Why BTO supply, not curbs, is key to cooling HDB resale prices

Since 2021, the authorities have tightened the loan-to-value ratio for HDB loans on three occasions — December 2021, September 2022, and August 2024 (Photo: Samuel Isaac Chua/EdgeProp Singapore)

Despite a raft of government measures aimed at curbing demand, HDB resale flat prices have surged by more than 50% since bottoming out in 2Q2019. This stark rise reflects a deeper truth: demand-side interventions have limited effectiveness when supply fails to keep pace with housing needs.

Demand curbs have a limited, short-term impact

Since 2021, the authorities have tightened the loan-to-value (LTV) ratio for HDB loans on three occasions — December 2021, September 2022, and August 2024.

In September 2022, the medium-term interest rate used to compute the mortgage servicing ratio (MSR) was also raised by 0.5 percentage points. A 15-month wait-out period was imposed that same month for private property owners (PPOs) and former private property owners before they could buy a resale flat.

While these measures may have temporarily delayed purchases, they did not dampen genuine demand — especially when resale flats serve an essential housing need. Buyers returned once eligible, and prices continued to rise.

Supply-side levers deliver more lasting impact

On the supply front, the government typically responds by ramping up the launch of Build-To-Order (BTO) and Sale of Balance Flats (SBF). These flats, offered directly by HDB, are more affordable than resale flats and can help absorb demand.

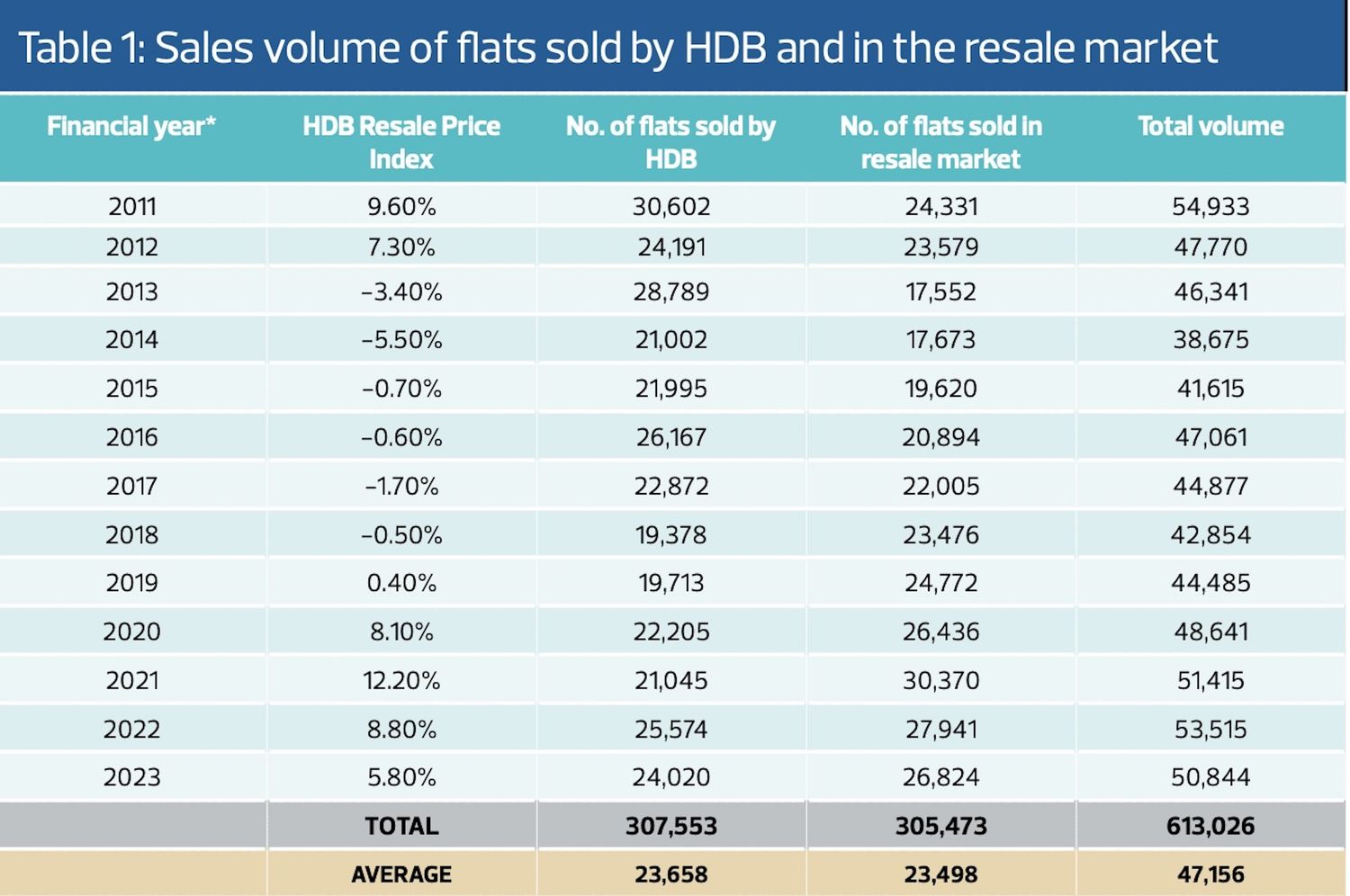

History supports this. In FY2011 (April 1, 2010 to March 31, 2011), HDB recorded a record 30,602 new flat bookings (BTO and SBF), which coincided with a slowdown in resale price growth to 9.6%, from 12.8% the year before.

This trend continued in FY2012 and FY2013, when flat bookings remained high — 24,191 and 28,789 units respectively — and resale price growth moderated further, eventually contracting by 3.4% in FY2013.

From FY2015 to FY2018, HDB scaled back its BTO supply. Sales bookings hovered above 21,000 units annually — down from the annual average of 25,000 between FY2011 and FY2014.

From FY2015 to FY2019, only 81,000 new flats were released, or about 16,000 annually. Unsurprisingly, resale prices bottomed out in FY2019, as buyers turned to the resale market amid dwindling BTO supply.

The pandemic shock — and the supply response

The Covid-19 pandemic was a black swan event. Construction delays, work-from-home arrangements, and supply chain disruptions pushed homebuying activity into overdrive. Resale prices surged 8.1% in FY2020 and 12.2% in FY2021 — a cumulative increase of more than 20% — despite efforts to boost BTO supply.

Recognising this, HDB stepped up its new launches. In FY2022 and FY2023, it booked 25,574 and 24,020 new flats, respectively. Resale volumes declined, and price growth slowed to 8.8% and 5.8% — down from the 12.2% high in FY2021. These figures reinforce a key point: higher BTO booking volumes, particularly above 21,000 units, help moderate resale market heat.

Note: Flats (BTO, DBSS, SBF and others) sold by HDB are based on HDB Annual Reports (*financial year from April 1 to March 31 the following year), which include actual and projected bookings. The HDB Annual Report 2024/2025 is not available as of July 22, 2025. Source: HDB Annual Reports, HDB, Huttons Data Analytics

SBF: Not a silver bullet

Conventional wisdom suggests that SBF units, which are often completed or near-completion, should exert more immediate pressure on resale prices. However, there is no clear correlation.

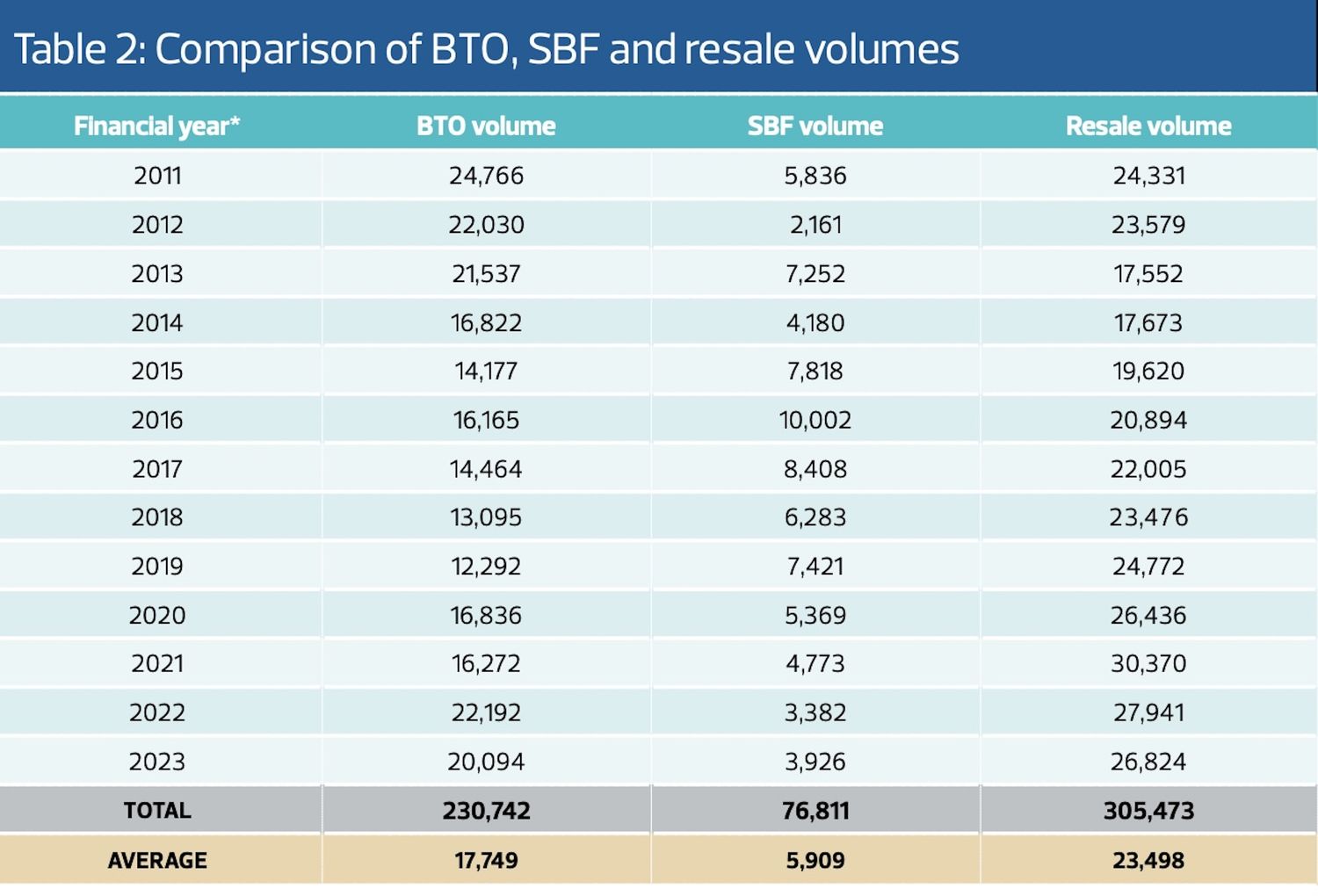

Between FY2011 and FY2023, increases in SBF bookings did not consistently correlate with drops in resale volume — the only clear declines occurred in FY2011 and FY2013.

This may be due to buyers being deterred by limited flat availability in specific towns, lower ballot success rates, and restrictions under the Ethnic Integration Policy (EIP). As a result, SBF bookings appear to have a weaker influence on resale demand and prices compared to BTO flats.

Note: Flats (BTO, DBSS, SBF and others) sold by HDB are based on HDB Annual Reports (*financial year from April 1 to March 31 the following year), which include actual and projected bookings. The HDB Annual Report 2024/2025 is not available as of July 22, 2025. Source: HDB Annual Reports, HDB, Huttons Data Analytics

The BTO-resale price link is stronger

The relationship between BTO bookings and resale prices is more pronounced. From FY2011 to FY2013, high BTO booking volumes corresponded with price moderation. From FY2014 to FY2021, bookings dipped below 21,000 units — and resale prices rose again.

As BTO launches ramped up in FY2022 (22,192 bookings) and FY2023 (20,094 bookings), price growth eased to 8.8% and 5.8%, respectively. Although FY2023 bookings dipped below the 21,000-unit threshold, the 15-month wait-out period for ex-PPOs may have contributed to the price moderation.

The evidence suggests that sustained booking volumes of over 21,000 BTO flats annually are necessary to cool resale price growth. Assuming a BTO take-up rate of 85%–90%, this translates into a launch volume of 23,000 to 25,000 flats per year — a target HDB has not consistently hit in recent years.

What about newly MOP flats?

Another factor is the release of flats that have just met their Minimum Occupation Period (MOP). These flats, typically newer and more desirable, often fetch a premium and may uplift overall resale prices.

Yet, the correlation between newly MOP flats and resale prices is weak (33%) in the year of MOP. However, with a two-year lag, the correlation strengthens significantly to 86.2%. This suggests that most flat owners do not sell immediately after fulfilling the MOP — but when they do, typically one to two years later, the market feels the full impact.

Key takeaways

- Supply matters more than curbs: Demand-side policies like LTV tightening or wait-out periods have only short-term effects. Sustainable cooling requires robust BTO supply.

- BTO matters more than SBF: While SBF flats are faster to be occupied, BTO booking volumes more consistently influence resale price movements.

- The 21,000-unit threshold: Historical trends show that booking volumes above this figure are needed to moderate price growth. To achieve this, HDB may need to launch between 23,000 and 25,000 BTO flats annually.

- Watch the MOP pipeline: A surge in MOP-flat supply may lift resale prices one to two years down the line — a factor that policymakers must weigh carefully.

A balancing act

Ultimately, HDB faces a complex challenge: it must manage public housing affordability while maintaining demand for executive condominiums and private housing. Oversupply in the BTO segment may soften resale prices now — but could inflate them later when these flats re-enter the market post-MOP.

Still, if the goal is to ensure housing affordability and a stable resale market, the answer is clear: Build more — and build consistently. The numbers show that supply, not restrictions, is the more effective lever.

Lee Sze Teck is the senior director of data analytics at Huttons Asia

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search