Singapore private home prices up by a modest 0.6% in 4Q2025 while rents dip 0.5%

On a full-year basis, private home prices were up 3.3% in 2025, led by landed properties which saw prices jump 7.6%. (Photo: EdgeProp Singapore)

Prices of private residential properties, excluding executive condominiums or ECs, in Singapore inched up by 0.6% quarter-on-quarter in the October-December period in 2025, a tad slower than the 0.9% growth in the July-September period, data released by the Urban Redevelopment Authority (URA) on Jan 23 showed.

For the whole year, private home prices were up 3.3% in 2025, moderating from the 3.9% increase in 2024 and marking the smallest increase in a year since 2020.

The updated overall private residential price index is slightly lower than the flash estimates released by URA earlier this month, which had shown a 0.7% q-o-q rise for the fourth quarter and a 3.4% jump for the year.

Mohan Sandrasegeran, SRI head of research and data analytics, said: “Importantly, this moderation has taken place alongside an expansion in land supply rather than in an environment of tightening availability, suggesting that price stabilisation has been driven by structural supply measures rather than any weakening in underlying housing demand.”

The easing trend has unfolded against a backdrop of a sustained ramp-up in the supply of private housing via the government land sales (GLS) programme since 2022. A significant supply pipeline of about 57,000 private residential units including ECs is expected to be completed in the next few years, URA noted. This includes the sustained high Confirmed List supply to be released in the first half of 2026, which is 50% above the average Confirmed List supply for the GLS programmes over the past decades.

The steady increase in GLS sites released under both the Confirmed and Reserved Lists has strengthened the pipeline of future private housing and improved overall supply visibility, noted Sandrasegeran.

“This calibrated approach has helped anchor market expectations, supporting a transition from the strong post-pandemic rebound toward a more balanced and sustainable growth phase,” he added.

Landed homes drive price momentum

The landed segment led the price growth in 4Q2025 as prices of landed properties rose 3.4%, gaining pace from the 1.4% increase in 3Q2025. On a full-year basis, landed home prices jumped by 7.6% — much faster than the 0.9% uplift seen in 2024.

This marks the fourth consecutive quarter of rising prices for the landed segment. A possible factor could be the higher prices of non-landed properties prompting some condo owners to take the opportunity to upgrade to a landed home, said Marcus Chu, CEO of ERA Singapore.

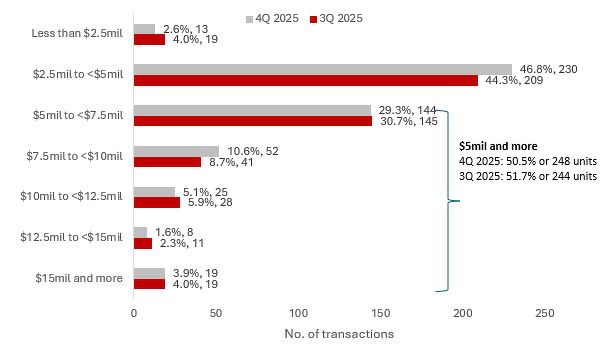

Price quantums of transacted landed homes in 3Q2025 vs 4Q2025:

Source: URA (as of Jan 21, 2026), ERA Research and Market Intelligence.

Based on caveats lodged, landed home transactions rose 4.0% q-o-q to 491 transactions in the last three months of 2025, according to ERA Singapore. This brings the year’s total to 1,852 transactions, 11.2% more than the whole of 2024.

The Outside Central Region (OCR) and the Rest of Central Region (RCR) saw an increase in the number of landed property deals in 4Q2025, reversing the trend in the previous quarter. “Buyers could have looked at homes further from the city centre as they balanced between their locational preference, spatial needs, and affordability,” ERA’s Chu commented.

On the other hand, the Core Central Region (CCR) had fewer transactions, amid higher prices as buyers and sellers “faced an impasse” on pricing, he said. This comes as sellers of landed homes in the CCR, typically with higher holding power, are usually less inclined to reduce their prices, according to Chu.

In the non-landed segment, prices were almost flat, falling by 0.2% in the quarter, reversing from the increase of 0.8% in the previous quarter.

Within the CCR, non-landed properties’ prices dropped by 3.5% in the October-December period last year, versus a gain of 1.7% in the previous quarter. In the RCR or city fringe, prices of non-landed homes inched up by 0.7%, slightly higher than the 0.3% increase in the third quarter. As for the OCR or suburbs, prices of non-landed properties rose 1.0%, compared with the 0.8% increase in the previous quarter.

For the whole of last year, non-landed private home prices were up 2.3% islandwide. In the CCR, RCR, and OCR, price gains were recorded at 1.9%, 1.6%, and 3.2% respectively across 2025.

Newmark’s head of research, Wong Shanting, commented that several ultra-luxury new sale transactions in the CCR helped lift overall per square foot (psf) pricing in the first half of 2025.

These included large-format, freehold developments such as Park Nova, which recorded a median price of $5,366 psf, and 21 Anderson at $4,999 psf, both of which are sought after by high-net-worth buyers. Separately, Skywaters Residences, a 99-year leasehold project in the central business district, saw two units sold at a median price of $6,171 psf, Wong said.

Rents of private housing decrease in 4Q2025

In the rental market, private home rents recorded their first decline since 2Q2024, with the overall private residential rental index falling by a marginal 0.5% in the final quarter of 2025, versus an increase of 1.2% in the previous quarter, based on the updated real estate statistics released on Jan 23.

This moderation occurred even as market fundamentals appeared to tighten significantly, said Chia Siew Chuin, JLL’s head of residential research, research and consultancy, Singapore. The islandwide vacancy rate fell to 6% in 4Q2025, supported by robust net new demand of 5,027 units which far outstripped the low net new supply of just 1,696 units during the quarter.

“This suggests that while underlying demand for rental accommodation remains healthy, the market as a whole is reaching an affordability ceiling, preventing the tight supply conditions from translating into further rental growth,” Chia said.

Across the full year, the rental index went up by a modest 1.9%, a reversal of the decrease of 1.9% in 2024. Rental volume was also higher on an annual basis with 89,376 rental contracts, up 3.4% from 2024.

In the landed segment, rents increased by 0.4% for the whole of 2025.

Non-landed properties’ rents islandwide rose by 2.3% for the year. Rentals of CCR, RCR, and OCR non-landed homes were up by 2.5%, 2.8% and 1.3% respectively in 2025.

Tricia Song, CBRE head of research, Singapore and Southeast Asia, noted that while the supply situation remains conducive for landlords in 2026, it is gradually shifting in favour of tenants. This comes as 6,123 units were completed in 2025, about 28% fewer than 2024’s 8,460 units, and a similar number of completions is expected in 2026 at 6,083 units.

Projects that have recently obtained their temporary occupation permit (TOP) will give tenants more choices, and it may take longer to rent out a vacant unit as tenants become more selective and landlords compete to secure good tenants, Song said.

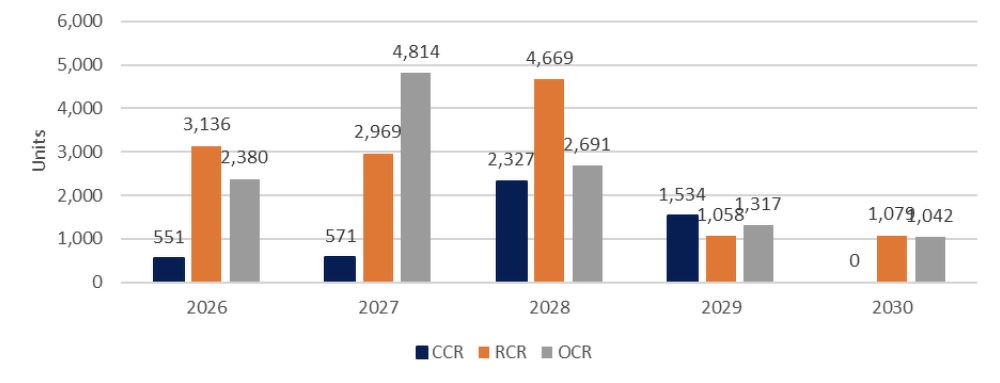

Upcoming supply of private residential properties under construction:

Source: URA, Huttons Data Analytics as of Jan 23, 2026.

Resale transactions steady, sub-sales subdued

When it comes to transaction volumes, the primary market saw developers selling more than 10,800 new private homes (excluding ECs) during the year, surging to the highest annual sales volume since 2021.

This tally from 2025 alone nearly matches the annual average of 10,974 new homes sold from 2019 to 2021, prior to significant market cooling measures, said Chia from JLL.

SRI’s Sandrasegeran noted the strong rebound in new private home sales in 2025 across all market segments, which marked a clear recovery in primary market activity after the more subdued conditions seen in the year before. This improvement was underpinned by several supportive factors, including the ramp up in housing supply from earlier awarded GLS sites, more stable interest rate conditions, and a gradual return of buyer confidence.

“Together, these factors helped reactivate demand and supported healthier transaction momentum across a wider range of projects and price points,” Sandrasegeran said.

Developers’ new home sales rebounded in 2025:

Source: SRI Research, URA Realis.

In contrast to the dynamic primary market, transaction volumes in the secondary market remained largely stable last year.

Huttons Asia CEO, Mark Yip, said the resale market saw lower volume in 4Q2025 as buyers were drawn to new launches that were priced close to resale prices. Resale transactions fell 9.1% q-o-q in the quarter to 3,529 units.

Meanwhile, total resale activity closed the year at 14,622 units, up 4.0% from 2024.

JLL’s Chia said this consistency highlights the resilience of the resale segment, which serves as the bedrock of the housing market for genuine homebuyers. Resale demand has been driven by buyers with immediate housing needs, those seeking properties in established locations with limited new supply, and families in search of the larger living spaces often found in older developments, she added.

As for sub-sales, there were 1,055 transactions in 2025, making up about 6.7% of total secondary-market deals for the year. Sub-sale volume decreased by about 26.1% from 1,428 in 2024.

Private home transactions (excluding ECs) by type of sale:

Source: URA, ERA Research and Market Intelligence

The proportion of sub-sales and total sales was among the lowest in recent years. PropNex chief executive Kelvin Fong said that falling sub-sales, which are commonly seen as a proxy for property speculation, may indicate that buying activity is increasingly driven by owner-occupiers and purchasers who take a longer-term view, which will be positive for market stability.

Fewer sub-sales could also mean that buyers have stronger financial holding power, or face less financing stress due to high interest rates, Fong added.

Chia noted: “A key indicator of market health was the subdued level of sub-sale transactions, which remained negligible despite the strong underlying buying sentiment.” JLL sees this as a direct result of the seller’s stamp duty (SSD) framework, which effectively curbs speculative activity, as well as the recent SSD adjustments, including the extension of the holding period, that have continued to deter property “flipping”.

Outlook for private residential market in 2026

Cushman & Wakefield’s head of research for Singapore and Southeast Asia, Wong Xian Yang, said that barring new cooling measures, he is “cautiously optimistic” that private residential prices could grow by 2% to 4% year-on-year in 2026, supported by low borrowing costs, increasing land prices and resilient buyer confidence, underpinned by still-low unemployment rates.

Affordability concerns could play a larger role in shaping upgrading decisions, particularly as private home prices continue to increase, he added.

Fong from PropNex described 2025 as "a relatively good place for the market", where prices rose more slowly despite stronger sales, while rentals recovered slightly amid healthy leasing demand.

"A combination of these indicators suggests that the market could be in a 'Goldilocks' phase where it is not too cold, nor too hot but balanced and just right," Fong said. That the robust sales in 2025 did not lead to rapid price spikes also reflects developers’ discipline in pricing units and their focus on driving healthy take-up rates at launch with well-calibrated prices in a highly value-conscious market, he added.

PropNex expects the stability and sales momentum from last year to spill into 2026. The continued moderate interest rates will help to anchor confidence and improve affordability, encouraging genuine buyers to enter the market, according to Fong. He noted that some 2-year fixed-rate home loan packages are going at 1.4% to 1.5% per annum currently, markedly lower than more than 4% per annum interest rates at the end of 2022, which can help to lighten debt burdens.

Christine Sun, chief researcher and strategist of Realion (OrangeTee & ETC) Group, projects private home prices to rise moderately this year, without significant growth as the number of new private home sales are expected to fall in tandem with fewer project launches.

Further, more than half of the new launches in 2026 will be in suburban areas, where prices tend to be lower than in the other market segments of CCR and RCR. The increase in completed properties may place some downward pressure on prices as well, Sun added.

Realion thus predicts the net effect may lead to prices going up moderately by 2.5% to 4.5%, which will be on par with the 3.3% growth in 2025 and 3.9% in 2024.

Wong from Newmark said that while key drivers of housing demand remain, several pressure points are beginning to emerge. Elevated land costs may narrow private housing affordability for some HDB upgraders, while persistently strong sales of new homes could raise the likelihood of policy intervention. “Nonetheless, these risks remain manageable against the backdrop of solid market fundamentals, including prudent buyer behaviour and a well-regulated housing environment,” She added.

In SRI’s view, private residential property prices in Singapore could continue to grow this year, albeit at a gentler pace than in 2025. With a larger pool of completions, a healthy new launch pipeline, and gradually easing financial conditions, private home prices are expected to rise by about 2.5% to 4.0% for the whole of 2026, said Sandrasegeran.

He added that the overall private residential property market in Singapore will likely remain “resilient and orderly” this year, with buyers staying price conscious while developers continue to pace launches strategically in line with demand.

For more news and analysis, read our weekly e-paper. Prefer a print copy? Get it delivered to your home every Monday.

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search