Asia Pacific real estate marks turning point with selective value-add opportunities

Mount Fuji and the Shinjuku skyline in Tokyo. Countries like South Korea and Japan also have higher shares of non-investable stock, pointing to opportunities for value creation via modernisation (Photo: Bloomberg)

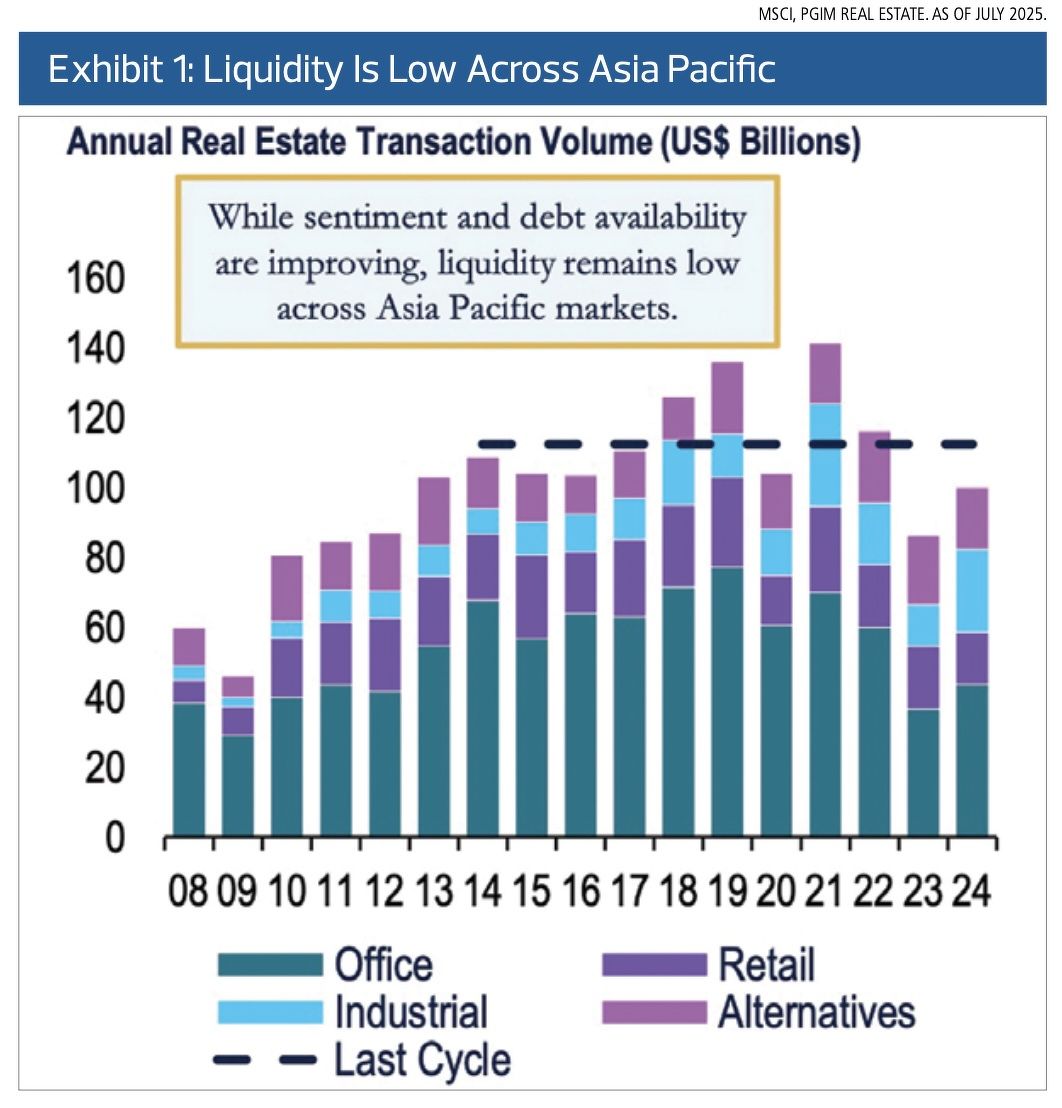

With 2025 marking the turning point for capital values, sentiment toward real estate is improving. However, debt and equity liquidity remain subdued compared to the last cycle (Exhibit 1), says PGIM Real Estate in an investment research report last month.

A drop in values combined with structurally higher interest rates has created a debt funding gap, putting stress on existing capital structures.

For investors, this presents opportunities to selectively acquire assets below valuation and capture immediate upside. Such opportunities are most compelling where assets face cash flow challenges, such as buildings with short lease expiries or those in need of further capital investment.

Looking to invest in overseas properties? Explore projects available for sale around the world

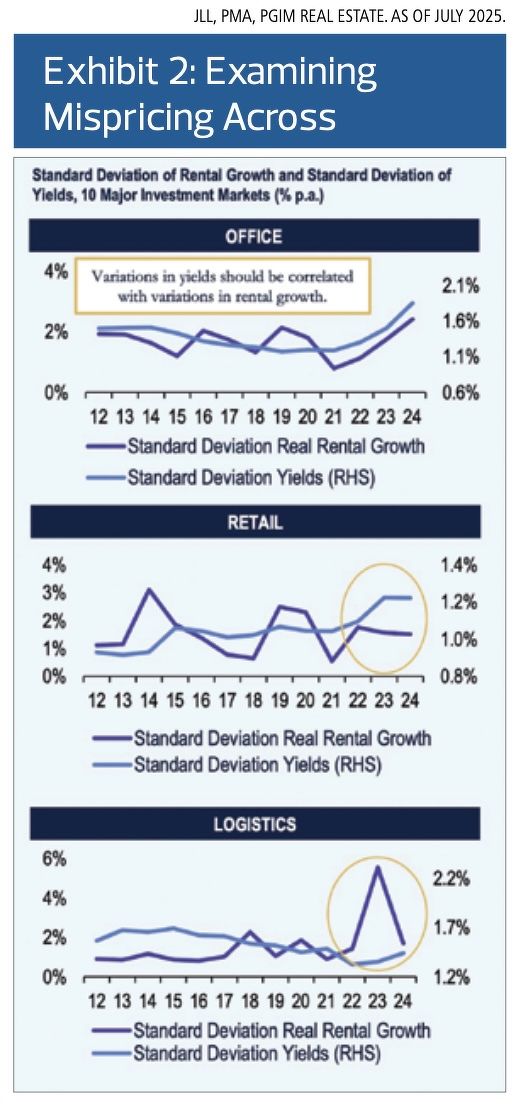

Low liquidity often creates mispricing, reflected in diverging patterns between yields and rental growth. A useful indicator is when the standard deviation of yields across markets does not align with the standard deviation of rental growth.

Recent evidence of mispricing is seen in logistics and retail (Exhibit 2), offering investors the potential to achieve enhanced returns.

The capital shortfall

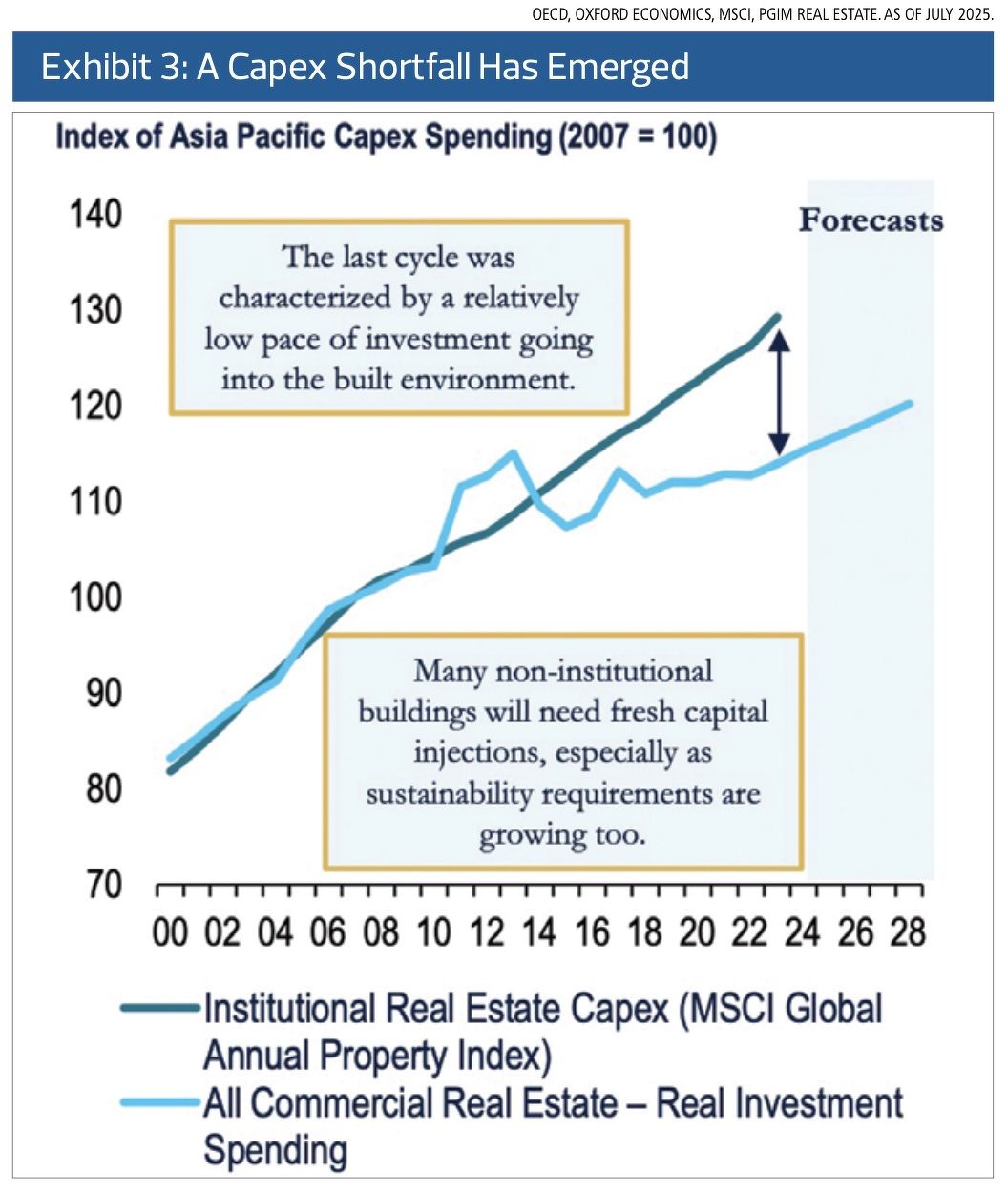

Institutional-quality real estate requires increasing capital expenditure (capex), particularly to meet higher sustainability standards. Yet, over the past decade, non-institutional real estate capex has lagged significantly behind institutional investment (Exhibit 3).

As a result, much of Asia Pacific’s real estate stock, especially those held by smaller owners, will require modernisation and institutionalisation.

With financing harder to access due to higher rates, tighter credit, and ESG requirements, well-capitalised investors with expertise will be favoured.

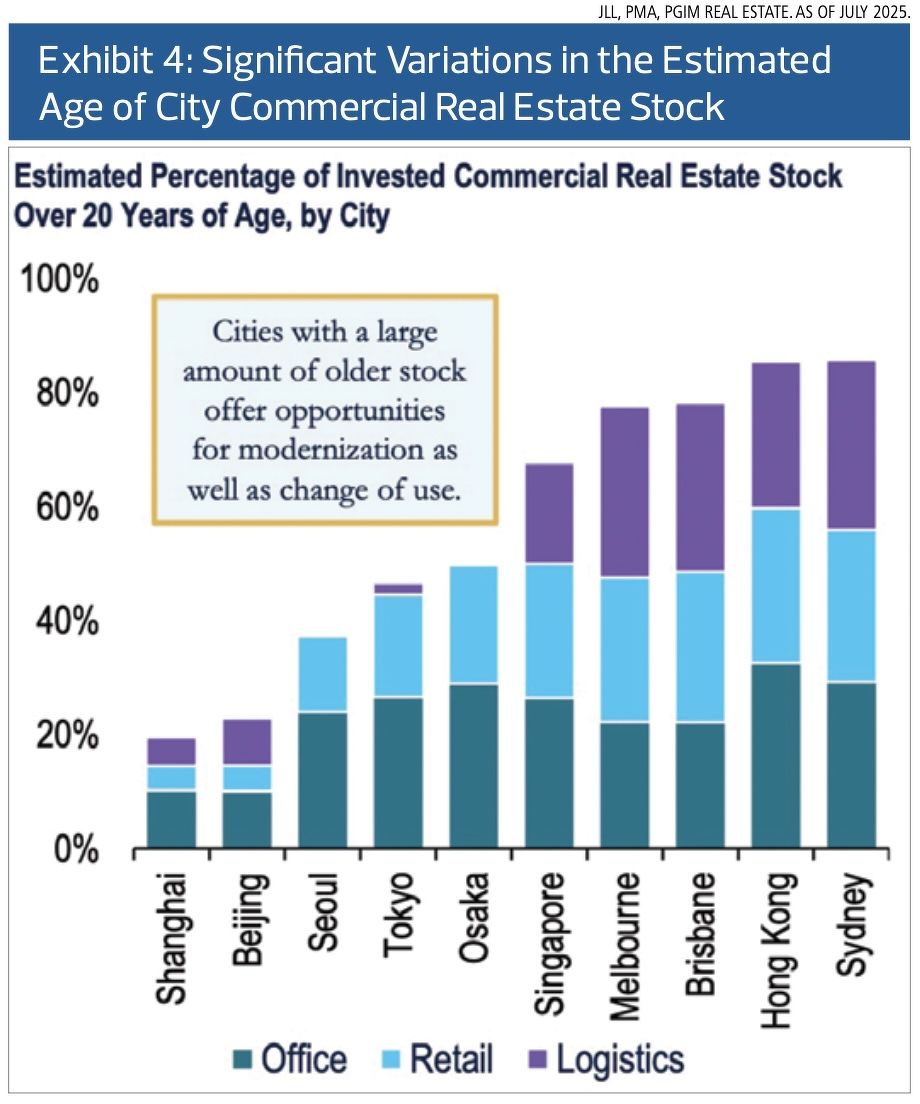

The shortfall in financing presents a substantial opportunity for the coming cycle, particularly as tenants gravitate toward high-quality stock. The extent of opportunity varies by city. Older stock is more prevalent in Hong Kong and Sydney than in Beijing or Shanghai (Exhibit 4).

In Japan, reforms are prompting corporates to divest under-managed real estate assets, while offices and retail present the largest share of older stock, compared to logistics, which is relatively modern.

Supply shortages

New supply has lagged since the global financial crisis. High build costs, tighter access to financing and weak investor sentiment toward development will limit supply growth in the coming years.

While this is rational in weaker segments like suburban office or retail, supply growth is also constrained in high-demand sectors such as housing, CBD offices, data centres, senior living, and hotels.

The resulting shortages will give landlords greater pricing power to drive rental growth.

Expanding the opportunity set

Two shifts are expanding the value-add landscape:

Sectoral diversification — Investment is moving beyond traditional office, retail, and logistics into multifamily housing (still underdeveloped outside Japan), hotels, student accommodation, co-living, senior living, and co-location data centres. The share of investment in operational sectors rose to 17% in 2024, up from 7% in 2014.

Geographic expansion — Institutionalisation continues in Australia and Japan, while second-tier markets such as Nagoya, Fukuoka and Perth are becoming more liquid.

Countries like South Korea and Japan also have higher shares of non-investable stock, pointing to opportunities for value creation via modernisation.

Current challenges

Elevated interest rates: Short-term rates are falling, but long-term rates remain well above last-cycle averages and are forecast to stay there. This reduces the scope for yield compression, meaning returns will be driven by rental growth and cash flow resilience rather than leverage.

Limited returns from traditional assets: Core assets are expected to deliver only around 2% annual returns, which historically translates into modest non-core performance. Achieving higher value-add returns will require investing beyond traditional assets and into operational sectors, as well as repositioning under-managed stock.

Value-add investment approaches

Five main strategies will shape value-add investing in the next cycle, each with distinct risk-return profiles. A balanced portfolio is likely to blend them.

Operational platforms are central to driving rental growth, whether in senior living, hotels, logistics, or offices with flex space offerings.

Development strategies will focus on sectors with strong structural demand — living, logistics, and data centres.

Mispricing persists in offices, logistics, retail and hotels, especially those still adjusting post-pandemic.

Active asset management will drive returns in traditional sectors where operational platforms are less involved.

Institutionalisation plays, such as upgrading privately held living assets or family-owned hotels, offer substantial opportunities.

Target markets: Countries and cities

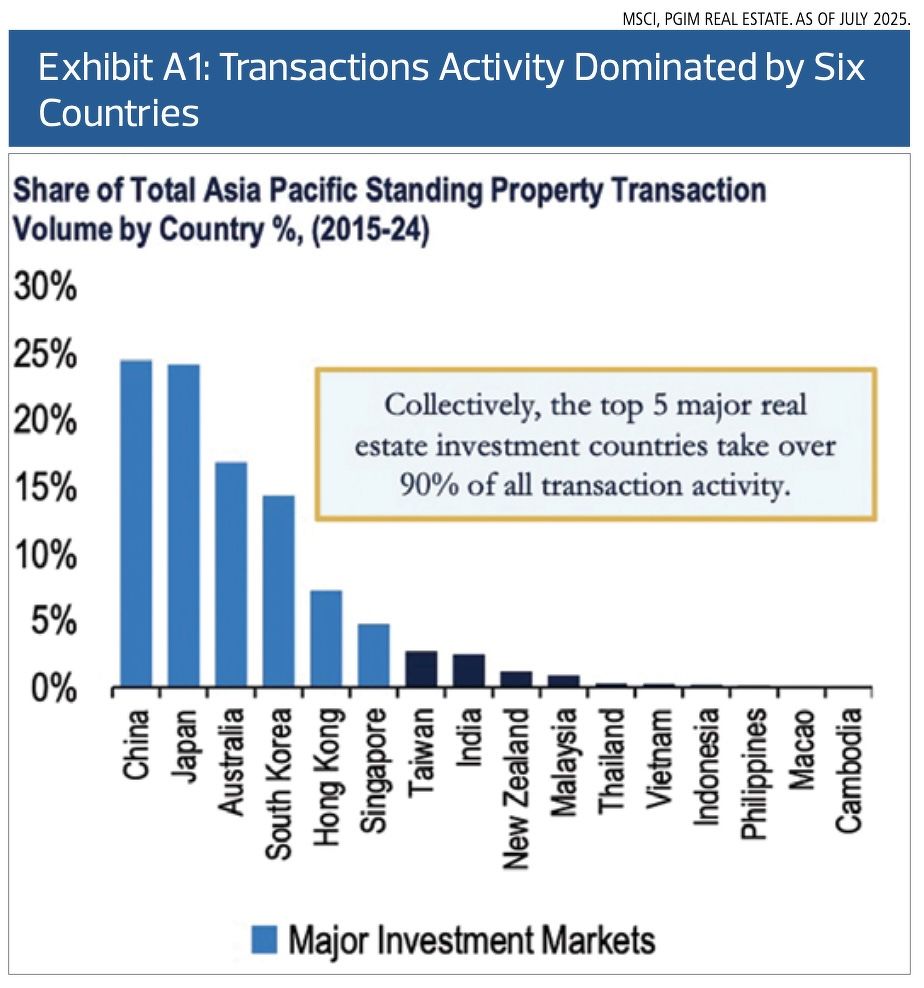

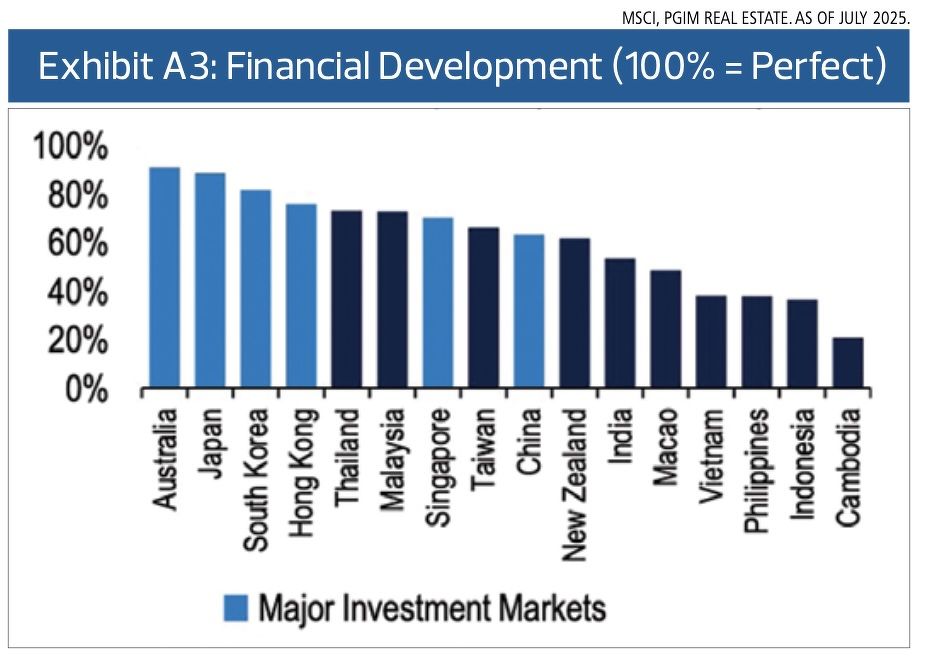

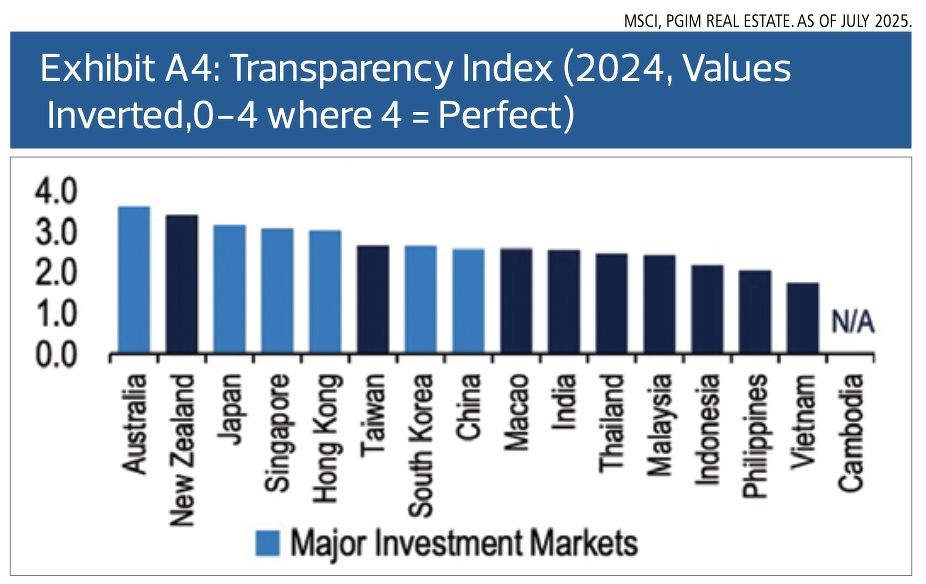

Institutional activity remains concentrated. Since 2008, five countries have accounted for nearly 90% of transactions (Exhibit A1). These markets also rank highest on investment size, financial development, and transparency (Exhibits A2–A4).

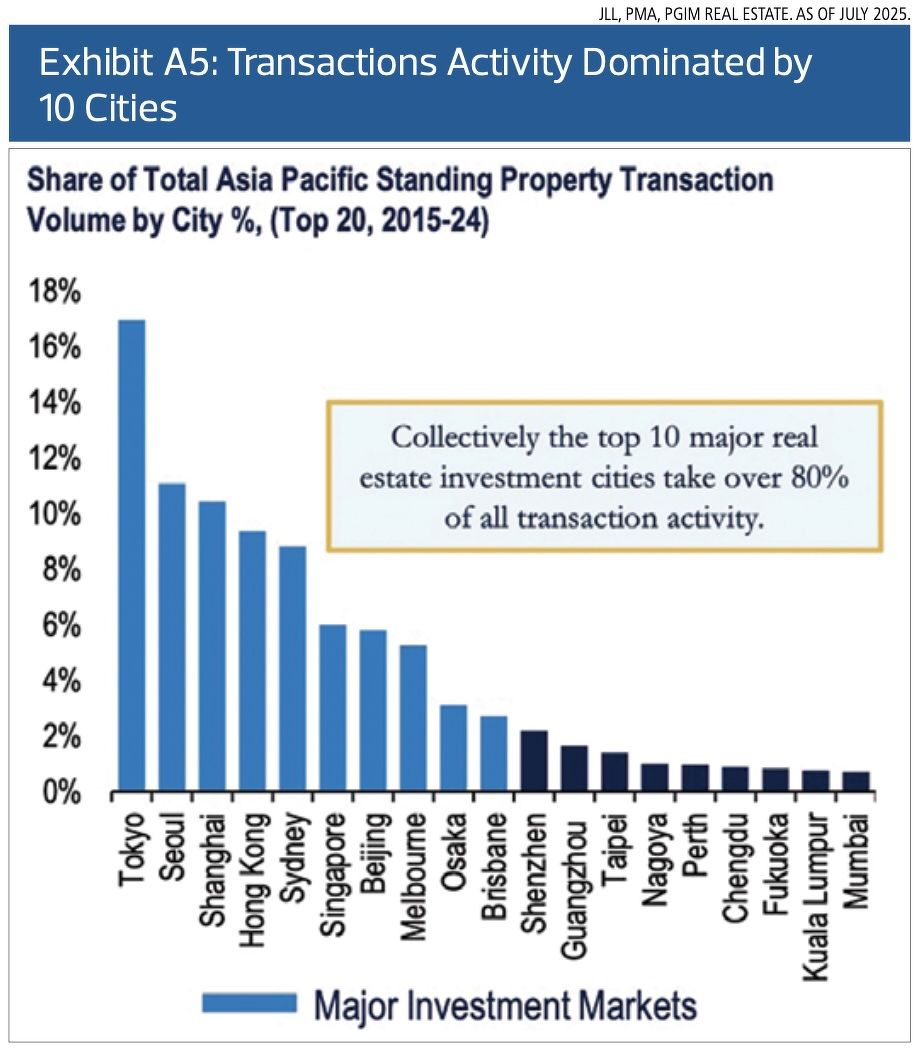

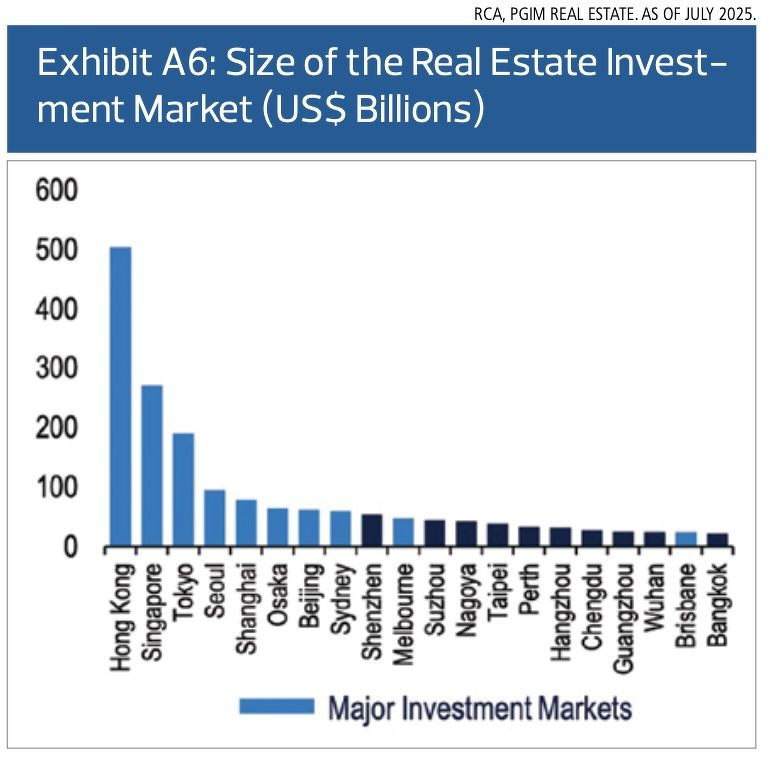

At the city level, just 10 cities captured nearly 80% of all transaction volume over the past decade (Exhibit A5). Liquidity and market size explain their dominance (Exhibits A6–A7). Nonetheless, liquidity is improving in second-tier cities such as Nagoya and Fukuoka, which are becoming increasingly institutionalised.

Opportunity-rich cycle

Asia Pacific real estate is entering a more selective but opportunity-rich cycle. While returns will be driven less by yield compression and more by rental growth and asset quality, the region offers investors clear avenues for outperformance.

Targeting mispriced assets, modernising under-invested stock, and building exposure to operational platforms will be key strategies to capturing the upside in the years ahead.

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search