Singapore Central Region office rents fall by 0.2% q-o-q in 1Q2026, submarkets perform unevenly

Based on property consultants’ basket of assets, core CBD Grade A rents rose across the board, with CBRE recording a 0.8% q-o-q increase and Newmark seeing 1.5% q-o-q rise in core premium Grade A rents. (Photo: EdgeProp Singapore)

The rental index for offices in the Central Region recorded a 0.2% drop q-o-q in 1Q2026, a reversal from the 0.4% quarterly gain in 4Q2025, according to statistics released by URA on April 24.

The decline was largely driven by uneven performance across submarkets, says Catherine He, head of research at Colliers. Rents for offices outside of prime areas, mostly comprising older buildings, have eased, while rental growth in the core CBD gained traction due to limited supply and sustained flight-to-quality demand.

Based on property consultants’ basket of assets, core CBD Grade A rents rose across the board. CBRE recorded a 0.8% q-o-q increase to $12.40 psf per month, marking the fifth consecutive quarter of growth, while Newmark saw a 1.5% q-o-q rise in core premium or Grade A rents at Raffles Place and Downtown to $12.15 psf per month.

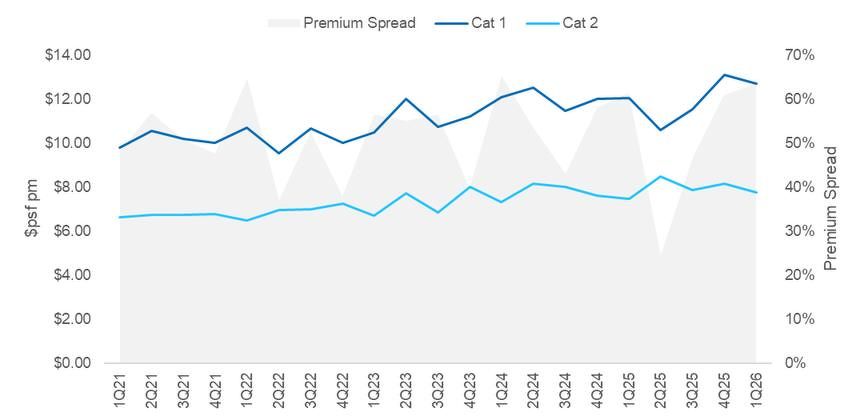

June Chua, senior managing director and head of Singapore leasing at Newmark, notes that the spread between Category 1 and Category 2 median rents in the Central Area widened further to 63.6% in 1Q2026, from 60.8% in 4Q2025.

Newmark's office rents for Category 1 and Category 2 buildings in Central Area

(Source: URA, Newmark Research)

Category 1 space transacted at $12.71 psf per month, as compared to Category 2's $7.76 psf per month. That reflects the growing divergence between premium and secondary stock.

Chua further notes that backfill spaces have emerged in older Grade A buildings as tenants upgraded to newer, higher-specification developments, though these were quickly reabsorbed, reflecting the overall tightness of the market.

In Knight Frank’s view, as tenants migrate to more modern and well-equipped options, older buildings are facing downward rental pressure.

Tightening vacancy

URA data shows islandwide office vacancy fell to 10.8% in 1Q2026, from 11.1% in the previous quarter, making this the fourth consecutive quarter of improvement. Net absorption increased by 0.28 million square feet over the period, pushing overall occupancy up 0.3 percentage points q-o-q to 89.2%.

Colliers attributes the tightening to companies consolidating, relocating and selectively expanding into the core CBD. Over the longer term, landlords of older buildings may need to consider asset enhancement or repositioning to remain competitive, as tenants place greater emphasis on building efficiency, green credentials and fit-out quality.

Based on CBRE’s basket of assets, vacancy rates for core CBD (Grade A) offices have shrunk to 3.3% in 1Q2026, down from 4.5% in the preceding quarter.

Tricia Song, CBRE’s head of research, attributes this to structural demand for large, contiguous Grade A floor plates, with occupiers in financial services, wealth management and quantitative trading continuing to anchor leasing activity.

Key developments in the core CBD, such as IOI Central Boulevard Towers, Marina One and Marina Bay Financial Centre (MBFC), continued to attract active leasing activity in the quarter, according to CBRE.

Leonard Tay, head of research at Knight Frank, says occupiers remain drawn to newer Grade A offices in the CBD as they balance prestige, accessibility, talent attraction and retention alongside cost considerations.

As a result, landlords of certain non-CBD offices are beginning to feel the effects of the flight to quality, as companies in decentralised locations reassess opportunities to move into prime central developments vacated or downsized by other tenants.

Well-connected, decentralised hubs such as Buona Vista and the Alexandra corridor continue to attract occupiers seeking cost-effective alternatives. Within these locations, higher-specification buildings are outperforming neighbouring properties in terms of occupancy and tenant retention, Tay says.

Landlords of older or less competitive assets in these areas are responding with flexible lease structures, fitted-out space options and targeted incentives to attract price-sensitive occupiers, he says.

Keen investor interest

Office prices in the Central Region edged up by 0.2% q-o-q in 1Q2026, reversing from a 0.7% decline in the previous quarter. Colliers expects this growth to accelerate, citing keen investor interest in Singapore office assets.

Beyond the established financial services sector, demand in 1Q2026 has expanded to include a wider range of occupiers.

“International AI companies, supported by venture capital funding and rapid technology adoption, have been actively seeking space to establish regional hubs in Singapore and are expected to require additional space in the near term given their growth trajectories,” says He.

According to CBRE’s Song, many AI companies are graduating from co-working arrangements into dedicated, self-managed offices. Well-located, high-specification properties that can capture the flight-to-quality and flex-space trends are also expected to be particularly attractive to investors.

Notably, the absence of additional buyer's stamp duty on commercial strata office assets makes them particularly attractive to foreign investors seeking to deploy capital into Singapore, adds Newmark’s Chua.

Geopolitical uncertainty adds caution, reinforces Singapore's appeal

The ongoing Middle East conflict has introduced an additional layer of caution into occupier decision-making, with some businesses adopting a more guarded stance on expansion and relocation.

However, Knight Frank’s Tay posits the situation has also reinforced Singapore's safe-haven status, with multinational firms operating in affected regions potentially considering the city-state as a stable base for their Asia Pacific operations.

He adds that rising energy costs stemming from the conflict could increase building operating expenses over time, with the impact likely passed through to tenants via service charges. Occupiers in energy-efficient buildings are expected to be better insulated from such cost pressures.

According to Newmark’s Chua, higher fit-out costs, driven by supply chain disruptions, may also prompt more occupiers to renew existing leases rather than relocate — at least until there is greater clarity on the macroeconomic outlook.

Mixed outlook on rental growth

Looking ahead, CBRE Research maintains its forecast for core CBD Grade A rental growth of approximately 5% year-on-year for 2026, reflecting the firm’s confidence in the durability of the current upcycle.

Meanwhile, Newmark expects rents for premium and Grade A office space to rise 3%–5% for the full year, though q-o-q growth could ease in the coming quarters.

Colliers predicts quarterly growth to be uneven, with momentum concentrated in premium and well-located assets.

CBRE’s Song says: “Despite global trade tensions, geopolitical uncertainty and macroeconomic headwinds, Singapore’s structural advantages such as its role as a regional headquarter hub, strong regulatory framework and historical resilient post correction recovery profile, will underpin its positive outlook.”

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search