Surge in workers' dormitory rents halts in 2H2025 as supply-demand gap narrows

The 10,500-bed Pioneer Lodge was completed across two phases in 2025 (Picture: Samuel Isaac Chua/EdgeProp Singapore)

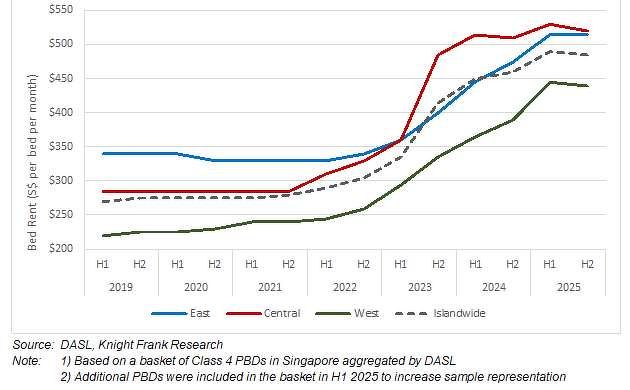

Rents for workers' dormitories in Singapore declined in 2H2025, reversing from a surge that started in 2019. Data in a March research report jointly published by the Dormitory Association of Singapore Limited (DASL) and Knight Frank Singapore found that the islandwide average monthly rent for a bed in a Class 4 commercial dormitory (which refers to dormitories that can accommodate 1,000 or more workers) inched 1% lower to $485 in 2H2025, from $490 in 1H2025.

This is the first time rents have moderated on a half-year basis since DASL and Knight Frank began tracking the data in 2019, based on a basket of Class 4 purpose-built dormitories. It also ends an unbroken surge in dormitory bed rents in recent years. In 1H2025, average dormitory bed rents islandwide stood at $490 per bed per month (pb pm), representing an 81.5% increase from the pre-pandemic trough of $270 pb pm in 1H2019.

Average dormitory bed rents islandwide and by zones

The lower islandwide rent in 2H2025 was supported by flat or declining rents across all three dormitory zones in Singapore. In the east zone, which covers the Kaki Bukit, Changi, East Coast and Bendeemer districts, the average bed rent stood at $515 pb pm in 2H2025, unchanged from the first half of last year.

In the central zone, which includes Tanjong Pagar, Marsiling, Seletar and Sembawang, the average bed rent declined by 1.9% to $520 pb pm in 2H2025 compared to 1H2025. Rents in the west zone (Jurong, Pioneer, Tengah and Tuas) also fell across the same period, declining 1.1% to $440 pb pm.

Moderating demand, rising supply

The lower workers' dormitory rents come amid easing demand and supply pressures in the market. For the former, DASL and Knight Frank’s report notes that the intensity of demand for dormitory beds, which hit full throttle from 2022 onwards following the lifting of border restrictions after the pandemic, has moderated as geopolitical disruptions and other factors weigh on the global economic climate.

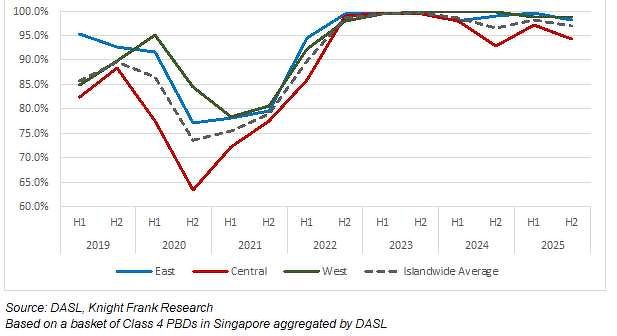

Consequently, occupancy levels for workers' dormitories in both the central and east zones fell in 2H2025 compared to the first half of the year, based on DASL and Knight Frank’s basket of dormitories. For the central zone, occupancy fell from 97.2% to 94.5%, while in the east, occupancy fell from 99.7% to 98.3%.

Average dormitory occupancy rates islandwide and by zones

Dormitories in the West remained almost full in 2H2025, with occupancy unchanged at 99%. Nonetheless, overall occupancy inched downward, with the average islandwide occupancy rate declining to 97.1% in 2H2025, compared to 98.3% in 1H2025. The wider availability has coincided with a lower number of workers on the waitlist for the next available bed, further signalling easing of demand pressure.

Stock of workers' dormitories by class

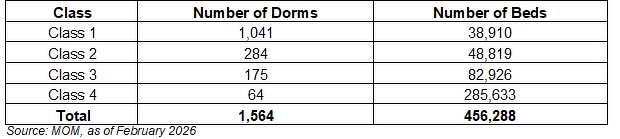

At the same time, the supply of workers' dormitories has continued growing. As of 2H2025, there are 64 Class 4 dormitories with 285,633 beds, higher than the 60 Class 4 dormitories with about 274,000 beds reported by DASL and Knight Frank for 1H2025. Based on the latest figure, the number of Class 4 beds as of 2H2025 makes up 62.6% of the total islandwide bed load, which also includes Class 1, Class 2 and Class 3 dormitories that accommodate fewer workers.

Recent completions include the 10,500-bed Pioneer Lodge, which commenced operations across two phases last year: 3,088 beds became operational in April, followed by another 7,412 beds towards the end of the year. Elsewhere, Westlite Toh Guan received the temporary occupation permit for a new block with 1,764 beds in October 2025.

Westlite Toh Guan has been expanded, with the completion of an additional block with 1,764 beds in October 2025 (Picture: Albert Chua/EdgeProp Singapore)

Rental growth of 5% for 2026

More workers' dormitories have opened since the start of 2026, including the 2,400-bed NESST Tukang Dormitory – the first dormitory to be developed by the Ministry of Manpower (MOM). The dormitory, which complies with guidelines under MOM’s New Dormitory Standards, is expected to be fully occupied by May.

Under MOM’s Dormitory Transition Scheme (DTS), existing workers' dormitories will need to be updated to meet DTS guidelines by 2030. As such, DASL and Knight Frank expect available bed inventory to be impacted over the next five years as more dormitories undergo improvement works.

Notwithstanding supply constraints, demand for beds is expected to remain resilient, backed by robust construction demand, sustained maritime activity, and ongoing mega-infrastructure projects.

As a result, the report predicts dormitory bed rents to grow at around 5% for the whole of 2026. “Transient supply constraints should prop up occupancies and support rental growth,” the report states. At the same time, as more dormitories complete their upgrades, rents may be adjusted upwards to reflect the improved quality.

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search