Middle East conflict sends shockwaves through construction supply chains

The closure of the Strait of Hormuz has caused oil production shortages even for Dubai (pictured), in the UAE, a major oil-exporting nation (Photo: Unsplash)

Amid the ongoing conflict in the Middle East, disruptions around the Strait of Hormuz — a key global oil transit route — have rippled across oil, gas and shipping markets.

While crude oil prices have surged as expected, the crisis is also disrupting commodity markets linked to the construction industry faster than anticipated, according to global construction consultant Linesight in an April 16 report. The firm has been tracking developments since the conflict escalated.

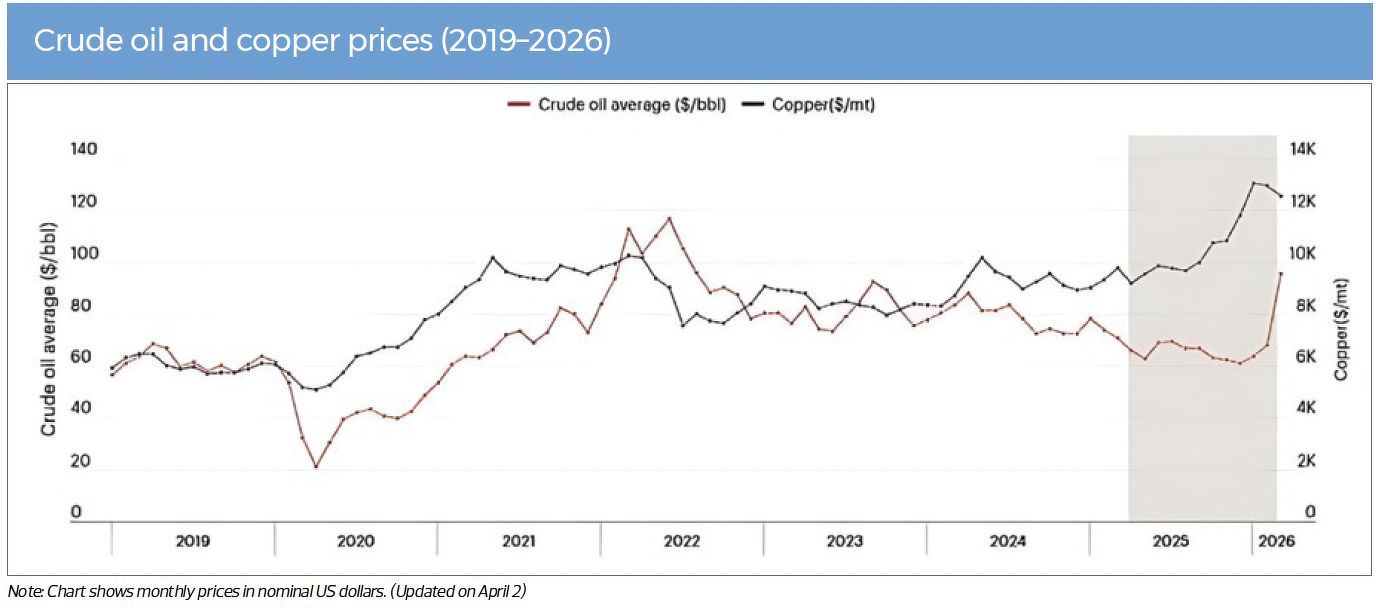

Chart: World Bank, Commodity Markets Outlook: Pink Sheet (March)

Although widespread material shortages have yet to happen, the conflict is introducing structural volatility across a range of import-dependent construction commodities.

Steel, cement and aluminium markets have been particularly affected, the report notes. Suppliers are responding with what Linesight describes as “cost noise” — shortening quote validity periods, imposing surcharges and delaying offers.

Rising supply-chain stress

Global supply-chain stress indicators are also rising, reaching levels not seen since 2022 due to front-loading, port congestion and reduced capacity across multiple freight routes, the report adds.

Within the construction sector, declining daily transits through the Strait of Hormuz have translated into longer lead times, higher landed costs (total cost of getting goods to their final destination) and less reliable delivery schedules.

Amid the ongoing Middle East conflict, disruptions around the Strait of Hormuz have created ripple effects (Photo: Linesight)

That said, the full impact of the conflict has yet to be felt, the firm notes. It points to past shocks. For instance, during the pandemic, supply chain disruptions fully materialised only about three months after the onset of the crisis.

Volatile pricing dynamics

Although oil prices are often used as a proxy for forecasting material costs, Linesight notes that they cannot be viewed in isolation. Most major construction materials are priced based on a range of factors, including raw material inputs, energy intensity, logistics exposure and demand outlook.

These dynamics help explain what the report describes as an “unexpected market response” in certain materials.

Aluminium, for instance, saw supply tighten more quickly than anticipated. With production concentrated in Australia and China, shipping disruptions and elevated operating risks caused imports into the Middle East to fall sharply — down 63% year-on-year in March.

Within days of the conflict, force majeure declarations in Bahrain and Qatar, together with smelter disruptions, heightened supply risk and pushed regional premiums in Europe and the US sharply higher.

Steel and copper under pressure

Global steel prices have also risen, with semi-finished steel recording sharper increases amid trade disruptions and higher substitution costs.

In Asia Pacific, South Korean steelmaker Posco raised prices by 50,000 won ($43.22) per ton across all distribution products, while Japan’s Kobe Steel increased long product prices by 10,000 yen ($79.90) per ton.

Copper markets, meanwhile, remain sensitive to both supply chain and geopolitical disruptions.

Sulphur — a key input in copper refining — is largely produced as a by-product of oil and gas processing, making copper supply particularly vulnerable to disruptions in energy markets and refinery operations.

With about half of global seaborne sulphur trade passing through the Strait of Hormuz, copper supply faces heightened risks amid potential sulphur shortages.

Although copper prices recently fell 9.4% due to a stronger US dollar, high inventories and demand concerns, they have rebounded on supply-side tightness, the report notes.

Looking ahead, Linesight expects copper prices to remain volatile as the market grapples with supply constraints and a projected deficit of up to 30% over the coming decade without significant new investment.

For more news and analysis, read our weekly e-paper. Prefer a print copy? Get it delivered to your home every Monday.

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search