Lessons from the most successful condo launches in 2025

Skye at Holland was almost sold out during its launch in October last year (Photo: Samuel Isaac Chua/EdgeProp Singapore).

Ask Buddy

Many factors play a part in driving demand for new condos. Last year saw the launch of around 25 condos, with an average take-up rate of 57% at launch. Five of them stood out, achieving launch take-up rates exceeding 90%. Thereafter, all condos saw their take-up rates improve, with nine securing take-up rates above 90% at the time of writing.

An examination of these popular new condos shows that they share several common factors. As always, location takes centre stage. Proximity to amenities is also vital, especially for projects located further from the city centre. In addition, the reputation and track record of the developer cannot be overlooked.

The top performers

Among the condos launched for sale last year, 15 reported take-up rates exceeding 50% during their launch month (see Table 1). Based on caveats lodged at the time of writing, all 15 condos have since achieved take-up rates of more than 65%. Notably, Lentor Central Residences is fully sold, while Skye at Holland and LyndenWoods are almost sold out.

Get the latest details on available units and prices for PARKTOWN Residence

Most of the 15 condos are 99-year leasehold developments, with freehold Bagnall Haus being the exception. As the only project with fewer than 300 units, Bagnall Haus is also the smallest development.

While it may be tempting to conclude that homebuyers are more receptive to 99-year leasehold new condos, the stellar sales performance of such developments is likely due to the fact that most condos launched for sale last year have 99-year leasehold tenures, rather than reflecting buyers’ preference.

Lesson 1: Central Region remains popular with buyers

Among the 15 top performers, four achieved take-up rates exceeding 90% during their launch month, namely Skye at Holland, LyndenWoods, Penrith and Lentor Central Residences. Of these four condos, only Lentor Central Residences is not located in the Central Region.

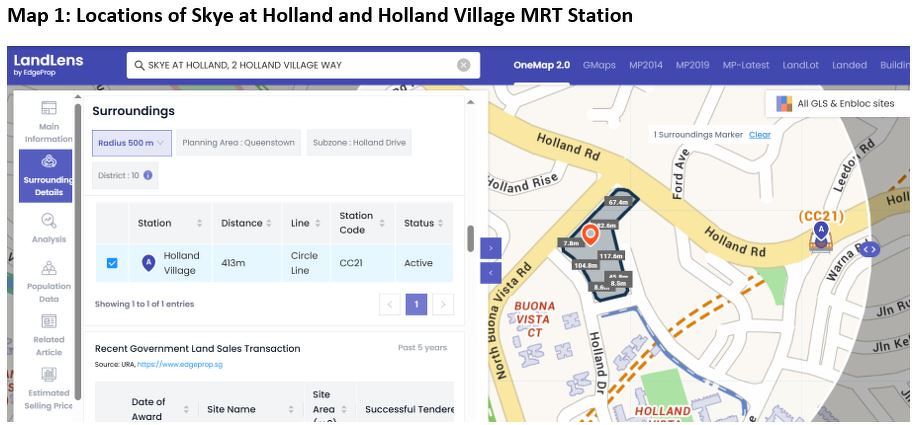

Skye at Holland met with an overwhelming response during its launch weekend due to its location in prime District 10. Being situated within both a prime district and the Central Region means that the project is close to the CBD and Orchard Road. Future residents of the upcoming condo will also enjoy being within walking distance of Holland Village MRT Station, Holland Village and One Holland Village (see Map 1).

At the time of writing, 661 caveats have been lodged for Skye at Holland, indicating that only five units from the 666-unit development remain unsold.

Source: EdgeProp LandLens

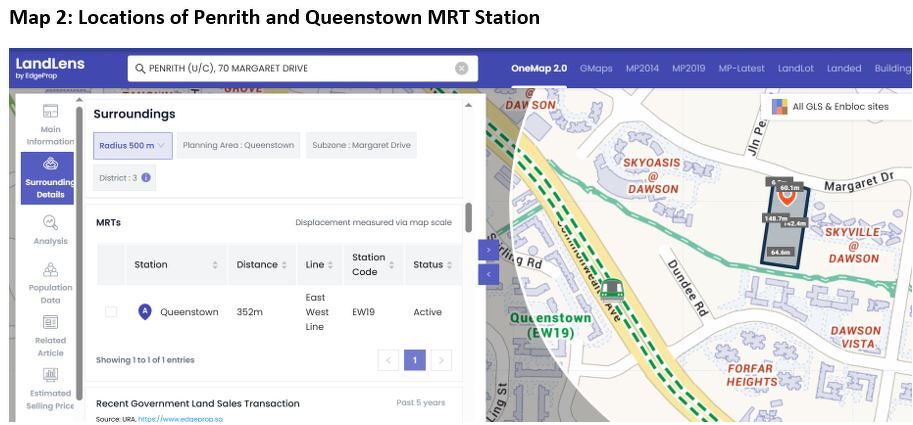

Penrith is also located within the Central Region, albeit in the less prestigious District 3. Nonetheless, it is a short drive from Orchard Road and the CBD. In addition, Queenstown MRT Station and Dawson Place are within walking distance (see Map 2). Schools within a 1km radius include Queenstown Primary School, Queenstown Secondary School and Queensway Secondary School.

Penrith achieved a robust take-up rate of 95% in its launch month. Since then, its take-up rate has increased to 97.2%, indicating that only 13 units in the 462-unit development remain unsold at the time of writing.

Source: EdgeProp LandLens

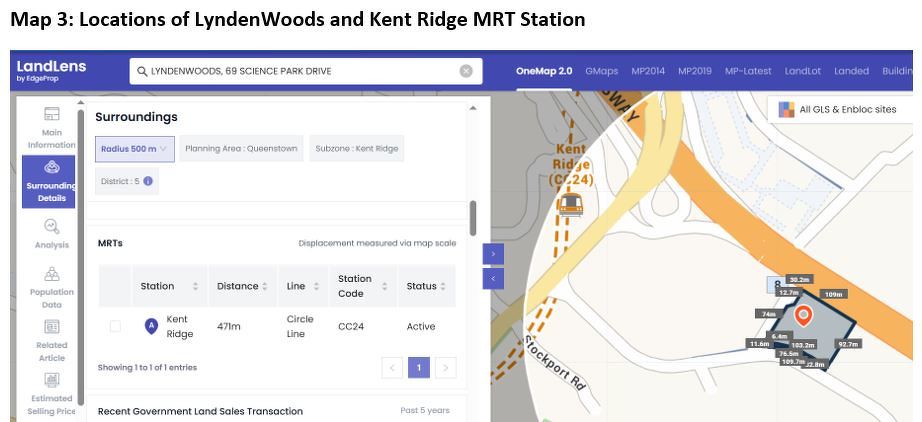

LyndenWoods is conveniently located within walking distance of Kent Ridge MRT Station, the Ayer Rajah Expressway, Kent Ridge Park and the newly opened Geneo (see Map 3). It is also a short drive from one-north and the National University of Singapore, making the condo attractive to homebuyers working in the business park as well as landlords seeking to attract tenants employed there.

During its launch month, LyndenWoods achieved a take-up rate of 95.6%. Based on caveats lodged at the time of writing, the take-up rate has since increased to 99.4%, indicating that only two units remain unsold.

Source: EdgeProp LandLens

Aside from the above-mentioned projects, five other top-performing condos are located in the Central Region, namely The Orie, UpperHouse at Orchard Boulevard, River Green, Zyon Grand and Promenade Peak. Among these five, River Green, Zyon Grand and Promenade Peak are located in close proximity to one another, as well as to Great World MRT Station and Great World City. They are also a short drive from Orchard Road and the CBD.

Notably, all three condos achieved strong take-up rates exceeding 50% during their launch month. Based on caveats lodged at the time of writing, River Green leads the pack with a take-up rate of 91.8%, followed by Zyon Grand (86.7%) and Promenade Peak (65.1%). Combined, the three developments have fewer than 350 unsold units.

Lesson 2: Proximity to amenities is important for OCR projects

Among the 15 top performers, eight are located in the Outside Central Region (OCR). The eight condos are Lentor Central Residences, Springleaf Residence, Faber Residence, The Orie, ParkTown Residence, Bagnall Haus, Elta and Canberra Crescent Residence.

Among these eight OCR condos, ParkTown Residence is the only development with more than 1,000 units. To date, 1,117 sale caveats have been lodged for the 1,193-unit project, making it the top performer in terms of the number of units sold.

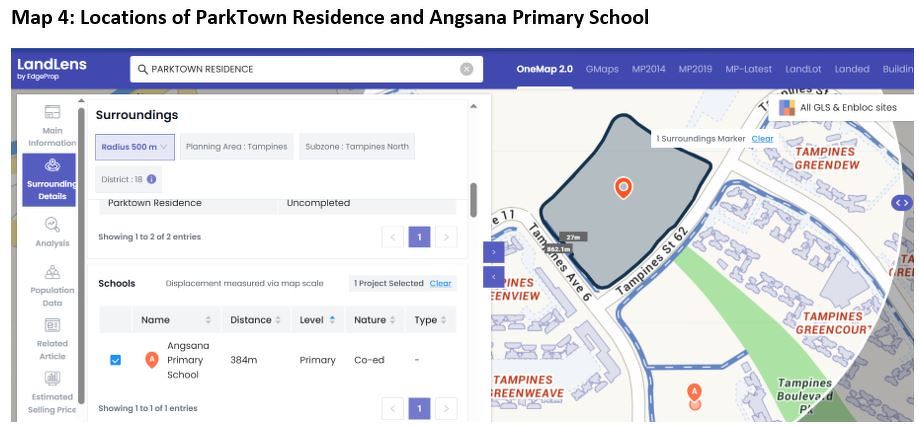

ParkTown Residence will be Tampines’ first integrated development, which may have contributed to its popularity among homebuyers. In addition to being integrated with the upcoming Tampines North MRT Station and a bus interchange, the development will also comprise a mall, a community club and a hawker centre.

ParkTown Residence is also a short drive from the Tampines Expressway. Additionally, eight primary schools are within a 2km radius, namely Angsana Primary School, Elias Park Primary School, Gongshang Primary School, Meridian Primary School, Park View Primary School, Poi Ching School, St Hilda’s Primary School and Tampines North Primary School (see Map 4).

Source: EdgeProp LandLens

Interestingly, two of the OCR condos are located in District 26. Lentor Central Residences is a short walk from Lentor MRT Station, while Springleaf Residence is located near Springleaf MRT Station. Demand for both projects can be attributed to their close proximity to MRT stations on the Thomson–East Coast Line (TEL). The completion of the majority of TEL stations has been a game changer, as residents living near the line now enjoy significantly shorter commute times to the city centre. Hence, the strong take-up rates for Lentor Central Residences and Springleaf Residence are hardly surprising.

Furthermore, Lentor Central Residences is a short walk from Lentor Mall, which opened last month. Meanwhile, Springleaf Residence is close to a number of shops and eateries along Upper Thomson Road and just one MRT stop away from Lentor Mall.

Lesson 3: Well-established neighbourhoods attract demand

The Orie and Elta are located in the well-established residential neighbourhoods of Toa Payoh and Clementi, respectively. As such, both upcoming condos are surrounded by a wide variety of amenities.

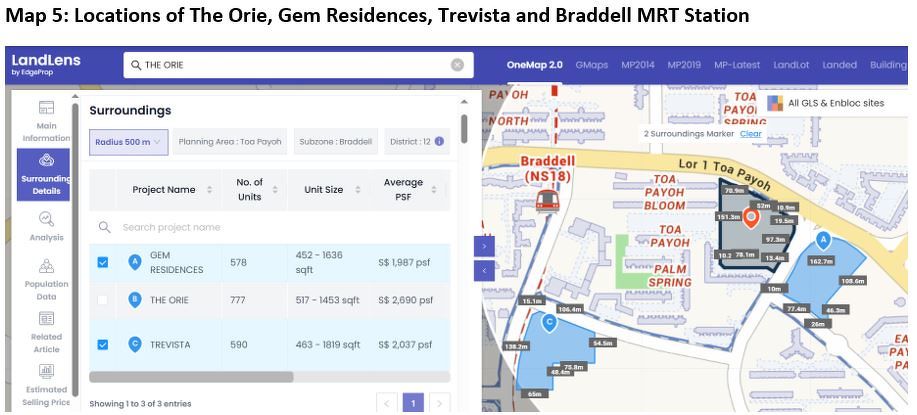

The Orie is a short walk from Braddell MRT Station, as well as Toa Payoh West Market and Food Centre (see Map 5). Schools within a 1km radius of the upcoming condo include First Toa Payoh Primary School, Kheng Cheng School, Pei Chun Public School, Beatty Secondary School, Raffles Girls’ School (Secondary) and Raffles Institution (secondary and junior college).

Source: EdgeProp LandLens

Despite the numerous nearby amenities, there are only two condos—Gem Residences and Trevista—within walking distance of The Orie, as most of the nearby residential properties are HDB flats. Hence, upgraders from nearby HDB flats have limited choices if they wish to continue living in the same neighbourhood.

At the time of writing, 191 profitable transactions and only one unprofitable transaction have been recorded for the 99-year leasehold Gem Residences. Profits range from approximately $6,000 to $896,000, while the loss from the sole unprofitable transaction was $139,000.

Meanwhile, the 99-year leasehold Trevista reported 488 profitable and 15 unprofitable transactions. Profits range from approximately $2,800 to $1.825 million, while losses range from breakeven to $170,000. Despite having more unprofitable transactions compared to Gem Residences, Trevista recorded five transactions with profits exceeding $1.5 million (see Table 2). In contrast, no transactions from Gem Residences yielded million-dollar profits.

Notably, Gem Residences and Trevista are relatively new, having obtained their temporary occupation permit (TOP) in 2019 and 2011, respectively. Their age, coupled with numerous nearby amenities, could explain why the majority of their sale transactions have been profitable, which in turn drives up demand for condos in the vicinity.

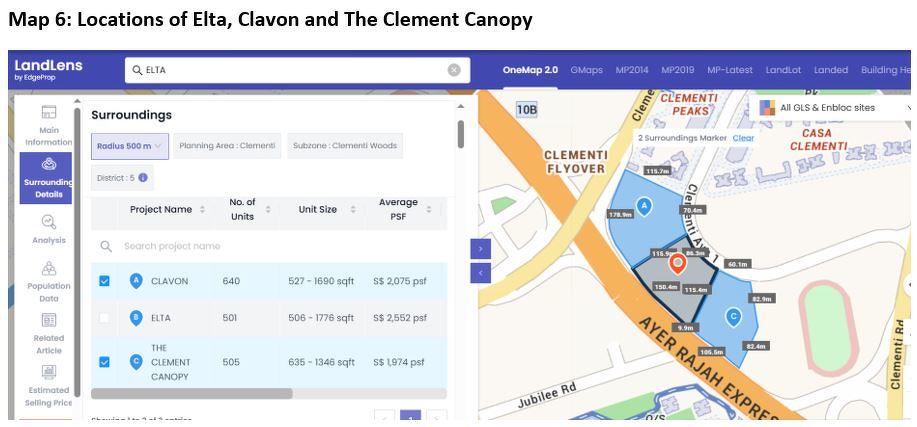

Elta is a short walk from West Coast Plaza, as well as Clementi Sports Centre and Swimming Complex. The upcoming condo is also a short drive from the Ayer Rajah Expressway. However, the main appeal of Elta is likely its close proximity to Nan Hua High School and NUS High School of Mathematics and Science (secondary and junior college). Other schools within a 1km radius include Clementi Primary School, Pei Tong Primary School, Kent Ridge Secondary School and New Town Secondary School.

Like The Orie, there are a limited number of nearby condos. The two developments within a 500m radius of Elta are Clavon and The Clement Canopy (see Map 6).

Source: EdgeProp LandLens

Clavon obtained its TOP in 2024, which could explain why the condo has not recorded any unprofitable transactions. Its 157 profitable transactions yielded profits ranging from approximately $58,000 to $1.068 million.

At the time of writing, its record-high profit of $1.068 million is the only million-dollar transaction for the condo. Including this, five transactions with profits exceeding $900,000 have been reported for the 99-year leasehold condo. (see Table 3).

In comparison, The Clement Canopy has reported 153 profitable transactions and no unprofitable ones. However, profits for the 99-year leasehold condo are lower, ranging from $102,000 to $906,000. The transaction that yielded the highest profit is the only one to exceed $900,000.

Like Clavon, The Clement Canopy is also fairly new. Having obtained its TOP in 2019, the condo is less than 10 years old, which could explain its strong profitability.

Lesson 4: Experience and reputation of developer play a part

Among the top performers, 10 achieved take-up rates exceeding 80% during the launch month. An examination of the developers behind these successful condo launches reveals that many were developed by consortiums that include experienced developers with extensive track records (see Table 4). The names that frequently appear include CapitaLand, UOL, GuocoLand and CDL.

CapitaLand is a well-known developer with numerous projects across the globe, including in China, Australia, Japan, the US and the UK. In Singapore, they have developed many projects spanning the entire property spectrum. Some of their more prominent past residential projects include CanningHill Piers, One Pearl Bank, Sengkang Grand Residences, The Interlace and The Orchard Residences.

UOL is part of the consortium that developed three of last year’s hottest new condos, namely Skye at Holland, ParkTown Residences and UpperHouse at Orchard Boulevard. Also well-established, it has developed many of Singapore’s well-known condos, including Watten House, Amo Residence, MeyerHouse and Clavon.

GuocoLand is known as the unofficial master developer of Lentor after snapping up the majority of Government Land Sale sites near Lentor MRT Station. Aside from its well-received residential projects in Lentor, their track record of condos in Singapore includes Martin Modern, Midtown Modern, Leedon Residence and Wallich Residence.

CDL is a reputable developer with numerous well-known residential projects under its belt. These include Newport Residences, which achieved a take-up rate of 57% at its launch earlier this month. CDL’s completed residential projects include Haus on Handy, Gramercy Park and South Beach Residences.

Lesson 5: Slow start does not always spell doom

Developers should take heart if their developments do not achieve an outstanding take-up rate at launch because a slow start does not necessarily spell doom.

A good example is Bloomsbury Residences, which achieved a take-up rate of 25.1% during its launch in April last year. However, the number of caveats lodged to date indicates that the take-up rate has since surged to 70.1% for the 358-unit development.

Additionally, the average new sale price for the condo increased by 4.2%, from $2,461 psf in April 2025 to $2,564 psf in January (see Chart 1).

Conclusion

An examination of condos that achieved stellar sales performance during their launch month indicates that such developments share several commonalities. A well-located condo within walking distance of an MRT station and a major mall will always find favour with buyers. Add bonus points if the condo is part of an integrated or mixed-use project.

Condos in the Central Region are popular with buyers because of their proximity to the city centre. Additionally, the prestige of having an address in a premier neighbourhood cannot be discounted. However, OCR condos can still appeal to buyers if they are near amenities such as MRT stations, shops, eateries and schools.

The track record and reputation of the developer behind a residential project also cannot be underestimated. Experienced developers with extensive track records can provide homebuyers with greater assurance of quality workmanship, thoughtful design and timely completion.

Finally, developers should take heart if their projects do not achieve resounding success at launch. Some projects launch to limited fanfare but see a significant improvement in take-up rates at a later date.

Check out the latest listings for Skye At Holland, Lentor Central Residences, Lyndenwoods, Penrith, River Green, Parktown Residence properties

Ask Buddy

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search