SE Asia's resilient growth to fuel real estate investments, with data centres and industrial assets in focus: C&W

Singapore was the biggest contributor of real estate investments across the top six Southeast Asian economies in 2025 (Photo: Samuel Isaac Chua/EdgeProp Singapore)

Southeast Asia remains one of the fastest-growing economic regions globally. Research compiled in Cushman & Wakefield’s Southeast Asia Outlook 2026, shows that Southeast Asia’s GDP has continued to register growth despite a turbulent global trade environment last year, with estimates showing an increase of 4.8% for 2025. The figure is based on the top six Southeast Asian economies (SEA-6): Singapore, Malaysia, the Philippines, Thailand, Indonesia and Vietnam.

In 2026, GDP growth is expected to rise by 4.3%. Published in March, the report highlights that private consumption, a key driver of growth in the region, has remained resilient, supported by relatively low unemployment rates and rising household incomes.

These positive economic metrics, coupled with favourable demographics and rapid infrastructure development, have put Southeast Asia on track to become the fourth largest economy in the world, says Cushman & Wakefield.

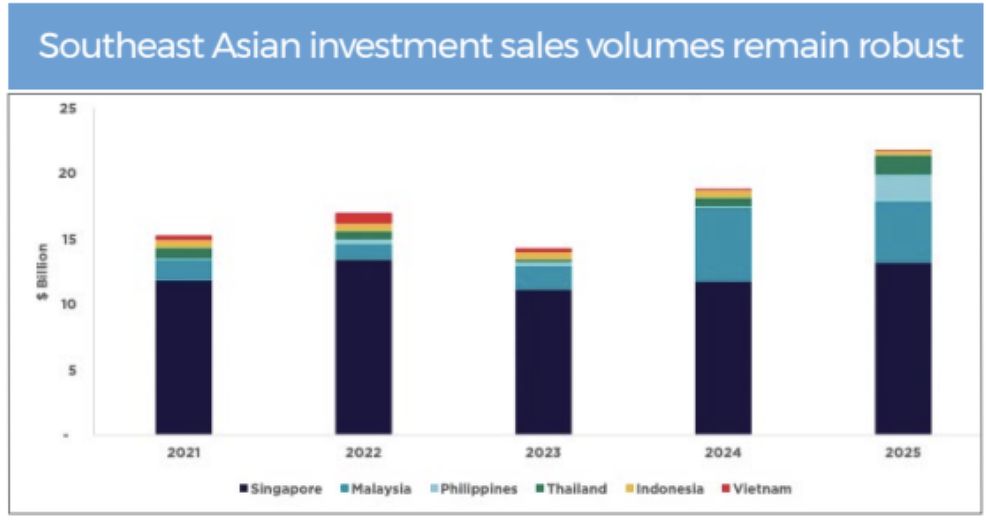

This, in turn, is expected to benefit the real estate sector as investments into Southeast Asia continue to show steady momentum. In 2025, the region’s real estate investment sales totalled an estimated US$21.8 billion ($27.7 billion), almost 16% higher y-o-y. Within the region, Singapore remained a key driver of overall activity, accounting for roughly 61% of total investment volume across the SEA-6 economies.

Chart: RCA, Cushman & Wakefield Research, data retrieved AS AT Feb 2

The firm anticipates real estate investments to remain strong in 2026, with property demand supported by the region’s growing role as a global manufacturing hub, as well as its rising importance as a consumer market. In addition, lower interest rates could also prompt more institution-driven deals as investors look to recycle capital.

Data centres and industrial assets shine

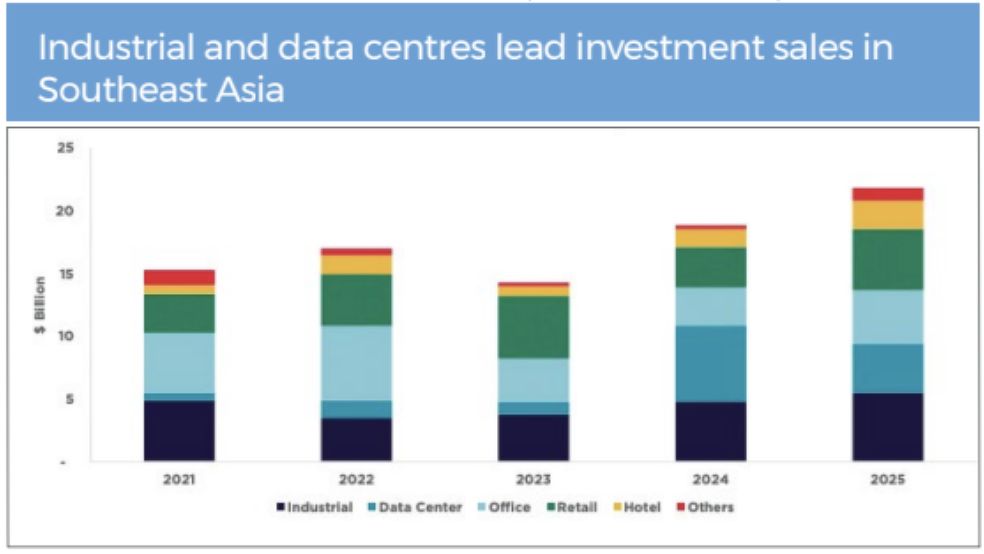

Cushman & Wakefield notes that industrial and data centre assets are shaping the investment landscape as industrial growth, accelerating digitalisation and urbanisation fuel demand for data centres. This is particularly true for the emerging markets in Southeast Asia, which the report defines as the SEA-6 economies, excluding Singapore.

Its report shows that data centres accounted for the highest levels of investment sales for the emerging Southeast Asian economies in 2025. Among these, Malaysia stood out: it logged roughly US$2.6 billion in data centre investment deals last year, mostly in Johor, which the report attributes to spillover demand from Singapore.

Chart: RCA, Cushman & Wakefield Research, data retrieved AS AT Feb 2

Moving forward, the firm expects Malaysia’s data centre sales to moderate as power and water constraints start weighing on future expansions. As for the other emerging markets, data centre infrastructure in Thailand, Indonesia, the Philippines and Vietnam remains underserved, offering further opportunities for growth and investment.

As for industrial real estate investments, these totalled US$1.3 billion across the emerging Southeast Asian markets, underpinned by deals for warehouses and prime logistics assets. The rising demand for such assets is backed by a robust e-commerce sector and the region’s growing importance as a manufacturing hub, amid shifting global trade dynamics, the report states.

Other sectors to watch

Across the other sectors, Cushman & Wakefield highlights that hotels have continued to attract demand as regional tourism picks up in Southeast Asia. While tourist arrivals from China continue to lag pre-pandemic levels, the hospitality industry has received a boost from recovering international visitor arrivals, alongside a rise in the popularity of affordable wellness destinations.

Among the SEA-6, Thailand continues to dominate in tourist arrivals in the region. That said, Malaysia is also seeing strong tourism growth, which is translating to investments: the country is contributing nearly 30% of hotel investment sales across the SEA-6, excluding Singapore.

The recovery in visitor arrivals has also coincided with stronger retail activity across the region. Against a backdrop of growing private consumption in Southeast Asia, international retailers are increasingly embarking on expansions across the region. “With consumers craving in-person experiences and e-commerce impact proving lower than anticipated, well-located malls with strong tenant mixes continue to enjoy healthy occupancy and rental growth,” the report adds.

To that extent, the retail real estate sector could see a further boost in activity in the near term, backed by strong market fundamentals. Additionally, emerging retail destinations could also contribute to activity, with the Johor retail scene being the one to watch, says Cushman & Wakefield. With the Johor Bahru-Singapore Rapid Transit System (RTS) set to be completed at the end of 2026, the enhanced connectivity positions Johor to capture increased cross-border spending, the report adds.

Country-specific opportunities

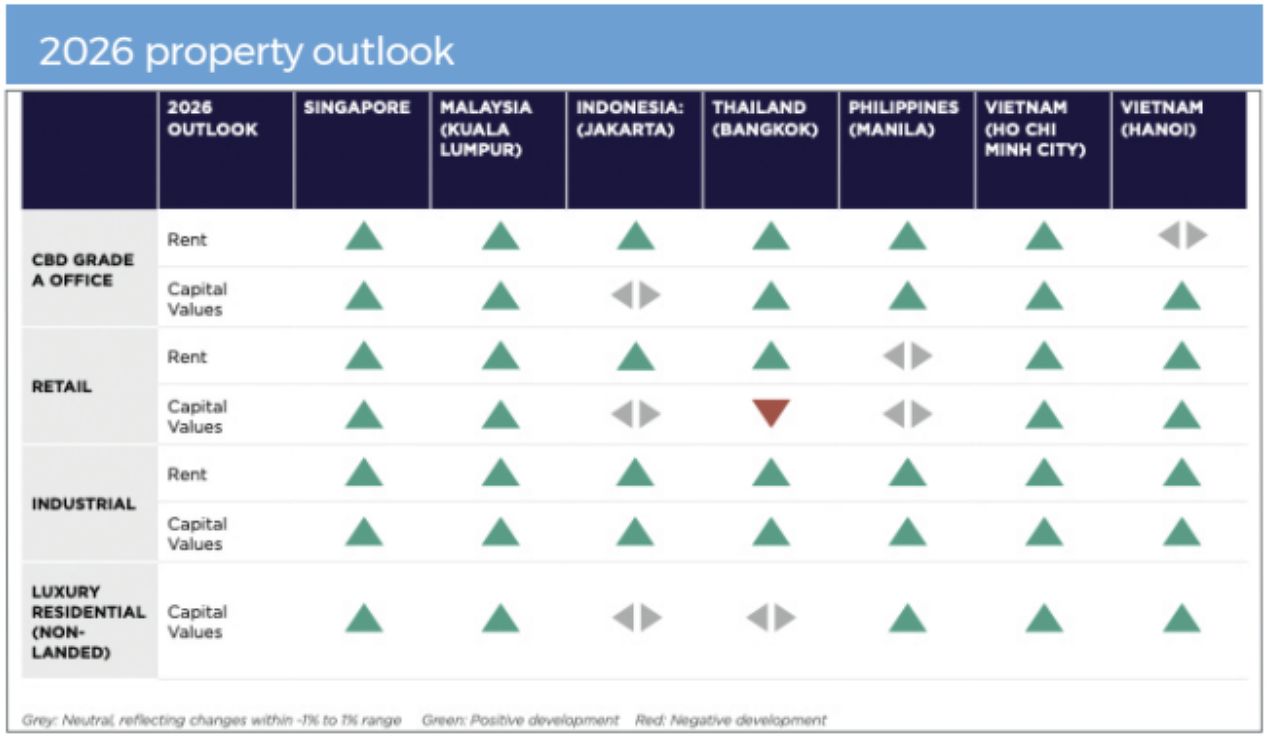

Cushman & Wakefield’s report observes a diverse landscape of investment opportunities across Southeast Asia for 2026, shaped by major developments in each market.

Table: Cushman & Wakefield Research

In Singapore, capital recycling continues to drive sales activity as Reits, investment funds and property companies divest assets to realign portfolios. With borrowing costs easing and property yields holding firm, the firm expects core investments to pick up in 2026, which is likely to support deals in the office sector.

In Malaysia, the rollout of large-scale infrastructure projects — such as the Johor-Singapore Special Economic Zone, the RTS Link and transit-oriented developments, including the Tun Razak Exchange — is anticipated to continue driving investments. In addition, Malaysia is expected to see growth from high-value sectors such as semiconductors and data centres, supported by its strategic location, developed infrastructure and capable workforce.

As for Indonesia, the commercial and residential property sectors are slated to see a boost in development from the phased completion of the Jakarta MRT, while easing mortgage rates are anticipated to stimulate housing demand. Meanwhile, the industrial sector is projected to maintain strong market momentum, supported by new infrastructure like the Patimban Access Toll Road.

Meanwhile, in Thailand, the industrial property market is seeing rising foreign investment, with Cushman & Wakefield noting strong demand for ready-built factories catering to the digital, electronics, machinery and automotive sectors. The ongoing recovery in the hotel industry is also expected to support capital market activity, with tourist arrivals to Thailand projected to hit 90% of pre-pandemic levels this year.

Lastly, Vietnam: the residential and industrial sectors are projected to lead activity here. In the industrial real estate segment, multiple developments have been approved for development, in tandem with robust foreign capital inflows into manufacturing sectors such as semiconductor and electronics. Meanwhile, strong demand for housing is propelling new residential developments, particularly in the high-end and luxury segments.

For more news and analysis, read our weekly e-paper. Prefer a print copy? Get it delivered to your home every Monday.

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search