Suburban projects, mixed-use developments take centrestage in new launches of 2026

Tengah HDB town will see the debut of its first private condo project this year at Tengah Garden Avenue (Photo: Samuel Isaac Chua/EdgeProp Singapore)

Ask Buddy

After a year marked by a surge in new price growth, Singapore’s residential market is heading into 2026 on a firmer and more balanced footing. Developers have been more aggressive in replenishing their land bank and bringing projects to market, while buyers have become increasingly price-sensitive and selective.

Against this backdrop, the coming year is shaping up to be one led by the suburban market — the Outside Central Region (OCR) — which is set to dominate new supply and sales activity.

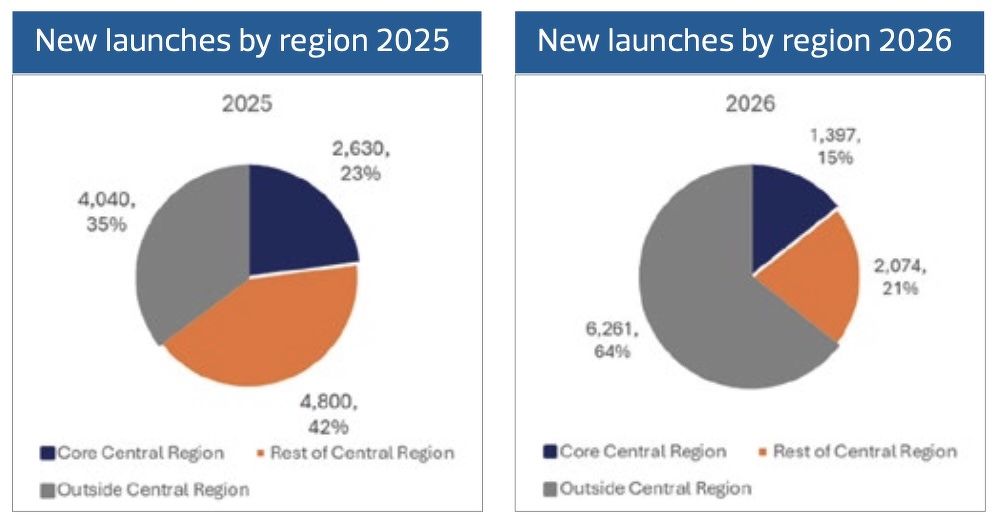

This year, about 11,000 to 11,500 new homes across 27 private residential projects were launched — the highest number of units released by developers since 2013, and 73% more than in 2024, says Mark Yip, CEO of Huttons Asia.

Get the latest details on available units and prices for Narra Residences

Meanwhile, developers’ sales of private homes for the whole of 2025 are likely to come in at around 11,000 units (excluding executive condominiums). This would mark the highest annual sales volume since 2021, when 13,027 units were sold, notes Yip.

Huttons Data Analytics projects 3%–4% price growth in 2025. “The market is more stable now, with price growth decelerating for the fourth consecutive year — from 10.6% in 2021 to an estimated 3% in 2025,” observes Yip.

Source: Huttons Data Analytics

Launch pipeline dominated by OCR supply

Marcus Chu, CEO of ERA Singapore, anticipates about 20 private residential development launches in 2026, including one landed housing project. Meanwhile, PropNex CEO Kelvin Fong is also projecting about 20 new launches in 2026, comprising an estimated 8,400 units for sale. Of these, about 65% will be in the OCR, 19% in the city fringe or Rest of Central Region (RCR), and the remaining 16% in the prime districts and city centre, or Core Central Region (CCR).

PropNex expects the OCR to be the key driver of developers’ sales next year, partly due to the larger share of new launches in the submarket. “In addition, demand for OCR homes is often driven by their greater affordability, family-friendly layouts, and sustained interest from HDB upgraders,” adds Fong.

Huttons, meanwhile, expects 22 new private residential launches in 2026, with an estimated 9,732 units. The OCR is projected to account for approximately 64% of the total supply. “This is 55% higher than the 4,040 units launched in 2025,” says Yip.

Among the major launches expected next year are SingHaiyi Group’s Bayshore Walk project (815 units); Narra Residences (540 units) at Dairy Farm Walk by Santarli Realty and Apex Asia; Kingsford Group’s 500-unit project at Lentor Garden; and Tengah Garden Avenue (860 units) by Hong Leong Group, GuocoLand and CSC Land Group.

In the RCR, notable launches include the 428-unit project on Dorset Road by UOL Group, Singapore Land Group and Kheng Leong Co (Photo: Samuel Isaac Chua/EdgeProp Singapore)

HDB MOP completions to support OCR demand

The sharp increase in OCR supply will be matched by a 68.9% rise in the number of HDB flats fulfilling their five-year minimum occupation period (MOP) in 2026, notes Huttons — a development expected to underpin upgrader demand.

In the RCR, notable launches include the 428-unit project on Dorset Road by UOL Group, Singapore Land Group and Kheng Leong Co; the redevelopment of Thomson View Condominium into a 1,240-unit project by a joint venture between UOL Group, Singapore Land Group and CapitaLand Development; and the 327-unit Media Circle (Parcel A) project by Qingjian Realty, Forsea Holdings and Hoovasun Holdings. They will collectively add 2,074 units in 2026. This represents a 56.8% reduction from 2025’s level, notes Huttons. With only four new RCR launches scheduled for 2026, the limited supply could spur stronger interest from buyers seeking a balance between accessibility and price, says Chu of ERA.

The CCR, meanwhile, may see about 1,397 units launched in 2026 — 4.8% fewer than in 2025 — according to Yip. Buyer interest is likely to focus on the small pool of freehold redevelopments, with GLS sites such as Dunearn Road and Holland Link also drawing attention from those looking to benefit from the transformation of Bukit Timah Turf City, ERA’s Chu adds. “The scarcity of freehold launches naturally supports stronger sentiment in this segment.”

First-mover advantage in emerging housing precincts

In recent years, the distinctions between regions have become increasingly blurred, observes PropNex’s Fong. “Byers and investors are placing greater emphasis on a project’s specific site attributes rather than its regional classification,” he says.

Projects that could benefit from first-mover advantage include SingHaiyi’s Bayshore Road development, Tengah Garden Avenue, and the Dunearn Road project by Frasers Property and Sekisui House. “These are the first private homes to be launched in the new Bayshore, Tengah, and Bukit Timah Turf City precincts, respectively,” notes Fong. As such, he expects keen interest driven by pent-up demand in these emerging housing areas.

Mixed-use developments in the pipeline for launch next year include Pinery Residences (588 units) in Tampines by Hoi Hup Realty and Sunway MCL (Photo: Samuel Isaac Chua/EdgeProp Singapore)

Spotlight on mixed-use developments

Mixed-use developments could also be in focus next year, says PropNex, with several projects offering commercial components alongside residential.

In the OCR, these include Pinery Residences (588 units) in Tampines by Hoi Hup Realty and Sunway MCL; a mixed-use development at Chencharu Close (about 875 units) in the new Chencharu Town at Khatib by Evia Real Estate, together with Gamuda Land and Ho Lee Group; and a 575-unit project at Lakeside Drive by City Developments (CDL).

In the CCR, upcoming mixed-use projects include River Modern (455 units) by GuocoLand and Newport Residences (246 units) by CDL, while the RCR will see the Media Circle (Parcel A) project. “Notably, most of these projects are located close to, or directly linked to, an existing or upcoming MRT station — enhancing their appeal to buyers who value convenience and transport connectivity,” says Fong.

Potential mega developments (with at least 1,000 units) include the redevelopment of Thomson View, which will yield 1,240 units (Photo: ETC)

Mega projects and EC launches

Potential mega developments (with at least 1,000 units) include the redevelopment of Thomson View, which will yield 1,240 units, and the amalgamation of two Chuan Grove GLS sites by a Sing Holdings–Sunway MCL joint venture, resulting in a single 1,055-unit project.

In the executive condominium (EC) segment, Coastal Cabana (748 units) by a consortium led by Qingjian Realty, and Rivelle Tampines (572 units) by Sim Lian Group, are set for launch in 1Q2026. More EC launches could follow towards the end of the year. ERA’s Chu expects five EC projects to be launched in 2026.

In the executive condominium segment, the 748-unit Coastal Cabana by a consortium led by Qingjian Realty, and Rivelle Tampines (572 units) by Sim Lian Group, is scheduled for launch next month ({Photo: Qingjian Realty)

CCR showing signs of recovery

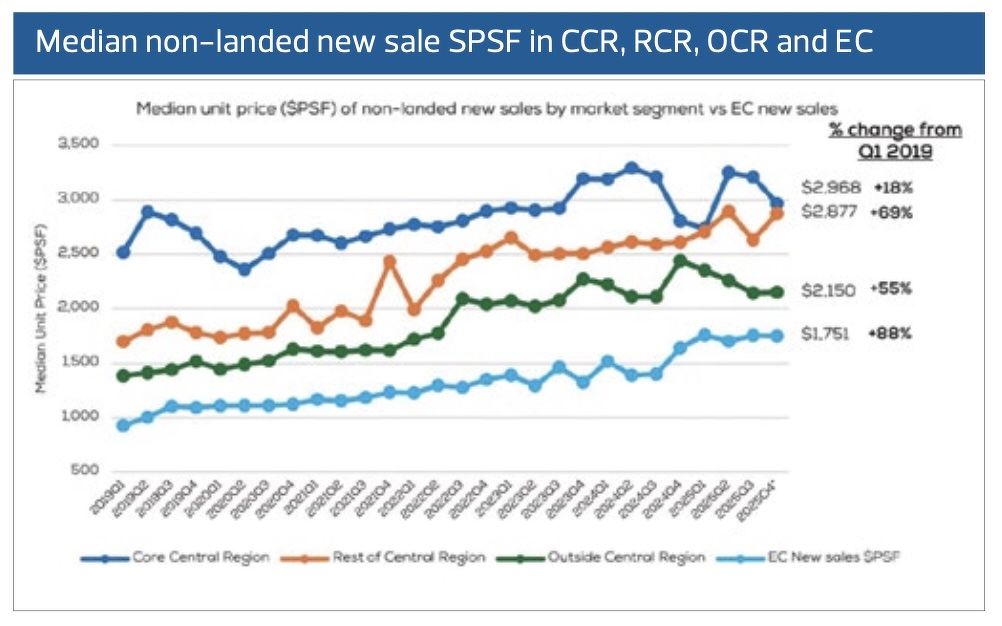

In 2025, the price gap between CCR and RCR new homes narrowed to 10%, the smallest in years, prompting many buyers to see value in CCR launches.

The narrowing of the CCR–RCR price gap in 2025 was driven by a strong pipeline of RCR launches, many sold at benchmark land rates and located near the CCR–RCR boundary, says ERA’s Chu. “This led to pricing that closely tracked core central developments, lifting overall RCR averages.”

In 2026, with just four RCR launches compared with 10 last year — and six CCR launches — upward pressure on RCR prices is likely to ease, adds Chu. As a result, the CCR–RCR price gap may widen slightly, moving closer to historical norms, though the difference is not expected to be significant.

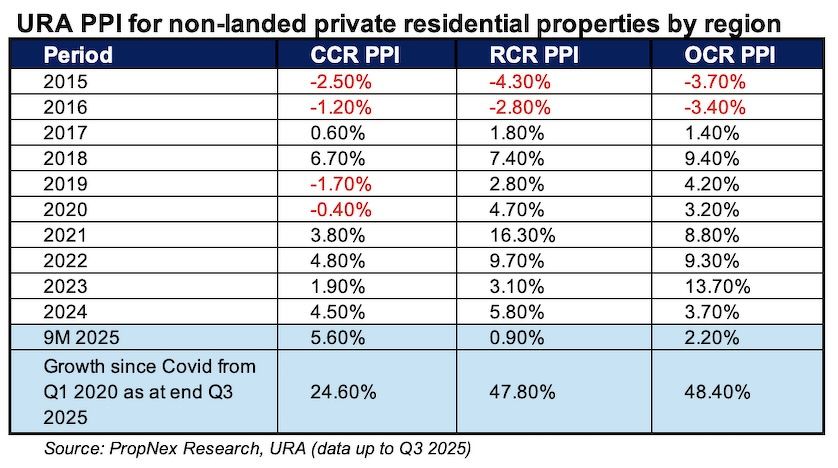

Based on URA’s private property price index for non-landed homes, CCR prices rose 5.6% in the first nine months of 2025, outpacing the 0.9% increase in the RCR and 2.2% growth in the OCR, according to PropNex Research.

Developers sold nearly 1,900 new CCR homes in the first 11 months of 2025, compared with just 378 units in the whole of 2024, reflecting a rebound in demand. Hence, Fong says the CCR is “on track to post its strongest year of price growth since 2021."

However, prices still lag behind those in other regions, according to PropNex Research: CCR values rose 24.6% between 1Q2020 and 3Q2025, compared with 47.8% in the RCR and 48.4% in the OCR.

Land prices, developer sales projections

PropNex projects developers’ sales to reach 8,000 to 9,000 units for the whole of 2026, citing relatively tight supply. ERA, meanwhile, forecasts 9,000 to 10,000 new homes.

For the private resale market, PropNex expects a higher transaction volume of 14,000 to 15,000 units, compared with ERA’s projection of 13,000 to 14,000 units.

Projections for overall private home price growth also vary across agencies. PropNex expects prices to rise by 3% to 4% in 2026, while ERA anticipates a 3% to 5% year-on-year increase. Huttons, meanwhile, projects a wider range of 2% to 5%, taking into account higher land acquisition costs.

While elevated land costs may nudge new launch prices upward in 2026, any increase is likely to be gradual or moderate, notes Fong.

Sources: URA, PropNex Research

Supporting this view, PropNex estimates that the average land rate for GLS sites sold in 2025 stood at $1,240 psf per plot ratio (ppr) — about 9.7% higher than the $1,130 psf ppr average recorded in 2024.

In 2025, about 67% of new non-landed private homes sold for below $2.5 million, broadly unchanged from 2024.

“Buyers remain price sensitive, and projects that strike the right balance between location, pricing and functionality will attract the most attention,” says Fong.

Developers are therefore expected to continue adopting price-quantum strategies, keeping a substantial proportion of units “within the $1.5 million to $2.5 million sweet spot”, he adds.

The site at the upcoming Chencharu Town (pictured). For buyers — particularly owner-occupiers and HDB upgraders — the market offers greater choice in the OCR, where affordability and functionality remain key drawcards (Phioto: Samuel Isaac Chua/EdgeProp Singapore)

‘A window of opportunity’

ERA’s Chu expects demand for new homes to remain resilient in 2026 despite higher prices. While URA data points to a moderate increase in project completions next year, the overall supply of newly completed homes remains limited, he notes. “This means that even with slightly higher completions, resale inventory is likely to stay tight, leading to continued spillover into the new homes market,” he adds.

For buyers — particularly owner-occupiers and HDB upgraders — the market offers greater choice in the OCR, where affordability and functionality remain key drawcards. At the same time, the limited supply of new CCR projects may pave the way for a gradual re-pricing in the prime segment after several years of underperformance.

“While 2026 will see its share of uncertainties, it also opens a window of opportunity,” says PropNex’s Fong. “Homebuyers will have more options at different price points as projects are launched in new housing precincts. The blurring of distinctions between regions will likely continue as improvements in infrastructure shrink distance, and more mixed-use projects are being built in the suburbs.”

Check out the latest listings for Narra Residences properties

Ask Buddy

Follow Us

Property updates, 24/7.

Subscribe to Newsletter

Market insights, delivered weekly.

Top Articles

Search