Retail market holds firm amid stronger consumer sentiment and new-to-market entrants

Stronger consumer spending, combined with the arrival of new-to-market entrants, is expected to support rental growth through the end of the year (Photo: Samuel Isaac Chua/EdgeProp Singapore)

Improved consumer spending and an influx of new-to-market entrants are expected to drive rental growth in Singapore’s retail property market through year-end. URA data showed that retail rents continued to rise steadily in 3Q2025, growing 0.9% q-o-q, matching the same pace of growth recorded in the previous quarter.

Ethan Hsu, head of retail at Knight Frank Singapore, notes that a combination of structural and cyclical factors underpinned the “robustness” observed in 2025. He points to resilient domestic consumption driven by a full economic reopening and steady market conditions, alongside a rebound in tourism that has supported demand from luxury brands, flagship retailers and destination-led F&B concepts.

The tailwinds led to a positive net absorption of 54,000 sq ft of private retail space islandwide in 3Q2025, reversing two consecutive quarters of negative net absorption. CBRE’s head of research for Singapore and Southeast Asia, Tricia Song, anticipates net absorption to remain positive in the last quarter. “The last quarters of the year have typically seen strong positive net absorption (at least 100,000 sq ft), which can be attributed to positive retailer sentiments on the year-end festive season,” she adds.

Supporting this view, Alan Cheong, executive director of research and consultancy at Savills Singapore, observes that about 247,500 sq ft of retail space will be completed in 4Q2025, which he expects to come from Dunearn Village, an upcoming mall on Dunearn Road by Tuan Sing Holdings at the site of the former Link@896, as well as the retail podium at GuocoLand’s Lentor Modern.

“As these two retail developments each have significant retail space, each carries enough clout in its marketing efforts and should draw in demand,” says Cheong. To that extent, he believes net absorption in 4Q2025 could potentially exceed the 54,000 sq ft recorded in 3Q2025.

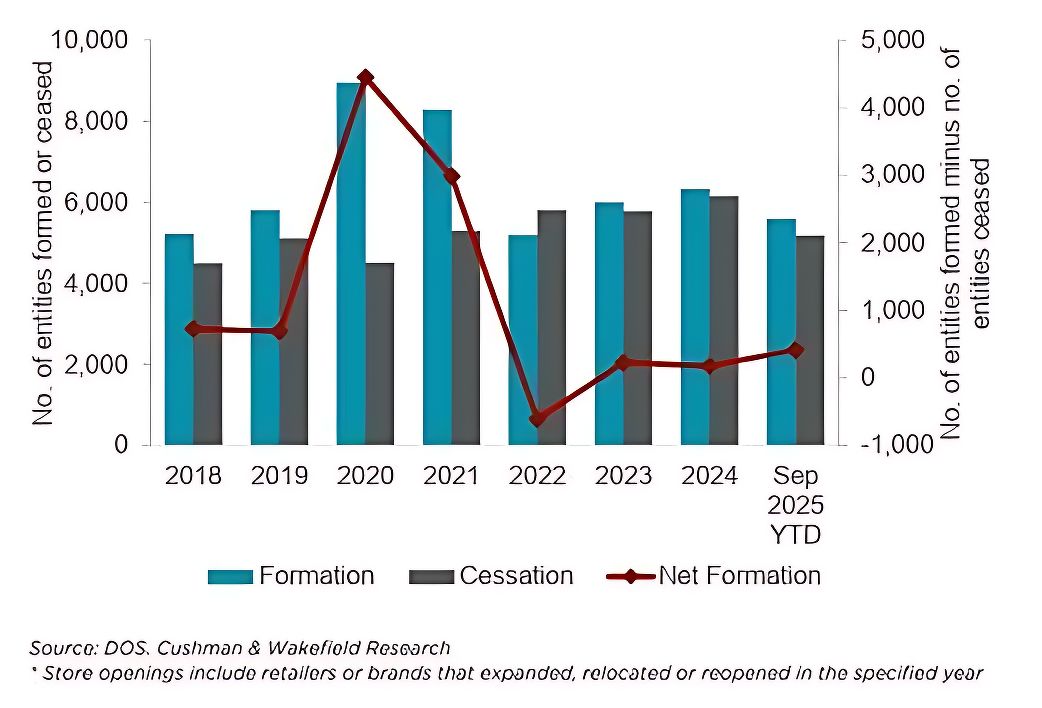

‘Regular tenant churn’

While steady demand has helped bolster retail rents, this year has seen a wave of closures and exits. The first half of the year saw a spate of well-known F&B brands, such as Eggslut, Prata Wala and Burger & Lobster, shutter. More than 2,400 F&B outlets closed in the first 10 months of 2025, according to statistics shared by Deputy Prime Minister Gan Kim Yong in Parliament.

For Lee Chau Hwei, a partner at Withers Khattar Wong, surging rents are a contributor to the closures. The corporate real estate lawyer estimates that retail rents have increased by approximately 10%–30% since the onset of the Covid-19 pandemic, as investors and landlords sought to recoup pandemic-related losses. In addition, manpower and other operating costs also remain challenging for retailers.

Outside the F&B space, notable exits include Cathay Cineplexes, which ceased operations in September, and indie cinema The Projector. Departmental store Isetan, which shuttered its Tampines Mall outlet in November, announced on Dec 17 that it would close its Nex location next year, leaving just one outlet at Orchard Road.

“Given the challenging retail operating environment, the Singapore market continues to experience regular tenant churn,” says Wong Xian Yang, head of research for Singapore and

Southeast Asia at Cushman and Wakefield (C&W). Despite this, he notes that while some tenants have right-sized or exited, vacant spaces are “typically backfilled swiftly”, underpinned by expanding retailers and new-to-market brands.

Joan Chen, head of retail services for Singapore at CBRE, adds that improving consumer sentiment, amid better-than-expected GDP growth, a resilient labour market and an ongoing tourism recovery, has imbued retailers with greater confidence. “Consequently, despite some closures and consolidation, which are more pronounced in certain trades, we have observed strong leasing activity across diverse sectors, including F&B, services and fashion. As of 3Q2025, the islandwide retail space vacancy rate stood at 6.9%, down from 7.1% in 2Q2025, according to URA data.

Net formation of entities in retail trade (Source: DOS, Cushman & Wakefield Research)

International appeal

This year, several overseas retailers made their debut in Singapore across various retail sectors. In the F&B landscape, Orchard Central saw the opening of the popular Australian self-serve yoghurt chain Yo-Chi, while the American fast-food restaurant chain Chick-fil-A opened its doors at Bugis+ earlier this month.

Knight Frank Singapore’s Hsu attributes Singapore’s appeal to international brands to its strong consumer base and position as a trusted gateway to Southeast Asia. “In 2025, Chinese F&B groups demonstrated especially strong interest, using Singapore as both a brand-building platform and a regional springboard,” he adds.

Several overseas retailers, including popular Australian self-serve yoghurt chain Yo-Chi, made their debut in Singapore this year (Photo: Samuel Isaac Chua/EdgeProp Singapore)

Chengdu-based beverage shop chain Chagee, which closed all its Singapore stores in January 2024, reentered the market just eight months later. It now operates over 20 stores across Singapore, with upcoming stores slated to open at Suntec City and Our Tampines Hub. Other Chinese F&B brands that entered the market this year include bakery cafe Ruxu and hotpot chain Shu Da Xia.

Beyond F&B, new entrants in Singapore span lifestyle stores such as KKV and OH!SOME, fashion. Brands such as Redchic and 2nd Street, athleisure favourites On and Alo, and beauty brands Joocyee and Judydoll.

“Notably, some e‐retailers are expanding into brick‐and‐mortar spaces to differentiate themselves in an increasingly competitive e‐commerce market,” says C&W’s Wong. For instance, online trading platform Moomoo Singapore opened physical stores at 313@Somerset and Jem this year, with another slated to open at Parkway Parade.

Chagee now operates over 20 stores across Singapore (Photo: Samuel Isaac Chua/EdgeProp Singapore)

Limited pipeline and low vacancy to support rental upside

Looking ahead, Wong highlights that new retail space will be limited over the coming years. Between 2026 and 2029, new supply is estimated to average around 300,000 sq ft annually, less than half the historical average of 800,000 sq ft per year over the last decade, he says. Of this upcoming supply, Orchard Road is expected to account for just 10%, with the bulk concentrated in other city locations (49%) and suburban malls (41%).

In 2026, retail spaces expected to be completed include CanningHill Square, the retail component at City Development’s CanningHill Piers integrated development in Clarke Quay

and Parc Point, a neighbourhood centre with retail options in Tengah. The developments will offer around 87,000 sq ft and 75,000 sq ft of retail space, respectively.

Against this backdrop of constrained new supply, CBRE’s Song anticipates consumer spending will remain resilient, bolstered by improving tourist arrivals driven by new attractions such as Minion Land and the Singaporean Oceanium, as well as a steady pipeline of MICE (meetings, incentives, conferences, and exhibitions) events and concerts.

Chinese beauty brands such as Judydoll and Joocyee have opened physical stores at Wisma Atria (Photo: Samuel Isaac Chua/EdgeProp Singapore)

In turn, this should support demand for retail spaces, especially in prime locations. “Coupled with below-historical-average supply in the next three years, islandwide prime rents are forecasted to grow by 1% to 2% in 2026,” Song predicts.

Savills’ Cheong echoes her views. “For 2026, we believe that due to the continued recovery in tourism, rents for prime malls along Orchard Road may rise by up to 3% y-o-y while suburban ones may go up by 1% y-o-y as outbound travel continues unabated.”

Knight Frank’s Hsu believes that brands will continue to expand in Singapore next year, though operators may grow more selective in their expansion, given Singapore’s high operating costs. “A two-tier market is solidifying: international brands competing for premium sites at high rent thresholds, while secondary markets cater increasingly to value-driven local operators,” he adds.

He anticipates prime retail rents to rise by approximately 2% to 4% in 2026, while secondary malls could observe more modest growth or even flat performance.

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search