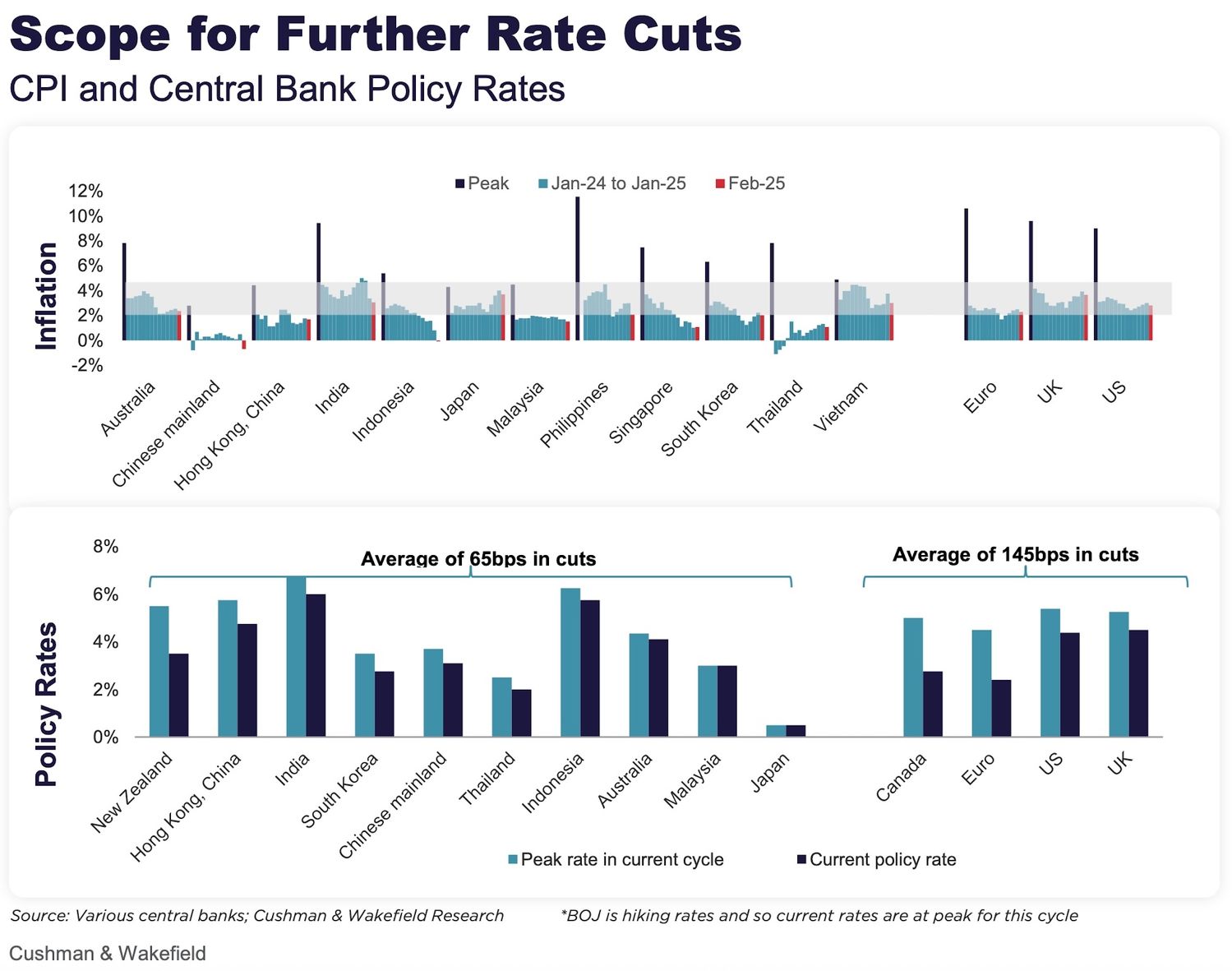

Inflation emerged later in the APAC region compared to other parts of the world and continues to trend downward, with little current evidence of renewed inflationary pressures.

As a result, APAC central banks have cut interest rates by an average of 65 basis points so far—less than the 185 basis points in Europe and 100 basis points in the US Within the region, variation exists: the Reserve Bank of New Zealand has cut rates by 200 basis points amid recessionary conditions, while Bank Negara Malaysia has yet to move, and the Bank of Japan is hiking rates as part of its monetary policy normalisation.

Central banks in APAC retain scope for further rate cuts to support domestic economies, although they remain watchful of foreign exchange pressures.

Such downward movements in interest rates could provide stronger support for the investment case in CRE.

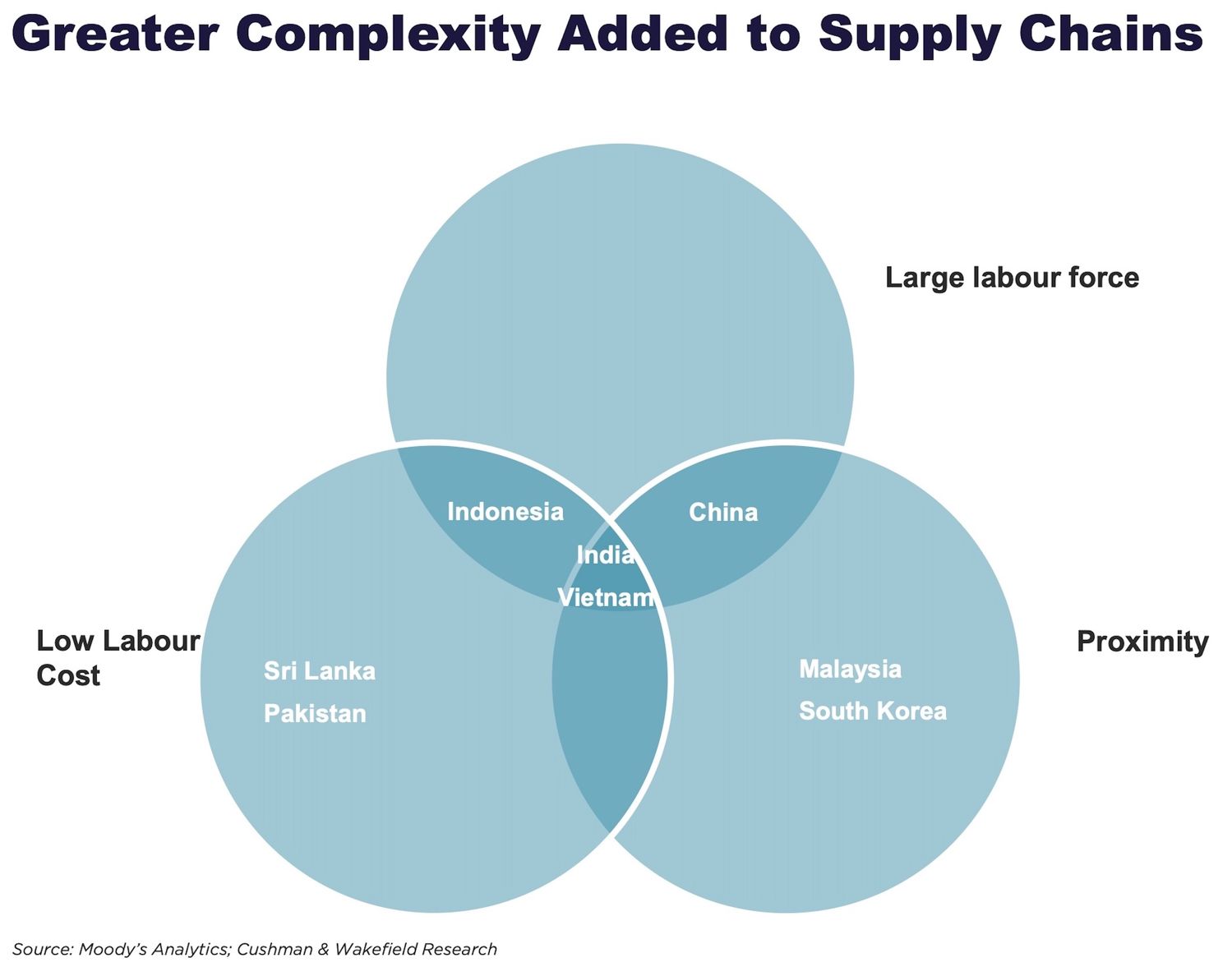

Greater complexity added to supply chains

Supply chains were reconfigured during and after the first Trump administration—partly in response to ongoing tariffs on Chinese goods and partly due to broader structural shifts.

China's pivot toward higher-value production, alongside lower labour and real estate costs in India and Southeast Asia, has driven rapid growth in industrial estates across these regions.

While blanket tariffs—like the current 10%—do little to affect the relative attractiveness of these markets, more selective tariffs targeting specific goods or countries could lead manufacturers to reassess their supply chain configurations for possible optimisation. Such changes are unlikely to happen in the near term.

Instead, the fluid trade environment is more likely to cause decision-making delays, dampening overall demand for industrial space.

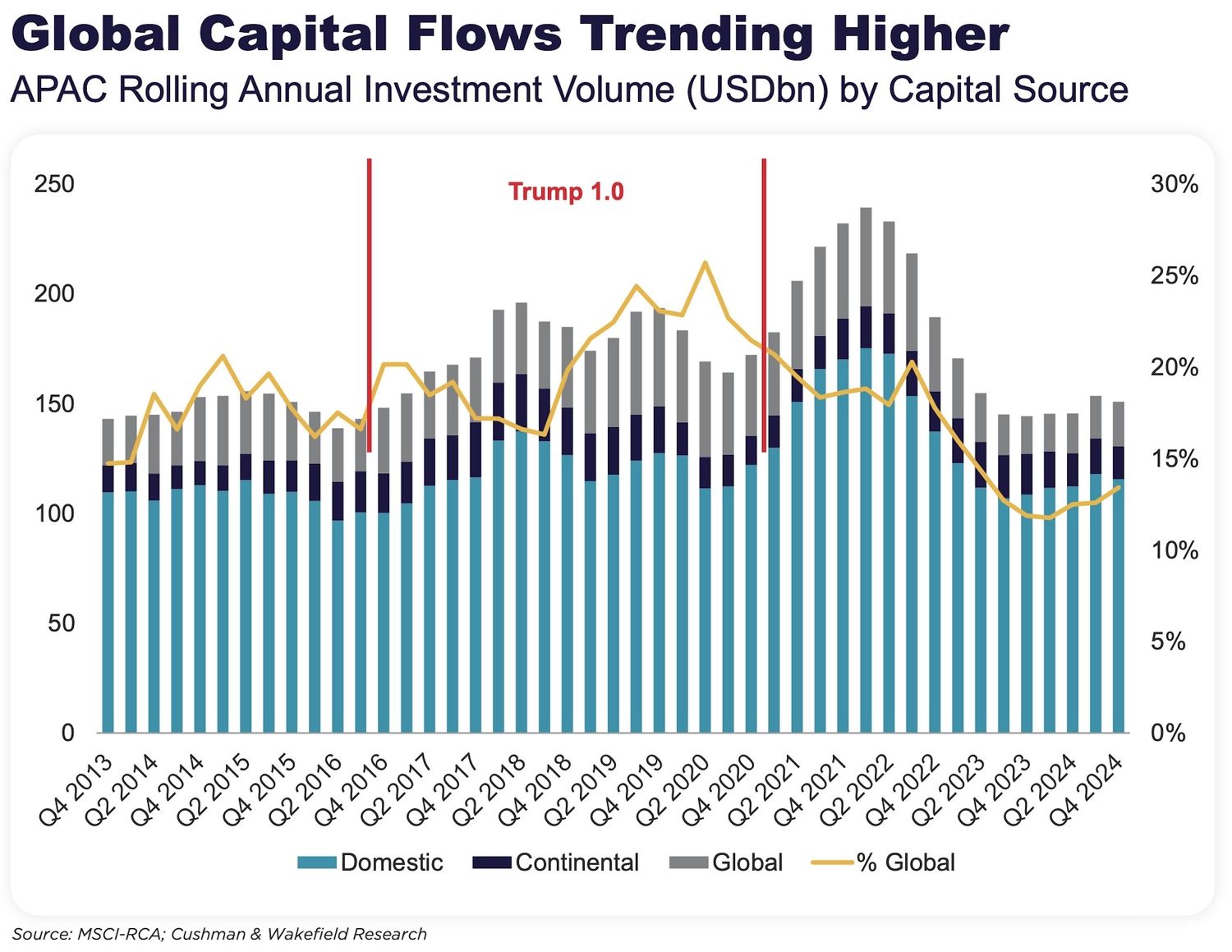

Global capital flows trending higher

Global capital inflows into APAC CRE rose from around 15% to nearly 25% of total investment during Trump's first term. Investment volumes increased from US$25 billion to US$45 billion during that period.

Following a recent pullback, early signs now point to a recovery. Over the past four consecutive quarters, global investment into APAC — led by US-based investors and supported by a strong US dollar — has risen in both absolute value and proportion of total global flows.

Given prevailing uncertainty, investors may increasingly favour CRE's more stable, income-producing characteristics, though they must navigate a higher risk premium.

Target markets and sectors will likely include those with limited exposure to global macroeconomic headwinds and "through-the-cycle" resilience. Examples include multifamily residential assets in Japan, logistics and industrial space in Australia, and operational data centres. Isolated assets influenced by external shocks may also come to market, presenting opportunistic returns.

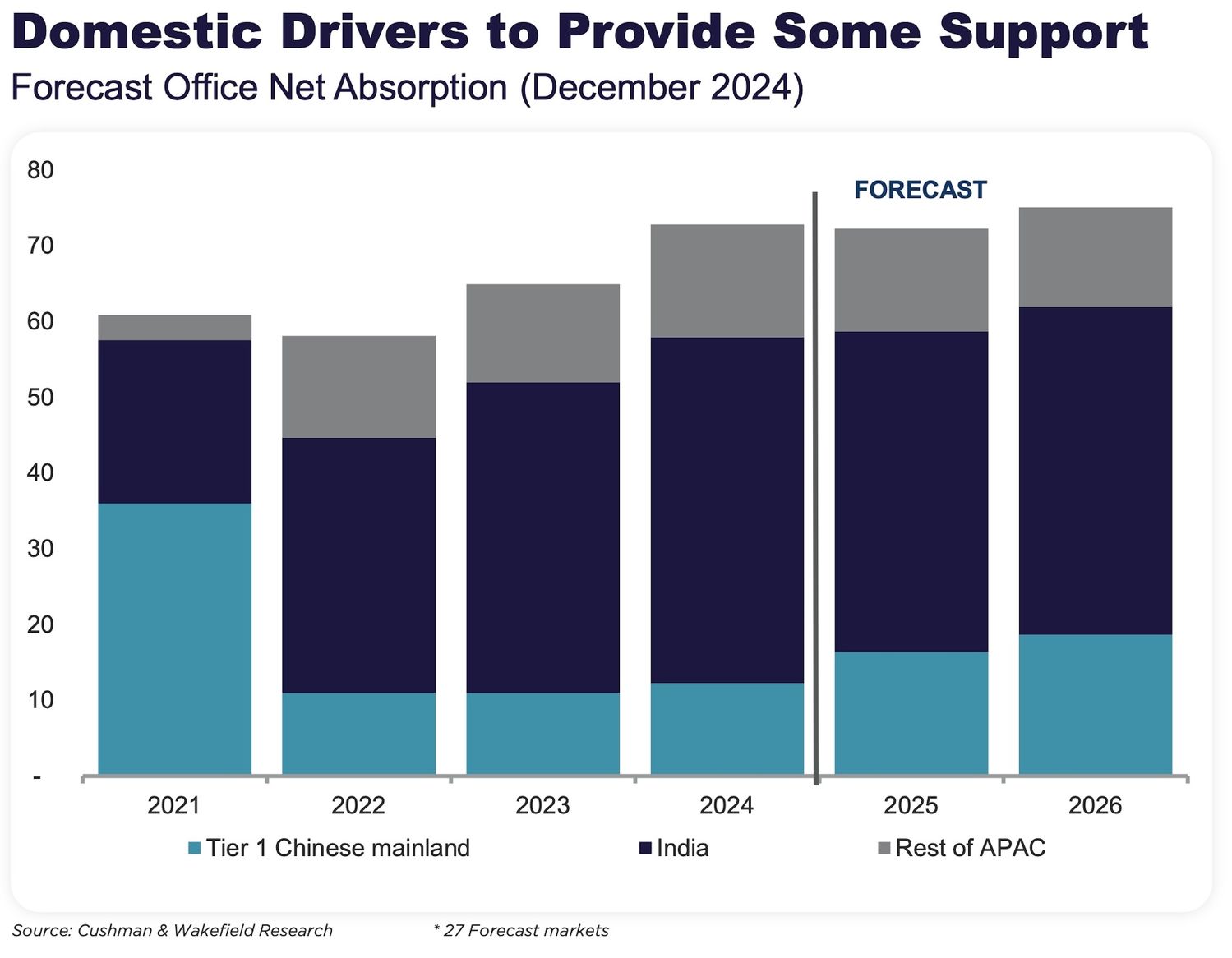

Domestic drivers to provide some support

As with late 2024, the baseline forecast for office demand in 2025 was for a broad continuation of existing trends. Early 1Q2025 data supports this outlook.

However, given ongoing macroeconomic and geopolitical uncertainty, the risks to this forecast for the remainder of the year are skewed to the downside, mainly due to delayed decision-making.

Even so, robust domestic drivers in markets such as India, Indonesia, and the Philippines could help buffer some of this uncertainty. Following a weak 2024, Australia is also poised for stronger economic performance in 2025, potentially supporting occupier demand.

It remains too early to gauge the full impact of recent volatility. The two most likely outcomes are (1) a temporary pause in decision-making or (2) more pronounced adverse effects if uncertainty persists. Either scenario suggests a softer near-term demand outlook.

Nevertheless, past experience shows the region can rebound quickly once conditions stabilise and confidence returns.

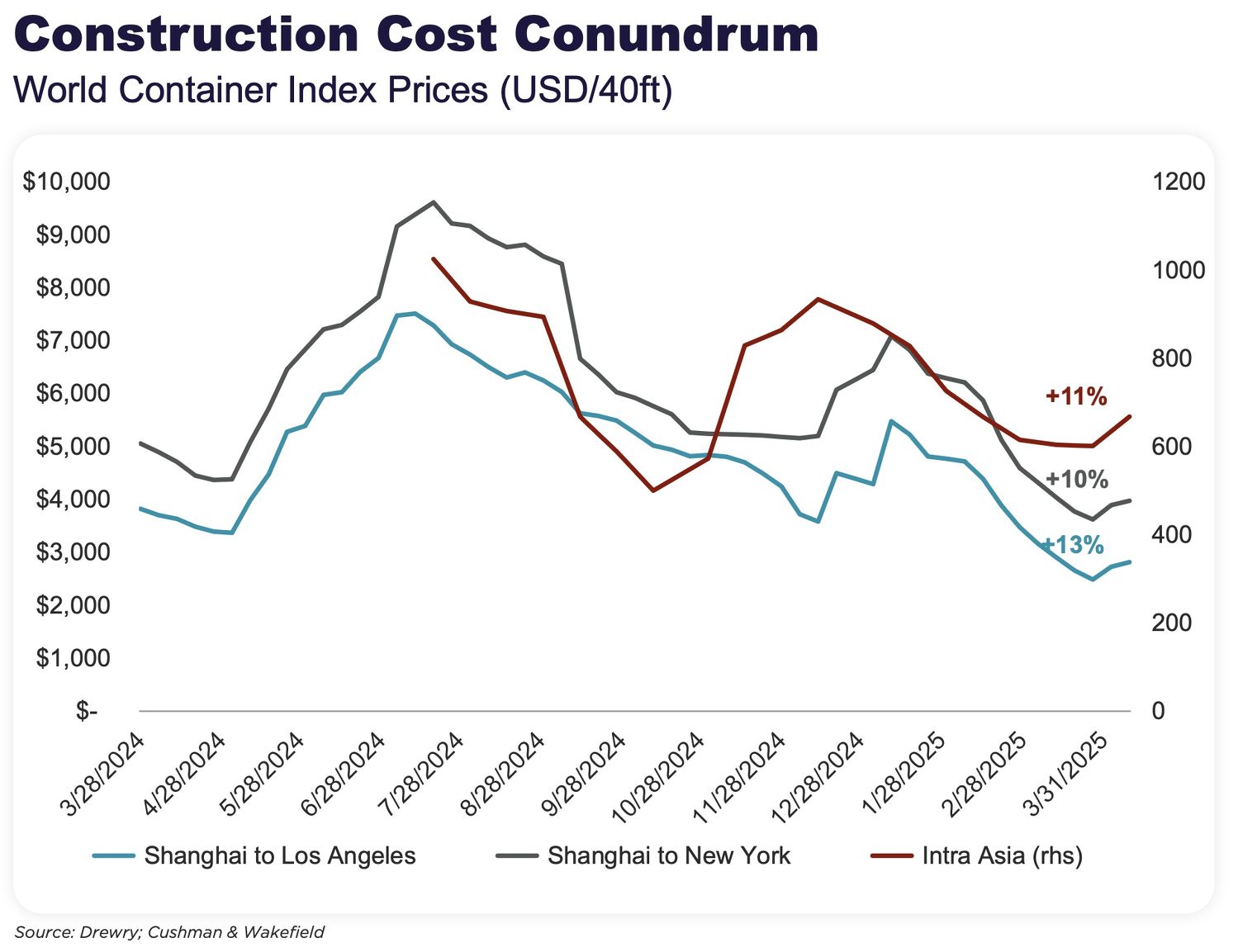

Construction cost conundrum

Steel and aluminium tariffs remain a key focus due to their implications for construction costs.

In the US, rising tariffs on raw materials and labour shortages are putting upward pressure on costs and slowing construction pipelines. This could lead to a short-term oversupply of raw materials until production schedules adjust, potentially pushing prices down. However, rising shipping costs, which are increasing as firms manage near-term inventories, could offset this.

On balance, raw material input costs in APAC may be lower in the near term. However, developers must also factor in other cost elements—such as local labour and land pricing—that play a larger role in determining overall project feasibility.

This issue is especially significant given the more than 230 million sq ft of office space slated for completion in the region by 2026.

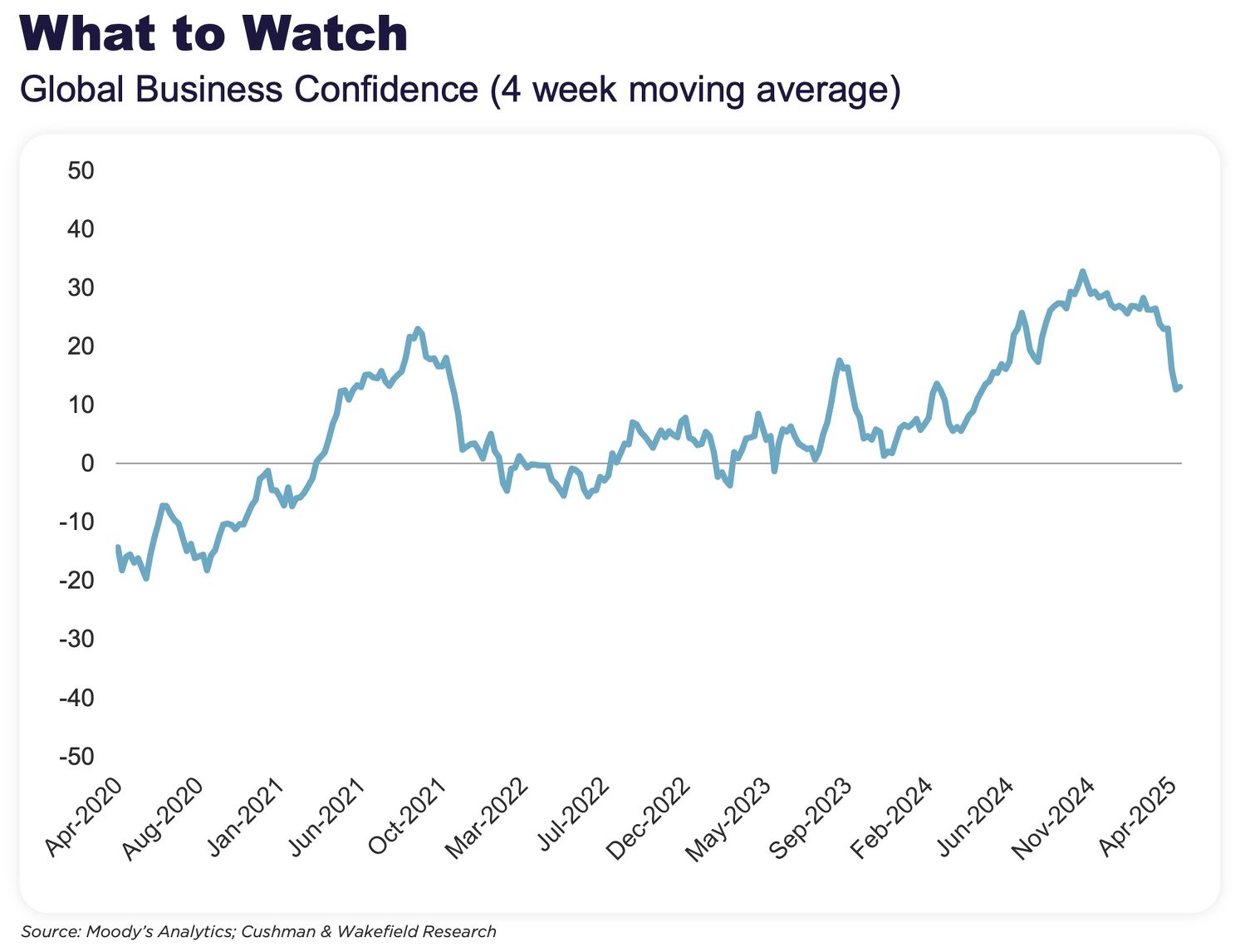

Global business confidence

Among many data points to watch, global business confidence remains a useful overarching indicator.

While volatile in nature, its moving average provides a sense of direction for business sentiment. In recent weeks, that average has trended meaningfully lower.

If this continues, it could signal weakening revenue expectations, reduced capital expenditure, and possibly rising job redundancies.

Ultimately, this would lower demand for CRE and reduce leasing activity.

That said, confidence levels remain well above the lows seen during the pandemic and the downturn associated with aggressive rate hikes. The key question now is how quickly sentiment can rebound and whether businesses will regain optimism in their outlook.

Cushman & Wakefield's report, Trump 2.0: The First 100 Days – Implications for the APAC Economy & Property Markets, was written by head of international research Dr Dominic Brown and chief economist Kevin Thorpe and published on April 30, 2025

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search