Japan's property market demands a new adaptive playbook for investors

Now that Japan has awoken from deflation, property investors could shift towards strategies that emphasise rent growth and value creation, says LaSalle. (Photo: Unsplash)

Investors may need to recalibrate their approach to Japanese real estate as inflation returns after decades of falling prices.

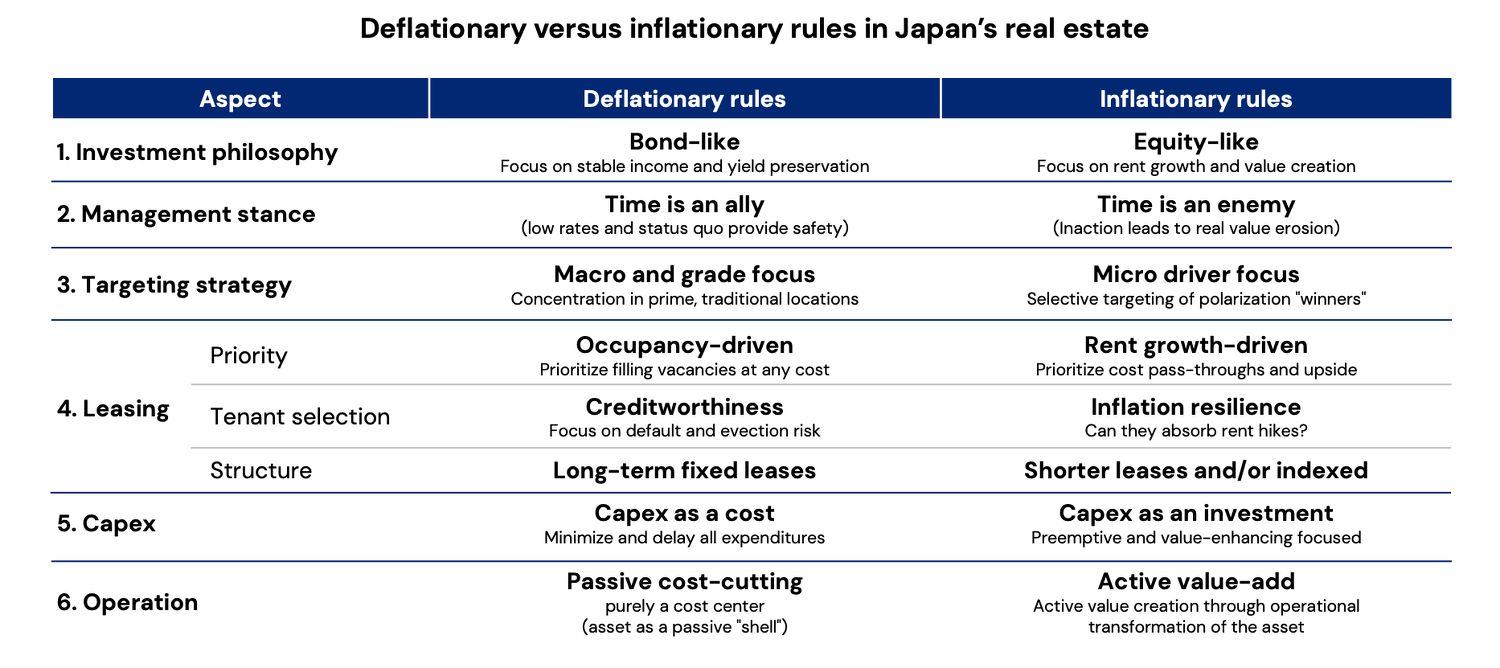

Strategies focused on occupancy and stability — once effective during the deflation era — should give way to approaches that emphasise rent growth and active asset management. According to global real estate investment manager LaSalle Investment Management, a subsidiary of JLL, the market is pivoting towards properties capable of capturing pricing power in an inflationary environment.

In its ISA Outlook 2026 report’s Asia Pacific (Apac) chapter, LaSalle suggests that this shift extends across the investment spectrum, from leasing structures and tenant selection to capital allocation.

From ‘three lows’ to ‘three hikes’

For three decades, Japan’s property market operated amid the “three lows”: low growth, low inflation and low interest rates.

That environment is changing. Japan is now experiencing the “three hikes”: rising prices, rising wages and rising interest rates. The Bank of Japan has ended its negative interest rate era, though borrowing costs remain historically low compared to other advanced economies. Inflation has returned after years of near-zero or negative price growth, and wage growth has also picked up.

Japan’s office sector has been supported by robust domestic demand. (Photo: Unsplash)

While equity markets have responded positively, the real estate sector has been slower to adapt. Property prices remain firm, but the J-REIT (Japan-listed REIT) market has softened. This divergence reveals an investor community “still hesitant to accept that the world they believed in is no longer real”, LaSalle notes.

According to the report, assuming a purely pessimistic outlook for real estate amid the Bank of Japan’s tightening would be overly simplistic. Because interest rates are deliberately held below nominal growth and inflation, the environment effectively lowers the cost of debt relative to inflation, creating “a quiet transfer of wealth” from savers to borrowers, the ISA Outlook 2026 notes.

This dynamic is reshaping yield expectations in the property market. Such an environment will reward assets that can raise rents in line with inflation and economic expansion, while penalising those “trapped by the old rules”, according to the report. Consequently, higher interest rates are unlikely to lead to a uniform cap-rate expansion across all assets. Instead, LaSalle expects to see differentiation based on properties’ ability to capture rental growth.

Real estate as equity, not bonds

What this means for real estate investors is that long-held assumptions may need to be reconsidered, according to Makoto Sakuma and Eduardo Gorab, the firm’s Apac co-heads of research and strategy, during a media roundtable on the report findings.

Sakuma (left): Internal migration will nurture a more diverse living sector. Gorab: Developers are turning to smaller-scale renovation and conversion projects. (Photos: LaSalle Investment Management)

Performance may increasingly depend on an “equity-like” investment philosophy, leasing strategies focused on rent growth, viewing capital expenditure as an investment and active value creation.

Most assets in Japan have been operating in a deflationary mindset, with rents barely increasing in the past 20 years, Sakuma notes. Owners tend to think of real estate like a fixed-income bond — to simply hold passively and prioritise stability over growth, as rental values were assumed to stay flat. “Many asset owners just focused on finding tenants as soon as possible once there was vacant space. As long as you had capital… you could rely on falling interest rates and eventually still make a profit,” he says.

But with Japan now seeing modest inflation, success depends on equity-like strategies that emphasise rent growth and value creation.

“If we can reposition to a value-add mindset, act more strategically, concentrate on adding capex to achieve a better NOI (net operating income), that could translate to better profits,” Sakuma shares. “This could open up a vast amount of opportunities for investors who can leverage it.”

LaSalle identifies several areas where Japanese real estate investment strategies could evolve. These include a shift in management approaches to have more active intervention, as inflation can erode value over time if properties are managed passively.

Inflation requires shift in Japan’s real estate mindset:

Source: LaSalle Investment Management, as of 11 Nov 2025.

In tenant selection, besides the traditional assessments of creditworthiness and default risk, investors may need to also consider tenants’ ability to absorb rent hikes — what LaSalle terms “inflation resilience”.

Leasing strategies could balance occupancy goals with rental growth, instead of solely aiming to fill space at any cost. Lease structures may also need to evolve, such as by switching from long-term fixed leases to shorter leases or the adoption of rent indexation clauses that allow periodic rent adjustments in line with inflation — a practice that is still relatively rare in Japan’s property market.

Capital expenditure (capex) ought to be viewed as investments instead of costs to be minimised and delayed. This is especially considering rising replacement costs and certain assets’ potential for rental growth.

“There are many, many assets that haven’t been capexed and with very low rents because that was the best way to achieve better NOI in the era of deflation,” Sakuma points out. He sees ample opportunities to improve or convert such properties in the current inflationary environment.

Gorab echoes the sentiment, describing the Japanese market as transforming to become more in line with what value-add or core-plus real estate investment strategies look like elsewhere in the world.

Resilient offices, durable homes, tourism growth

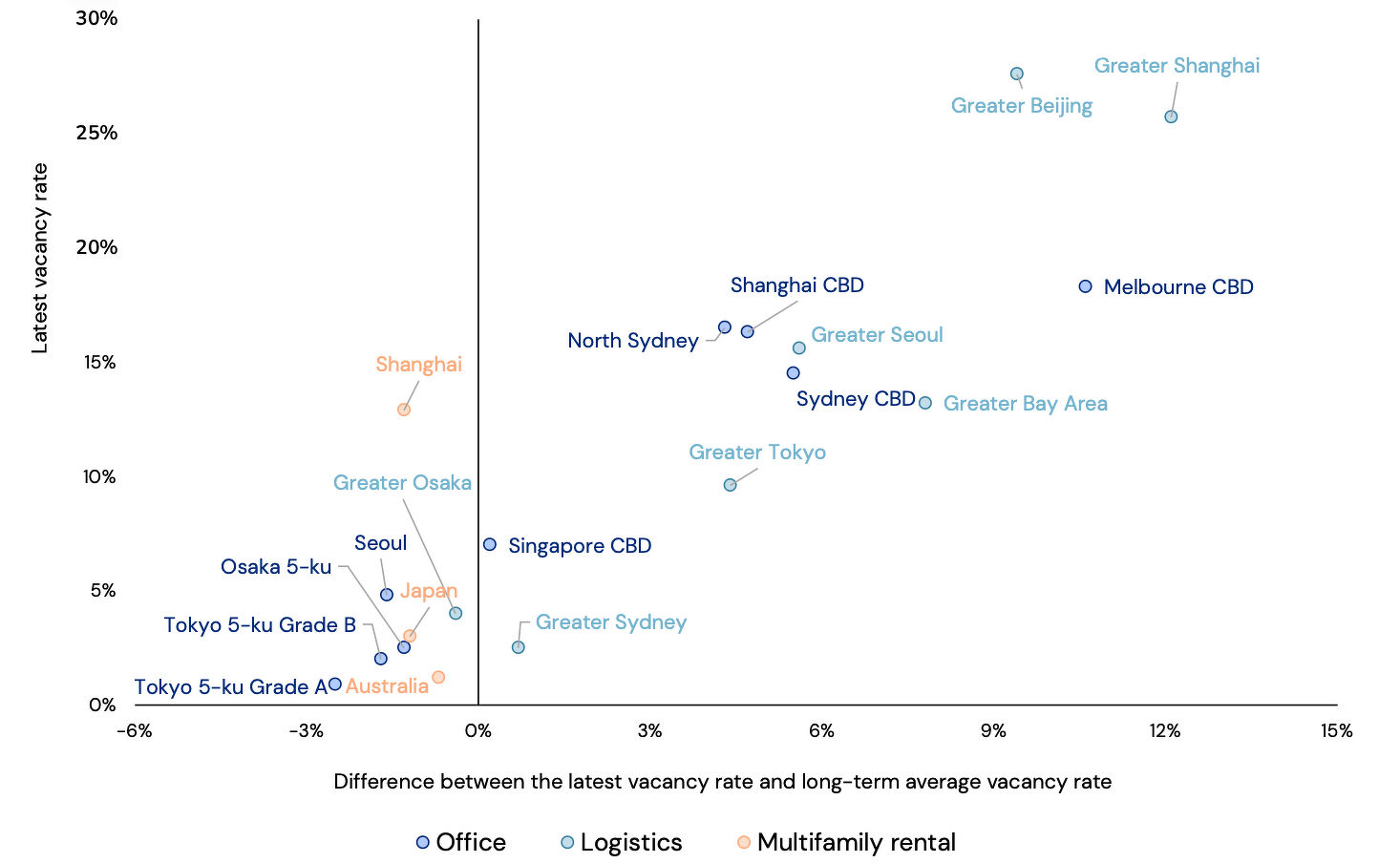

Market fundamentals vary by sector and location. The office sector has shown resilience in major markets such as Tokyo and Osaka and even some peripheral submarkets, with steady domestic demand keeping vacancy rates at historic lows. Occupancy and rents in these markets are likely to remain healthy, LaSalle says.

Vacancy rates in Apac by market and sector:

Source: LaSalle Investment Management’s ISA Outlook 2026; JLL REIS, Ichigo Real Estate Services, SQM Research.

Attractive opportunities could potentially be found in Grades A and B offices in “Tokyo 5-ku”, or the central five wards of Tokyo, namely Chiyoda, Chuo, Minato, Shinjuku and Shibuya, as well as offices in the “Osaka 5-ku” core business district. The latest vacancy rates in these segments were all less than 5% and have also tightened to fall below their long-term average vacancy rates since the early 2000s, based on LaSalle’s analysis.

Although new supply is expected to increase in a few of these tighter office markets in Japan, LaSalle sees upcoming projects having only a limited impact, with new completions absorbing pent-up relocation demand.

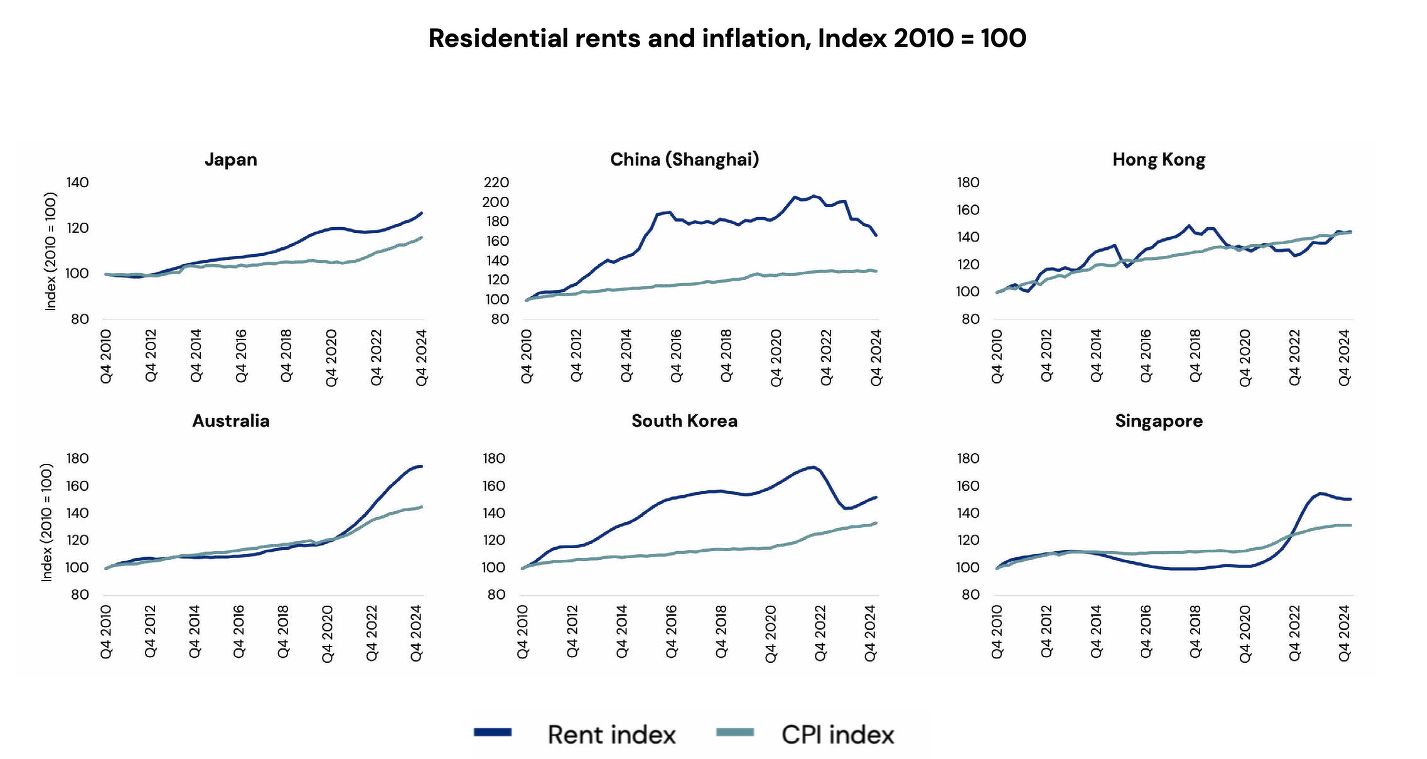

Meanwhile, the residential sector may offer protection against inflation, given inelastic housing demand. Residential rents in Japan have consistently outpaced inflation over the last 15 years, similar to other major Apac markets such as Shanghai, Hong Kong, Australia, South Korea and Singapore.

Residential rents in Apac have beaten inflation:

Source: LaSalle Investment Management’s ISA Outlook 2026; Sumitomo Mitsui Research Institute, SQM Research, Centaline Property, URA, Statistics Korea, Oxford Economics, as of 4Q2024.

This puts rental residential assets in a “uniquely strong position”, LaSalle reckons. In the midst of macro and geopolitical uncertainty, the investment manager sees opportunities in durable assets that can capture stable demographic drivers — from both natural population increases and migration — and needs-based demand.

For investors, demographics serve as a key filter in helping to guide capital towards locations and property types aligned with enduring demand. Although Japan’s national population has declined since 2009, strong internal migration towards metropolitan hubs like Tokyo and Osaka has more than offset population losses in those key metro areas, albeit at the expense of peripheral markets.

“Inner migration within Japan, with urban and suburban mobility, is making the market stronger and will also nurture a more diverse living sector, not only in terms of quantity but also quality [of assets],” Sakuma says.

Shibuya crossing in Tokyo. Japan has seen strong internal migration towards its metropolitan hubs. (Photo: Unsplash)

Residential assets in those dense urban nodes where people and capital cluster thus continue to demonstrate strong potential for net operating income growth.

Gorab highlights the importance of selecting the right locations strategically. “We think of location as a magnet, like a nexus of skill and expertise that is self-reinforcing,” he says. The focus is on “choosing the locations that are likely to have businesses that will be the exporters of the future and the locations where intellectual capital can congregate and aggregate together”, while also considering mobility and migration as a key factor, Gorab adds.

As for the hospitality sector, strong inbound travel momentum and a relatively weak yen compared with historical levels will support its continued outperformance, the report notes.

LaSalle expects Japan to achieve the government’s target of welcoming 60 million inbound tourists by 2030, driven by an increase in tourism flows from both Asian and Western markets.

Dotonbori, a key tourist and nightlife district in Osaka, Japan. (Photo: Unsplash)

Supply constraints

On the supply side, construction hurdles could support asset values. New supply is set to shrink across most sectors and markets in the region, given rising construction costs and interest rates amid inflation.

This calls for flexibility, creativity and disciplined capital use among developers in Apac. Some are changing their playbook, turning to smaller-scale renovation and conversion projects rather than large-scale redevelopment, Gorab notes. The focus is increasingly on unlocking value within existing assets through refurbishment, repositioning and adaptive reuse.

In Japan, labour shortages and pricier materials have pushed construction costs more than 30% above pre-pandemic levels, making real estate development increasingly challenging.

A key exception is the country’s office sector, where planned completions are slated to increase in major markets. This is in part because the sector has seen limited supply in the last few years and is also in response to the current strength of the sector, Gorab says.

A widening divide

Other developed markets have demonstrated how adaptive real estate strategies can succeed amid inflation, offering lessons that Japan can draw upon. That said, local insight and expertise will also be essential to translating these approaches into the Japanese context.

As the market adapts, the divide is likely to widen between investors sticking to the ways of the past and those embracing the new environment.

“The most adaptive players will find opportunity in the inertia of others,” the report notes. “This proactive mindset will be the decisive differentiator.”

For more news and analysis, read our weekly e-paper. Prefer a print copy? Get it delivered to your home every Monday.

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search