Private credit gains ground in Asia Pacific real estate

Private credit provides funding for over a quarter of residential construction in Australia, with a preference for build-to-sell assets, according to CBRE. (Photo: Unsplash)

Private credit is gaining traction in Asia Pacific (Apac) real estate as investors — including institutional investors, family offices and ultra-high-net-worth individuals — explore new opportunities while property developers adapt to rising costs.

This comes as investors are looking to diversify their ways of accessing real estate exposure and equity returns are coming under pressure, making debt positions more attractive, says global real estate investment manager LaSalle Investment Management, a subsidiary of JLL.

Moreover, property developers in the region are shifting towards smaller-scale projects such as refurbishment, creating financing needs that fall outside conventional bank lending parameters.

Inflation has driven up construction costs in major Apac real estate markets — up more than 30% above pre-pandemic levels in Japan, 35% in Singapore, 33% in South Korea and 23% in Hong Kong, LaSalle notes in the Apac chapter of its ISA Outlook 2026 report.

This has made it “substantially more difficult” for developers to achieve viable project economics, the report adds. In many instances, land values have not corrected sufficiently and rents have not increased enough to offset escalating build costs.

Developers are therefore rethinking their approaches, shifting from large-scale redevelopment to smaller-scale renovation and conversion strategies. This adaptation is creating new openings for private credit.

Filling gaps in a shifting landscape

Apac’s traditional lending environment remains deep, heavily dominated by traditional, conservative bank financing.

The likes of transaction finance and senior loans for core investments — involving stabilised assets that generate consistent income with very low risk — therefore remain "the playground of the big institutions", says Eduardo Gorab, LaSalle’s Asia Pacific co-head of research and strategy, during a media roundtable discussing the report findings.

"That leaves some room for non-bank lenders to fill less senior pieces of the capital stack, or fund higher risk activities that are less attractive to banks, like construction or transitional assets," he adds.

Where private credit finds opportunity is in more flexible forms of real estate finance and situations with higher risk profiles, including the types of smaller-scale, adaptive projects that developers are increasingly pursuing. This helps maintain project momentum and opens new channels for capital deployment.

Private real estate credit players are stepping in, particularly in Australia and South Korea, to provide development loans, mezzanine financing, structured credit and transitional financing, LaSalle notes.

Likewise, global property consultancy Knight Frank sees private credit filling targeted gaps where banks are less active, such as in higher-risk developments, refinancing stress, cross-border transactions, or cases requiring leverage, while banks continue to provide straightforward real estate loans.

Knight Frank describes private credit in Apac as playing a “complementary and cyclical” role alongside the banking sector, instead of displacing banks in the way it does in the West. “In fact, many private credit funds in the region rely on bank financing themselves to achieve ‘an extra turn’ on returns,” the consultancy notes in its report.

The opportunities are expected to be selective, arising from cyclical dislocations, market stress, or borrower’s needs for more flexible capital, Knight Frank adds.

Varying prospects

Market conditions for alternative lenders differ considerably across the region.

Sydney, Australia. Major banks have pared back exposure to commercial real estate in the country. (Photo: Unsplash)

Australia’s private credit market, for example, has expanded significantly over the past decade as major banks pared back their exposure to commercial real estate.

Real estate in Australia is funded by about A$50 billion ($44.6 billion) of private credit. This is forecast to grow to around A$90 billion by 2029, according to commercial real estate services and investment firm CBRE.

Private credit provides funding for over a quarter of residential construction in Australia, with non-bank lenders showing a strong preference for residential build-to-sell assets over larger-ticket retail and data centres, CBRE says in a recent insights report.

In South Korea, private credit is entering niche but high-growth areas such as logistics and data centres. These are segments where timelines, complexity and sponsor requirements are better served by agile, non-bank financing, Knight Frank notes.

By contrast, in Japan, private credit “will not be an easy strategy to do”, says Makoto Sakuma, Asia Pacific co-head of research and strategy at LaSalle, at the roundtable. He points to the strong position of domestic banks and intense inter-bank competition in Japan. “Even with interest rates going up, banks will still have to fill a portion of their portfolio with real estate,” Sakuma adds.

Knight Frank similarly notes that Japan’s stable banking sector and ultra-low rates make entry harder for private credit players, though mezzanine and bespoke financing for sponsor-backed projects are starting to surface, particularly where tailored structures are needed.

Cautious development amid cost pressures

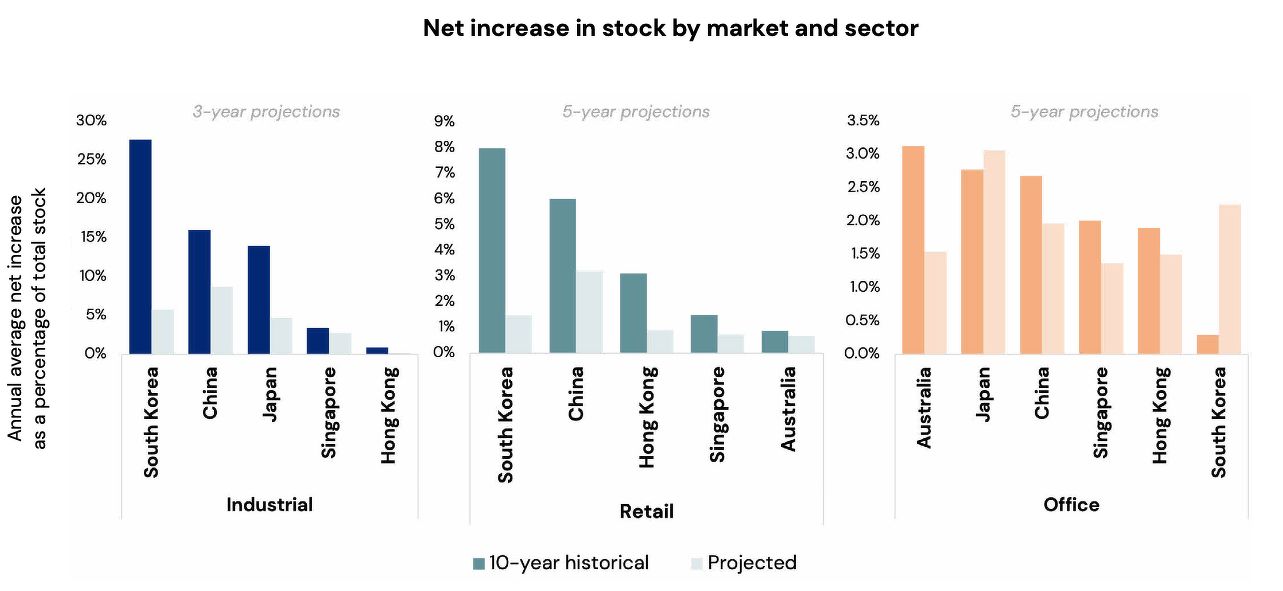

Projected net increases in industrial, retail and office stock in Apac are expected to fall below their 10-year averages across most markets, with the exception of the office sector in Japan and South Korea.

The region’s shrinking supply pipelines reflect developers’ caution amid more modest demand, cost inflation and tighter financing conditions, according to LaSalle’s ISA Outlook 2026.

Supply pipelines expected to ease:

Source: LaSalle Investment Management; Ichigo Real Estate Service, JLL REIS, as of 3Q2025.

Note: Projected net increase for Australia office and retail and Japan industrial are based on total completions.

That said, development and redevelopment of real estate are not disappearing entirely, but simply becoming more selective and requiring disciplined capital use.

“Opportunities remain in segments with clear rental growth potential or favourable long-term demand drivers, such as hospitality, residential and living sector, as well as logistics in selected submarkets,” LaSalle notes.

It adds that in an environment of rising costs and narrowing margins, adaptability — in both asset strategy and financing — will define success in Apac real estate.

For more news and analysis, read our weekly e-paper. Prefer a print copy? Get it delivered to your home every Monday.

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search