Industrial rents rise for 22nd straight quarter, but momentum eases in 1Q2026

For business parks, supply remains limited, with only one project — 27 International Business Park — expected over the next three years (Photo: Samuel Isaac Chua/EdgeProp Singapore)

Ask Buddy

- Industrial rents in Singapore rose for the 22nd consecutive quarter, but momentum eased to 0.4% q-o-q, reflecting tenants’ growing selectivity for asset specifications and location amid global uncertainties.

- Single-user factory rents led growth at 1% q-o-q in 1Q2026, with occupancy improving to 89.2% and major completions like Trans Auto Logistics’ facility at 4B Jalan Besut bolstering segment performance.

- Despite a 19.8% drop in transaction volume to 369 caveats, activity in smaller strata units remained robust, with more than half of deals below $1.5 million, underscoring sustained investor appetite for freehold assets.

AI generated

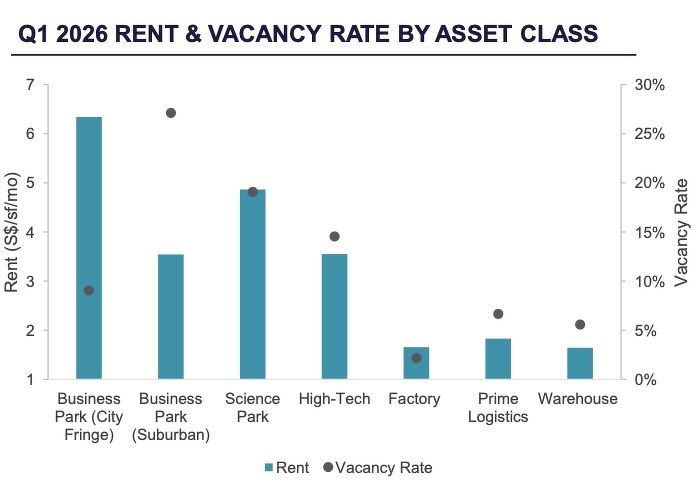

The JTC All Industrial Rental Index increased 0.4% q-o-q in 1Q2026, easing from 0.5% in the previous quarter. On a y-o-y basis, rents rose 2.3% and are up 26.5% since the pandemic trough in 3Q2020.

“While occupier demand remains resilient, tenants are increasingly selective, with location and asset specifications becoming key differentiators beyond headline rents,” says Tricia Song, CBRE head of research for Singapore and Southeast Asia.

Despite ongoing global uncertainties, the industrial market continued to record growth in both rents and prices in 1Q2026, notes Wong Xian Yang, head of research for Singapore and Southeast Asia at Cushman & Wakefield (C&W). However, he cautions that the ongoing Middle East conflict has introduced downside risks, particularly through higher energy and logistics costs.

The Purchasing Managers’ Index (PMI) dipped slightly to 50.5 in March but remained in expansionary territory for the eighth consecutive month. Manufacturing output declined 0.1% y-o-y in February after five months of expansion, with growth in 1Q2026 driven solely by the electronics cluster.

Selectivity emerges across segments

Rental growth was led by the single-user factory segment, where rents rose 1% q-o-q in 1Q2026, up from 0.7% in the previous quarter. Occupancy improved by 0.4 percentage points to 89.2%.

Major completions during the quarter included Trans Auto Logistics’ facility at 4B Jalan Besut and Sumitomo Seika’s facility at 12 Sakra Road.

Rents for multi-user factories increased 0.5% q-o-q, accelerating from 0.2% in 4Q2025, while occupancy edged up to 90.2%. New completions included food factories such as Smart Food @ Mandai and Azalea Kitchens, as well as the final phase of Stellar @ Tampines, a strata-titled B2 development.

In the business park segment, rents rose 0.3% q-o-q, moderating slightly from 0.4% in the previous quarter, while vacancy increased to 23.3%. According to CBRE, the rise in vacancy was driven by older or less competitive assets in Rest of Island locations struggling to retain tenants.

By contrast, newer, higher-specification developments in city-fringe locations continued to benefit from flight-to-quality demand, resulting in a two-tier performance across the segment.

C&W notes that suburban business parks and prime logistics buildings recorded stronger rental growth of 1.7% and 1.5% q-o-q, respectively, while conventional factories and high-tech assets saw more modest increases.

Warehouse rents rose 0.2% q-o-q, easing from 1.1% in the previous quarter, as occupancy dipped to 89.4%. Notable completions included Jurong Logistics Terminal 5 and Katoen Natie’s two-storey ramp-up warehouse at 1 Banyan Place, as well as CWT’s cold-chain logistics facility at 8 Jalan Besut.

“With no new completions available for lease until 2027, vacancy rates in prime logistics properties are set to tighten,” says Catherine He, head of research at Colliers. “However, rental growth is expected to be capped as occupiers become more cost-conscious and prioritise efficiency.”

Source: Cushman & Wakefield

Prices continue to outpace rents

The JTC industrial price index rose 1.2% q-o-q in 1Q2026, easing slightly from 1.4% in the previous quarter. This marks the eighth consecutive quarter in which price growth has outpaced rental increases, supported by sustained investor demand, notes CBRE.

Tridiana Ong, head of occupier strategy and solutions at Knight Frank Singapore, attributes part of the price increase to the listing of UI Boustead REIT, which comprises 21 local industrial assets valued at $1.3 billion.

Large-ticket transactions during the quarter included CapitaLand Ascendas REIT’s $749.2 million acquisition of assets at 25 Loyang Crescent and a 50% stake in The Ascent, as well as Standard Chartered Bank’s sale and leaseback of two Changi Business Park assets for $183 million. Far East Organization also sold four warehouses for $322 million.

However, transaction volume declined 19.8% q-o-q to 369 caveats lodged, although this remains above the quarterly average of 310 transactions in 2019. More than half the deals were below $1.5 million, indicating continued activity in smaller strata units.

“The majority of the units that changed hands were freehold strata developments, highlighting keen investor interest in such assets,” says Wong.

Domestic interest rates remain supportive, with the three-month SORA easing to 1.04% as of April 23, from 1.19% at the end of 2025. “Amid geopolitical uncertainty, investors continue to gravitate towards leasehold industrial assets as they offer stable income and positive carry,” adds CBRE’s Song.

Source: Cushman & Wakefield

‘Stockpiling demand’

The ongoing Middle East conflict could lead to a prolonged period of elevated energy prices, driving up construction and logistics costs, says C&W's Wong. “This may temper new development demand and further tighten supply over the medium term as overall development costs rise,” he adds.

At the same time, higher transportation costs are expected to push occupiers to prioritise well-located logistics facilities and build buffer inventory. Wong expects “stockpiling demand” to return amid supply-chain uncertainties and volatile energy prices.

This could support stronger demand for warehouse space, adds Colliers’ He. For instance, specialty chemical producers such as Evonik, Kuraray and Cariflex — which last year launched the world’s largest polyisoprene plant in Singapore — are scaling up operations, driving demand for storage.

Meanwhile, chemical logistics player Katoen Natie is investing $60 million in a new warehouse on Jurong Island to expand capacity, underscoring continued confidence in Singapore as a petrochemicals hub.

Supply pipeline and structural drivers

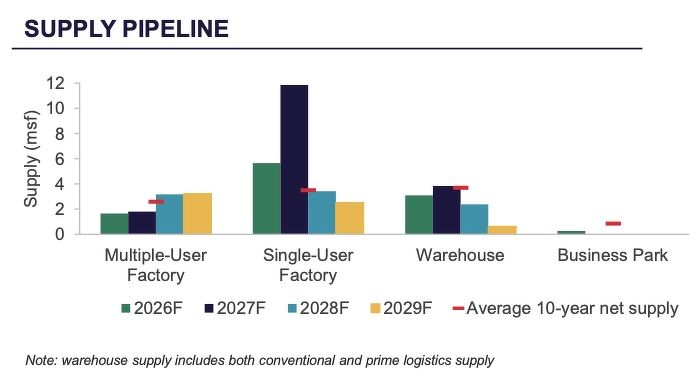

As of end-March 2026, about 8 million sq ft of new industrial space — equivalent to 1.4% of total stock — is scheduled for completion over the next three quarters.

Single-user factories account for 60.5% of the pipeline, followed by warehouses (30.1%), multi-user factories (6.1%) and business parks (3.3%).

For business parks, supply remains limited, with only one project — 27 International Business Park — expected over the next three years. At the same time, asset enhancement initiatives for older developments could further tighten available space, says CBRE.

Prime logistics supply is also expected to ease significantly in 2026, with most upcoming facilities already pre-committed. CBRE estimates occupancy in this segment at 95.8% as at 1Q2026, potentially rising to 97% by year-end.

Structural demand drivers remain intact, particularly for high-specification logistics and advanced manufacturing facilities. CapitaLand Investment’s OMEGA 1 Singapore, a fully leased smart logistics facility incorporating automation and robotics, exemplifies the shift towards technology-enabled infrastructure.

JTC has also announced plans for an AI park in one-north and the rollout of LaunchPad @ Punggol Digital District, which are expected to support demand for business park space from AI startups and research activities.

Outlook: Uncertainty persists, but demand holds

Advance estimates from the Ministry of Trade and Industry show Singapore’s economy contracted 0.3% q-o-q in 1Q2026, reversing the 1.3% expansion in the previous quarter. Manufacturing growth moderated to 5% y-o-y, down from 11.4% in 4Q2025, although electronics, transport engineering and precision engineering continued to expand.

“The Middle East conflict that began in end-February may have heightened economic uncertainties in the near term,” says CBRE’s Song. “However, occupier demand has remained firm, supported by AI-related manufacturing.”

While some investors may adopt a more cautious stance, Knight Frank expects deals already in advanced stages to proceed, supported by relatively low borrowing costs. The firm forecasts industrial prices to grow by 3% to 5% for the full year.

C&W projects rental growth of up to 2% in 2026, with potential upside in business parks and well-located high-tech developments. However, rental growth in the logistics segment is expected to moderate as tenants resist further increases amid rising operating costs.

Chua Yang Liang, JLL head of research for Southeast Asia, expects rents to grow at a more modest pace of 1% to 2%, alongside price growth of 2% to 3%, as capital continues to seek relatively stable markets such as Singapore.

Meanwhile, the Johor-Singapore Special Economic Zone (JS-SEZ) could reshape occupier strategies, allowing firms to split operations across borders — anchoring high-value activities in Singapore while shifting more space- and labour-intensive functions to Johor.

“As greater clarity emerges, execution risk should ease, translating into improved investor confidence and investment commitments,” says Song.

Ask Buddy

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search