HDB resale transactions slow y-o-y in first quarter of 2026; uptick in million-dollar flats

Transaction volumes slowed from the year-ago period, with 6,285 flats changing hands as compared with 6,590 in 1Q2025. (Photo: Unsplash)

In Singapore’s public housing market, 6,285 resale flats were transacted in the first quarter of 2026, slowing on a y-o-y basis, albeit increasing on a q-o-q basis.

HDB released the latest figures on April 24, with its resale price index also showing that prices inched down by 0.1% during the quarter — in line with the public housing authority’s flash estimates published earlier this month.

While the number of resale transactions rose by 19.6% in 1Q2026 from 5,256 in 4Q2025, this was likely to be seasonal because the first quarter of a year tends to be busier than the fourth quarter, said Mark Yip, chief executive at Huttons.

But compared to the first quarter of 2025, when 6,590 transactions were recorded, resale volumes were 4.6% lower in the latest quarter.

That is the lowest first-quarter volume since 2021, and could be due to the concurrent launch of the Build-To-Order (BTO) and Sale of Balance Flats (SBF) exercises in February 2026 pulling demand away from the resale market, in Huttons’ view.

Christine Sun, chief researcher and strategist of Realion (OrangeTee & ETC) Group, said: “We observed that deals are taking longer to close in recent months, as buyers had more housing options and sentiment has slowed in view of the uncertain macroeconomic conditions.”

SRI head of research and data analytics, Mohan Sandrasegeran, said the slight moderation on a y-o-y basis may reflect a more balanced market environment as demand remains intact but is more evenly distributed. Buyers today have a wider range of options, with a continued ramp-up in BTO and SBF supply and more MOP flats entering the market.

“This could be redistributing demand across different housing segments rather than concentrating it solely within the resale market,” said Sandrasegeran.

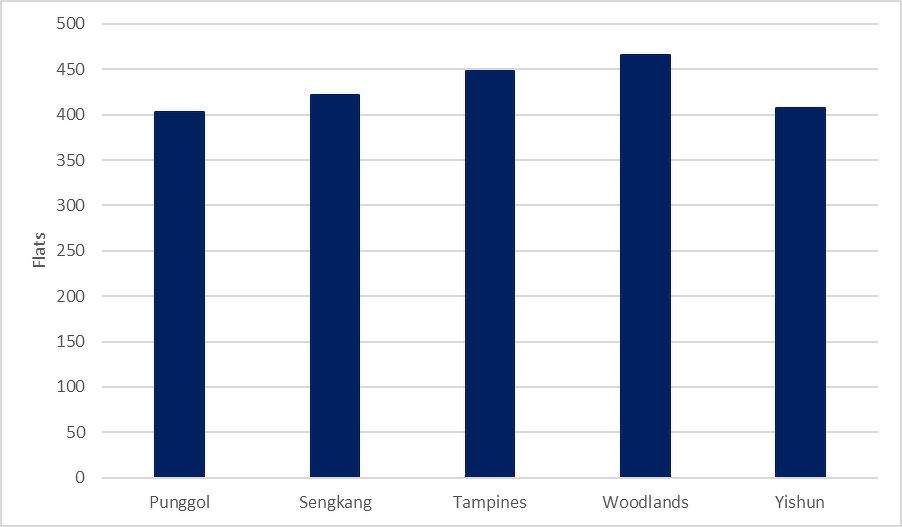

In 2025, the five most popular HDB towns among buyers were Punggol, Sengkang, Tampines, Woodlands and Yishun. Based on caveats lodged, they accounted for about 35.5% of total transactions in the first quarter of 2026.

Top five HDB towns among buyers in 1Q2026:

Source: HDB, Huttons Data Analytics; as of April 24.

More million-dollar flats

An estimated 412 HDB resale flats were sold for $1 million or more during the quarter, about 17.4% higher q-o-q.

These comprise 190 four-room flats, 143 five-room flats, 78 executive flats, and a multi-generation flat, according to PropNex.

Wong Siew Ying, head of research and content at PropNex, noted that some of the choicest units in attractive locations continued to see pricing upside.

That said, million-dollar deals still account for just 6.6% of total quarterly transactions, which is a relatively small share while the overall resale market remains broadly accessible to the typical homebuyer, said ERA Singapore key executive officer Eugene Lim.

As more flats in mature estates fulfilled their five-year minimum occupation period (MOP), the number of million-dollar deals also increased in tandem.

At least 63 deals, or 15% of million-dollar HDB transactions in 1Q2026, involved units that recently obtained their MOP, with remaining leases of 94 years or more, according to ERA. The bulk of these transactions were concentrated in newer projects such as Alkaff Courtview and Ang Mo Kio Court, which recorded 24 and 20 deals, respectively.

Million-dollar deals during the quarter continued to be concentrated in towns such as Toa Payoh, Queenstown, Bukit Merah and Ang Mo Kio. “This reflects persistent demand for newer HDB homes in central locations, which are not subject to the tighter resale conditions applied to Plus and Prime flats,” Lim commented.

HDB data showed that median resale prices for five-room flats reached $1.1 million in Toa Payoh, $1.09 million in Ang Mo Kio, and $1.085 million in Bukit Merah. The next-highest were $970,000 in Bishan and $930,500 in Kallang/Whampoa.

For four-room flats, median prices hit the million-dollar mark in Queenstown and Toa Payoh, at $1.038 million and $1 million respectively. The next-highest median prices for four-room flats were seen in Bukit Merah at $938,000 and Kallang/Whampoa at $929,000.

On average, million-dollar flats across Singapore fetched about $1.151 million during the first quarter this year, which is 1.2% lower than the previous quarter’s $1.165 million, Huttons noted.

The most expensive resale flat in the latest quarter was a five-room premium loft apartment at SkyTerrace @ Dawson that went for $1.7 million. It measures 1,313 sq ft and has a remaining lease of about 89 years, EdgeProp Singapore reported in February.

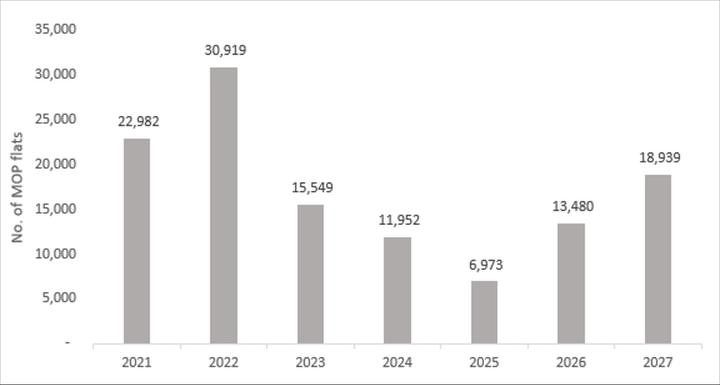

More MOP flats expected this year

Resale supply is set to expand significantly in 2026, with an estimated 13,480 flats reaching their MOP — nearly double the 6,973 units last year, ERA noted.

This influx will broaden buyers’ choices across locations and flat types, helping to sustain transaction volumes even as price growth remains moderate, said Lim.

Number of MOP flats by year:

Source: data.gov.sg, ERA Research and Market Intelligence

Nearly 70% of flats reaching their MOP this year are in popular towns such as Punggol, Tampines, Toa Payoh and Queenstown.

In these towns, the newly MOP flats are likely to command higher asking prices, supported by their “strong location appeal” and relatively longer remaining leases, Lim said.

Distribution of MOP flats by town in 2026:

Source: data.gov.sg, ERA Research and Market Intelligence

Overall resale prices dip

Amid increased supply, prices of resale flats fell slightly by 0.1% in the first quarter of 2026, compared with the previous quarter.

This is the first decrease in the HDB resale price index since it bottomed out in 2Q2019.

PropNex’s Wong said: “We are watchful on whether the gap between HDB resale prices and non-landed private home prices, particularly in the Outside Central Region, will continue to widen.” A widening gap between HDB resale and private housing prices, over time, may potentially make the leap for HDB upgraders more challenging, she added.

The dip in resale prices came amid regular and sustained supply of BTO flats over the past four years, noted Yip. Some of these BTO flats had a shorter waiting time of three years or less, while the SBF exercises also offered buyers another alternative to resale flats, he added.

The resale market’s price growth has decelerated for six consecutive quarters since 3Q2024.

Across different flat types, price movements varied. Caveat data showed quarterly price declines for one-room (-4.4%), five-room (-0.7%) and executive (-2.9%) flats, Realion’s Sun pointed out. Marginal price gains were recorded for two-room (1.5%), three-room (1%) and four-room (0.8%) flats.

Going by HDB towns, 10 out of 26 of them saw prices decreasing by between 0.1% and 6.9% in 1Q2026, according to Huttons Data Analytics. This was an improvement from the previous quarter, when more than half of the towns saw price declines, Yip shared.

Prices of four-room flats in top five HDB towns in 1Q2026:

Source: HDB, Huttons Data Analytics; as at April 24.

Clementi posted the biggest decline of 6.9% for resale flat prices, followed by Marine Parade with a 5.6% decrease and Bukit Timah with a 5.2% drop, according to Huttons.

Sandrasegeran from SRI said that overall, the latest price movement suggests that earlier supply measures are beginning to take effect in a more visible way. “The moderation in 1Q2026 should not be viewed as a downturn, but as part of a broader normalisation process driven by sustained supply expansion,” he added.

Demand fundamentals remain intact, supported by household formation and genuine housing needs, but the urgency that previously drove sharper price increases is gradually easing, in Sandrasegeran’s view.

Tenants could have the upper hand in rental market

As at the end of the first quarter this year, there were 58,598 HDB flats rented out, a marginal decrease of 0.1% from the 58,775 flats rented out in the fourth quarter last year.

Median rents for executive units were the highest in Bedok at $4,200 per month, followed by Tampines at $4,000 and Jurong West at $3,780, based on approved applications to rent out HDB flats in the first quarter of 2026. Choa Chu Kang and Sembawang posted the lowest median rents for executive flats, at $3,300 and $3,500 per month respectively.

For five-room flats, Queenstown posted the highest median rent of $4,400. Next on the list were Bukit Merah at $4,200, as well as Clementi and Kallang/Whampoa at $4,100.

On the other end were Bukit Panjang, Choa Chu Kang, Hougang, Punggol, Sembawang, Sengkang and Woodlands with five-room flats fetching about $3,230 to $3,300 per month for five-room flats.

Four-room flats commanded median monthly rents of $4,200 in the Central Area, $4,150 in Queenstown, as well as $3,900 in Bukit Merah and Clementi.

Three-room flats were going for $3,200 per month in the Central Area, $3,030 in Marine Parade, and $3,000 in Bishan, Bukit Merah, Clementi, Kallang/Whampoa, and Queenstown.

HDB said the data on median rents is based on rents self-declared in the application forms, and does not include cases where there are fewer than 20 rental transactions in the quarter for the particular town and flat type.

Noting the dip in HDB rental applications on both a q-o-q and y-o-y basis, Realion’s Sun said that this year, the tide may turn in favour of tenants as the public housing supply is expected to climb.

“As more than 50,000 flats reach their MOP over the next three years, we expect more flats to be listed for rent, intensifying competition among landlords,” she shared. Tenants, having more housing options available, could have greater negotiating leverage and stronger bargaining power to secure better rental rates and leasing terms.

At the same time, the impact of the HDB supply surge may spill over to the private rental market — young expatriates who prioritise convenience and accessibility might switch to renting HDB flats instead of private homes.

“Some may find the benefits of residing in a new flat, with proximity to MRT stations, malls or other amenities, outweigh the advantages of living in a private condo,” Sun remarked.

Resale market may face 'soft landing' in 2026

Yip reckoned that the HDB resale market may be heading for a “soft landing” in 2026.

“The bargaining chips are slowly shifting to the buyers, and sellers are taking longer than the usual six to eight weeks to sell,” he said.

This is similar to the 2011-2014 period when HDB had pushed out more than 100,000 BTO flats for application. HDB resale prices started to see some softness in 2013 and continued to stay weak for more than five years till 2019, Yip noted.

Sun anticipates more buyers to look to the BTO market as a few “attractive” projects will be launched this June, including the second BTO project at the Greater Southern Waterfront precinct.

With housing supply set to rise over the next few years, she foresees downward pressure on resale flat prices. Price growth could also remain subdued — rising modestly by 2% to 4% for the whole of this year — amid macroeconomic uncertainties, in Realion’s view.

In its April 24 release, HDB said that the macroeconomic outlook has become more uncertain, and households should continue to exercise prudence when purchasing property and taking out mortgage loans.

SRI’s Sandrasegeran pointed to rising energy prices and supply chain pressures, which could contribute to higher inflation in the coming months. These cost increases may gradually filter through into the economy including the built environment sector, potentially affecting construction costs and business expenses.

Buyers may adopt a more measured approach in such an environment, although these factors are not likely to materially weaken underlying housing demand, Sandrasegeran said.

SRI expects resale transaction volumes to total about 26,000 to 27,000 flats this year, with prices possibly growing at a more measured pace of about 2% to 3.5%.

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Related Articles

Top Articles

Search